JasonDoiy

A extra in-depth model of this report, together with metric definitions and targets, was first shared with members of my High quality + Worth Methods subscription service within the Searching for Alpha Market on October 13, 2022.

Visa, Inc. (NYSE:V) is a poster little one for Peter Lynch’s “purchase what you realize” mantra. Client or service provider Visa accounts exist in most wallets and checkouts, whether or not on-ground or digital. The cost processor’s high-quality enterprise mannequin is textbook. Nonetheless, is it obtainable at a price worth for brand spanking new or present shareholders on this endemic bear market?

On this preliminary main ticker analysis report, I put Visa and its Class A typical shares by means of my market-beating, data-driven funding analysis guidelines of the worth proposition, shareholder yields, fundamentals, valuation, and draw back danger.

The ensuing funding thesis:

Visa’s high-quality enterprise mannequin and development profile presently worth the inventory above a disciplined worth investor’s most popular entry level. Nonetheless, the inventory rewards long-term shareholders with market-beating capital features and a pretty dividend yield on price.

My present general score: Maintain, primarily based on a bullish view of the corporate and a impartial view of the inventory.

Until famous, all knowledge offered is sourced from Searching for Alpha Premium as of the market shut on October 21, 2022; and supposed for illustration solely.

Dynamic Enterprise Mannequin or Freeway Theft?

V (Class A shares) is a dividend-paying large-cap inventory within the data expertise sector’s knowledge processing and outsourced companies business.

Visa Inc. operates as a funds expertise firm worldwide and facilitates digital funds amongst customers, retailers, monetary establishments, companies, strategic companions, and authorities entities. Visa was based in 1958 and is headquartered in San Francisco, California, USA.

My worth proposition elevator pitch for Visa:

Family identify in cost processing has half its revenues dropping to the underside line. Now that is a dynamic enterprise mannequin if not authorized freeway theft.

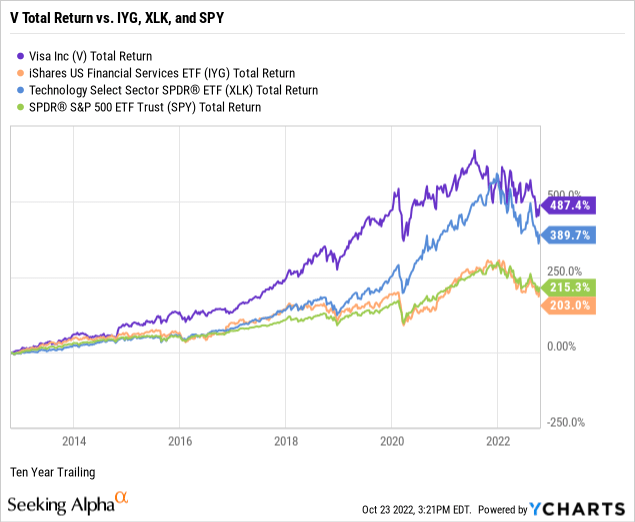

The chart beneath illustrates the inventory’s efficiency in opposition to the iShares U.S. Monetary Companies ETF (NYSE:IYG), the Know-how Choose Sector SPDR Fund ETF (NYSE:XLK), and the SPDR S&P 500 ETF Belief (NYSE:SPY) over the previous ten years.

In the end, I purpose to beat the benchmark indices over time when investing in particular person frequent shares. For instance, V has outperformed the full returns of its business, sector, and market, reflecting its positioning as a core portfolio holding.

My worth proposition score for Visa: Bullish.

Yields Underperforming the 10-Yr Treasury

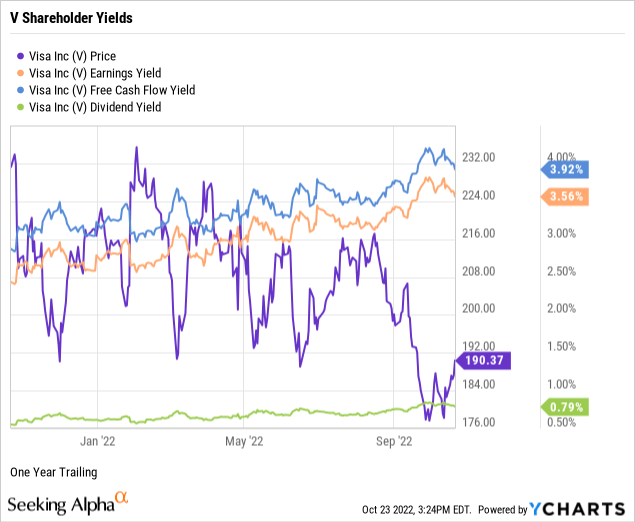

As a part of my due diligence, I common the full shareholder yields on earnings, free money movement, and dividends to measure how a focused inventory compares to the prevailing yield on the 10-Yr Treasury benchmark word. In different phrases, what’s the fairness bond charge of the frequent shares?

V was buying and selling at an earnings yield of three.56% and a free money movement yield of three.92%, as demonstrated within the beneath chart.

Visa provides a modest ahead dividend yield of 0.79%. Nonetheless, its conservative 20.83% payout ratio signifies a protected, well-covered dividend with loads of room for annual raises.

I favor excessive dividend yields solely when calculated on a price foundation. Notably, V was yielding 4.60% on an annual payout of $1.50 and split- and dividend-adjusted 10-year price foundation of $32.63 per share, or 381 foundation factors above the ahead yield.

Subsequent, I take the typical of the three shareholder yields to measure how the inventory compares to the prevailing yield of 4.22% on the 10-Yr Treasury benchmark word. For instance, the typical shareholder yield for V was 2.76% or 4.03% if utilizing a ten-year price foundation.

Typical market knowledge holds equities as riskier than U.S. bonds. Thus, securities resembling V, which reward shareholders with yields at or beneath the federal government benchmark, argue for proudly owning the bond as a substitute of the inventory.

Do not forget that earnings and free money movement yields are inverse valuation multiples, suggesting that V trades at a premium. I am going to additional discover valuation later on this report.

My shareholder yields score for V: Impartial.

Distinctive Efficiency in Golden Gate Metropolis

Now, I’ll discover the basics of Visa, uncovering the efficiency power of the corporate’s senior administration.

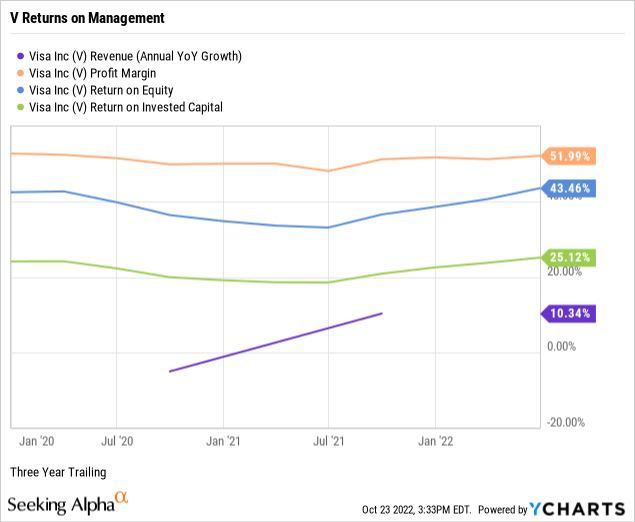

Per the beneath chart, Visa had three-year annualized income development of 10.34%, exceeding the 6.23% median development for the knowledge expertise sector.

Visa had a trailing three-year double-digit pre-tax internet revenue margin of an astounding 51.99%, far outperforming the sector’s modest median internet margin of three.87%.

Visa was producing a trailing three-year return on fairness or ROE at a convincing 43.46% in opposition to a median ROE of simply 6.51% for the sector.

Notably, Visa is amidst a $12 billion share buyback program with no expiration date. Nonetheless, is the board shopping for their shares at a premium?

At 25.12%, Visa six-packs the sector’s median return on invested capital or ROIC of three.80%, indicating that its senior executives are competent capital allocators.

ROIC must exceed the weighted common price of capital or WACC by a cushty margin, confirming administration’s capacity to outperform its capital prices. For instance, Visa’s ROIC comfortably exceeds its trailing WACC of 9.49%, an in any other case excessive capital price foundation. (Supply: GuruFocus).

The double-digit income development, tremendous internet revenue margin, and excellent returns on fairness and capital point out distinctive administration efficiency in The Golden Gate Metropolis.

My fundamentals score for Visa: Bullish.

An Overpriced Fintech Juggernaut

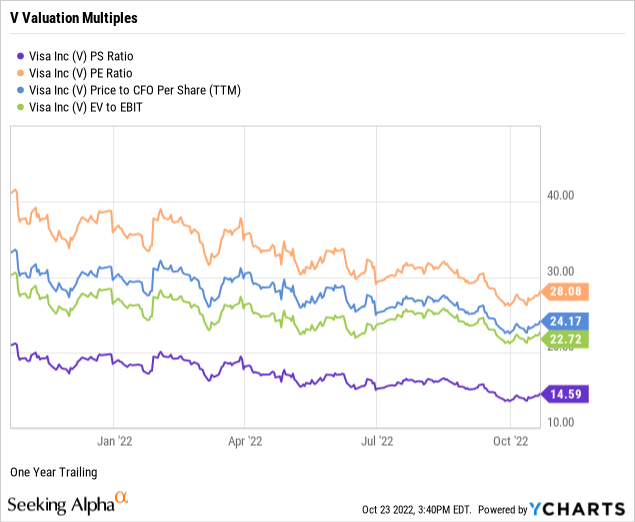

I’ve constructed and maintained a market-beating household portfolio of the frequent shares of tolerating enterprises since 2009, counting on simply 4 valuation multiples to estimate the intrinsic worth of a focused high quality firm’s inventory worth.

V was buying and selling at a price-to-sales ratio or P/S of 14.59 instances, considerably increased than 2.48 instances for the knowledge expertise sector and a pair of.15 instances for the S&P 500. (Supply of S&P 500 P/S: Charles Schwab & Co.) Thus, the weighted business plus market sentiment suggests a premium-priced inventory relative to Visa’s topline.

V had a price-to-earnings a number of or P/E of 28.08 instances in opposition to a sector median P/E of 20.32, indicating investor sentiment overvalues the inventory worth relative to earnings per share. Additional, V was buying and selling at a premium a number of to the S&P 500’s general P/E of 18.27. (Supply of S&P 500 P/E: Barron’s).

At 24.17 instances, V’s price-to-operating money movement a number of was buying and selling at a premium to the sector’s median of 18.65, indicating that the market costs the inventory above truthful worth relative to present money flows.

Towards the broader sector median of 17.31, V was buying and selling at 22.72 instances enterprise worth to working earnings or EV/EBIT, signaling the inventory was overbought or undersold by the market.

Weighting my most popular valuation multiples suggests the market assigns a hefty premium to Visa’s inventory worth relative to gross sales, earnings, money movement, and enterprise worth. Subsequently, primarily based on the basics and valuation metrics uncovered on this report, dangers and potential catalysts however, I’d name V an overpriced inventory of a legacy A-rated fintech juggernaut.

My valuation score for V: Bearish.

Liquidity and Moat Drive Under Common Danger

When assessing the draw back dangers of an organization and its frequent shares, I give attention to 5 metrics that, in my expertise as a person investor and market observer, usually predict the potential danger/reward of the funding. Therefore, I assign a draw back risk-weighted score of above common, common, beneath common, or low, biased towards beneath common and low danger profiles.

Alpha-rich buyers goal corporations with clear aggressive benefits from their services or products. An investor or analyst can streamline the worth proposition of an enterprise with an financial moat task of extensive, slim, or none. Morningstar assigns V a large moat score.

Lengthy-term debt protection demonstrates stability sheet liquidity or an organization’s capability to pay down debt in a disaster. Notably, as reported on its June 2022 quarterly monetary statements, at 1.41 instances, Visa’s long-term debt protection might repay 100% of its longer-term debt obligations in a disaster utilizing its liquid belongings, resembling money and equivalents, short-term investments, and accounts receivables.

In an extra check of its paydown capability, Visa’s long-term debt to fairness was a manageable 57.90%.

Visa’s short-term debt protection or present ratio was 1.43 instances. Thus, its stability sheet offers vital liquid belongings to pay down 100% of its present liabilities, together with accounts payable, accrued bills, short-term borrowings, and earnings taxes.

As a long-term investor, I exploit a five-year beta pattern line, and V’s 60-month trailing beta was 0.92. At 1.01, its shorter-term 24-month beta was about equal. With worth volatility buying and selling across the S&P 500 customary of 1.00, V presents as a market-average core portfolio holding.

The brief curiosity share of the float for V was a primarily bear paws-off of two.73%. So maybe the near-sighted merchants view the inventory as a wide-moat fintech staple with a loyal and sustainable buyer, service provider, and investor base. Nonetheless, there could also be some skepticism about Visa’s development prospects in a recession.

Visa is a essentially superior firm with a client/service provider market-dominating worth proposition and a pretty danger profile in opposition to a broader bear market.

My draw back danger score for Visa: Under Common.

Visa Catalysts and Remaining Ideas

Catalysts confirming or contradicting my general maintain funding thesis on Visa, Inc.’s Class A typical shares embrace, however should not restricted to:

Confirmations: Visa’s main market share creates extra alternatives for loss than acquire. The oligopolistic nature of the business makes Visa and its opponents targets for regulators, doubtlessly leading to hefty fines. Governments might shut Visa out of some emerging-market alternatives. Continued excessive inflation and financial recession might sluggish development and profitability. Contradictions: Visa has a commanding market share in a scalable business, permitting enchancment of its already spectacular margins. There are nonetheless loads of alternatives for development in digital funds, which have surpassed money funds globally. Though nonetheless elevated to the sector and the broader market, present valuation multiples are at five-year lows. Visa is a market chief offering huge monetary power and profitability.

(Extra supply of catalysts: Morningstar.)

Visa’s high-quality enterprise mannequin and development profile presently worth the inventory above a disciplined worth investor’s most popular entry level. The family identify in cost processing has half its revenues dropping to the underside line, a dynamic enterprise mannequin if not authorized freeway theft. Visa’s worth proposition is very sustainable, fundamentals are strong, and draw back dangers are beneath common. Nonetheless, shareholder yields underperform the 10-Yr Treasury.

Nonetheless, the inventory rewards long-term shareholders with market-beating capital features and a pretty dividend yield on a price foundation.

{kind=link}