In late 2021 and early 2022, a lot of pundits warned that the Fed was transferring too rapidly to tighten financial coverage. It’s now clear that these pundits have been fallacious. Not solely did the Fed not do an excessive amount of tightening, there’s nearly no proof that the Fed has tightened financial coverage in any respect, at the least to any measurable extent.

Roughly a yr in the past, it turned obvious (even to the Fed) that the financial system was transferring towards overheating. So why would possibly an abrupt tightening in late 2021 have been a mistake? In spite of everything, inflation is a giant drawback, and tight cash is the one dependable approach of lowering inflation. Tight cash can scale back NGDP progress to a stage in line with 2% inflation.

The usual reply is that the Fed must be cautious, as tight cash imposes ache on the labor market. And I imagine that’s true—all of us noticed what occurred in 2008 when the Fed over tightened. The unemployment fee shot as much as 10%.

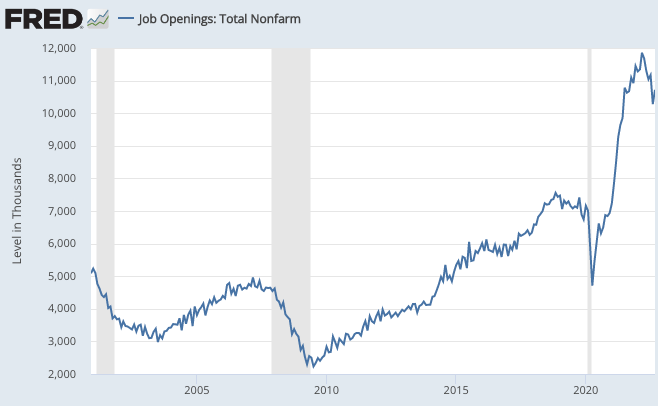

If that’s your criterion for over tightening, then the Fed actually has not performed so. Certainly not solely has the Fed not imposed extreme ache on the labor market, they’ve produced such fast NGDP progress in 2022 that the labor market is sort of absurdly scorching. Job openings are at present far above the extent of earlier increase durations similar to late 2019.

A fascinating coverage of bringing inflation down by way of gradualism would stability the prices of inflation and unemployment. It could impose a modest quantity of ache on the labor market, however not an excessive amount of. However the Fed has not imposed any ache in any respect. Certainly it hasn’t even returned to labor market again right down to the increase situations of late 2019. There’s been no balancing of prices. And there’s been no vital discount in inflation in any respect. Regardless of what you learn within the press, there’s been no tight cash coverage in 2022.

Later this yr, I plan to launch a ebook that discusses issues in the best way we measure the stance of financial coverage. Listed below are some errors which were made in 2021-22:

1. Assuming that rates of interest measure the stance of financial coverage. They don’t. Rising charges don’t point out tighter cash. The cash provide can be not a great indicator.

2. Gradualism in adjusting the coverage instrument. It’s true that you just’d wish to deliver NGDP progress down steadily, in order to not create lots of unemployment. However that doesn’t imply that it’s essential increase the goal rate of interest at a gradual tempo.

3. Complicated a falling inventory and bond market with tight cash. (That is referred to a tighter “monetary situations”.) Essentially the most expansionary financial coverage in my lifetime (1966-81) was accompanied by a really weak efficiency of the inventory and bond markets. Markets hate excessive inflation—however excessive inflation just isn’t a product of tight cash. Don’t equate tight monetary situations and tight cash.

4. Assuming that financial coverage impacts NGDP with a protracted and variable lag. In reality, financial coverage impacts NGDP nearly instantly, as we see within the few financial shocks which are clearly recognized (similar to 1933). It looks as if a protracted lag if you happen to assume that rising charges are tight cash, however they aren’t.

5. An excessive amount of concentrate on inflation and never sufficient concentrate on NGDP progress. There was a protracted and completely ineffective debate about whether or not inflation was attributable to provide or demand aspect components. It doesn’t matter! What issues is NGDP progress, which is 100% demand pushed. And NGDP progress has clearly been too excessive.

6. President Biden waited too lengthy to reappoint Powell. It’s doable that Powell felt uncomfortable making the choice to tighten financial coverage only a month or two earlier than Biden was to make his determination on a brand new Fed chair.

7. Most necessary of all (by far), the Fed’s FAIT fiasco. The Fed signaled an intention to focus on the typical fee of inflation at 2%, simply because it adopted a extremely expansionary financial coverage. FAIT truly would have been an excellent thought, if applied correctly. However as quickly as stabilizing the typical inflation fee required a decent cash coverage, the Fed introduced that the coverage was uneven, and that they’d not offset inflation overshoots with future undershoots.

In late 2019, financial coverage within the US was in an excellent place, the very best coverage I’ve seen in my total life. Tragically, all these features have been thrown away over the next few years, in a reckless try and artificially create prosperity by printing a lot of cash. FAIT would have been an excellent coverage. Uneven FAIT has been a catastrophe.

PS. I received this e mail from Bloomberg:

It’s that point of the month—jobs day. The US nonfarm payrolls report shall be scoured for any clue that the Fed can downshift to a 50 bp hike subsequent time round or reaffirm the next terminal fee. Proof could also be blended: The financial system most likely added 195,000 jobs in October, fewer than in September however nonetheless OK.

No, 195,000 wouldn’t be OK; it could be far too excessive. I’m not advocating excessive unemployment, however is it an excessive amount of to ask that the Fed at the least deliver the labor market again to the traditionally robust increase of late 2019, as a substitute of the virtually absurd overheating that we see at the moment? In any case, Bloomberg was fallacious. The financial system added 261,000 jobs in October, and former months have been additionally revised upwards. Nominal wage progress was additionally above expectations. We’re nonetheless booming.

PPS. A couple of months again, a complete bunch of commenters informed me that the US entered a recession in early 2022. These individuals have to rethink their mannequin of the financial system. Ditto for these individuals who warned that the Fed was tightening too aggressively in early 2022. Time for some soul looking out. (I did some soul looking out in January, once I realized that the Fed’s FAIT was a sham.)

.jpeg?itok=EJhTOXAj'%20%20%20og_image:%20'https://cdn.mises.org/styles/social_media/s3/images/2025-03/AdobeStock_Supreme%20Court%20(2).jpeg?itok=EJhTOXAj)

{kind=link}