Bet_Noire/iStock by way of Getty Photographs

Introduction

I was a shareholder of South African gold producer DRDGold (NYSE:DRD) till 2017 and I’ve been intently following the corporate over the previous few months because it’s beginning to look more and more low-cost primarily based on fundamentals. My newest article on SA about DRDGold was written in August.

The corporate not too long ago launched its manufacturing outcomes for the third quarter of 2022 (or Q1 for FY23), and I believe they appeared robust contemplating gold costs are sliding and South Africa is experiencing a difficult interval of load shedding. Let’s evaluate.

Overview of the Q3 2022 outcomes

In case you have not learn any of my earlier articles about DRDGold, right here’s a fast description of the enterprise. The corporate owns two tailings retreatment complexes throughout the huge Witwatersrand Basin, the place half of the world’s gold has been mined. A number of many years in the past, the common gold grades throughout the globe have been a lot greater which implies that the cut-off grades have been additionally greater, and this led to the buildup of an unlimited quantity of mining waste (or tailings) that was left behind after mines shut down. DRDGold makes use of massive hoses to slurrify slime or sand after which pumps this materials by way of a community of pipes so far as 60 km away for processing in its services.

DRDGold

In the intervening time, the corporate has an annual manufacturing of about 180,000 ounces of gold whereas its mineral reserves stand 5.35 million ounces of gold, making it the most important gold producer on this planet from tailings. The mine life (when you can name it that on this case) is thus over 20 years. For my part, the principle problem for tailings retreatment companies is excessive unit prices as grades are low. Nevertheless, there is no such thing as a exploration danger and capital bills are restricted in comparison with conventional mines.

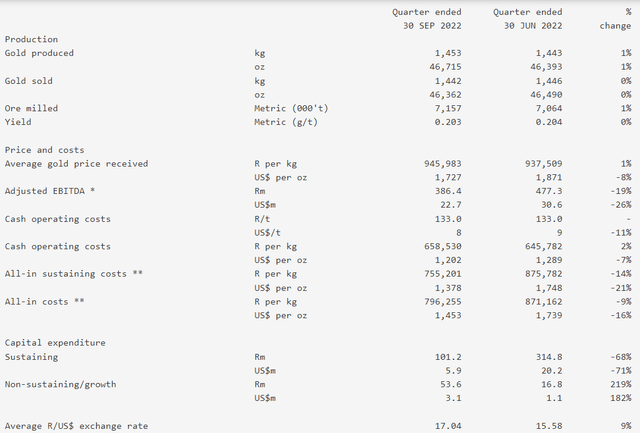

Turning our consideration to the Q3 2022 manufacturing and monetary outcomes, you’ll be able to see from the desk under that gold manufacturing charges have been secure as they inched up by simply 1% quarter on quarter, primarily resulting from a 1% enchancment in tonnage throughput. The yield was solely 0.001g/t decrease at 0.203g/t, which comes to point out how constant and predictable the manufacturing efficiency tends to be right here. All-in prices declined by 14% in rands because of decrease sustaining capital bills and the lower was even greater in US {dollars} because of the weaker rand. Nevertheless, EBITDA slumped by 26% to $22.7 million resulting from an 84.7 million rand ($4.7 million) insurance coverage declare acknowledged in Q2 2022.

DRDGold

Total, I believe it was a stable quarter from each manufacturing and monetary standpoints regardless of a number of days wherein there was load shedding introduced by nationwide electrical energy firm Eskom. Throughout these durations, DRDGold has to scale back the quantity of energy it attracts from the grid and depend on costly diesel mills. To keep away from this sooner or later, the corporate plans to construct a 20 MW solar energy plant on the Ergo advanced. Nevertheless, I’m skeptical that DRDGold will be capable to accomplish this anytime quickly regardless of having the funding as securing permits to construct a personal energy plant in South Africa is difficult. For instance, South Africa-focused platinum group metals (PGM) producer Sibanye Stillwater (SBSW), which holds 50.1% of DRDGold, has been attempting to construct its personal solar energy plant since not less than 2015.

Trying on the steadiness sheet, money and money equivalents decreased by 280.5 million rands ($15.6 million) quarter on quarter to 2.25 billion rands ($125.1 million) as the corporate paid out a 342.5 million rands ($19.1 million) last dividend in the course of the interval. Sadly, the money and money equivalents that DRDGold retains are primarily in rands which implies that its money pile is lowering in greenback phrases. This money pile is more likely to diminish within the coming months as the corporate plans to make capital investments of about 1.4 billion rands ($78 million) in FY23 ending on June 30. Nevertheless, remember that this sum contains an undisclosed quantity for the photo voltaic plant.

Trying on the future, DRDGold expects to provide between 160,000 ounces and 180,000 ounces of gold in FY23 at money working prices of 685,000 rands (38,180) per kg. Contemplating the corporate produced over 46,000 ounces of gold at money working prices of simply over 685,000 rands per kg in Q1 FY23, the steering appears to be like simply achievable. Until gold costs proceed to slip, I believe it may obtain EBITDA of over $100 million in FY23. This could imply that DRDGold is buying and selling at lower than 4x ahead EBITDA as of the time of writing. Sure, I do know that you just shouldn’t take a look at EBITDA when calculating the worth of a mining firm, however I believe it’s okay on this case because the mine life is over 20 years.

Trying on the dangers for the bull case, I believe that the key one is weaker gold costs over the approaching months. The sentiment within the gold sector is kind of bearish in the meanwhile as main central banks world wide are elevating rates of interest at a fast tempo. As well as, gold costs have a unfavorable correlation to the US greenback, they usually dipped under $1,700 per ounce close to the tip of September. But, they nonetheless stay at fairly excessive ranges in comparison with the times earlier than the COVID-19 pandemic.

goldprice.org

Different close to time period potential dangers that I can consider embrace a stronger rand, extra load shedding from Eskom, and excessive summer time rainfall ranges.

Investor takeaway

For my part, DRDGold is a secure and predictable gold firm from a manufacturing standpoint and has a wholesome amount of money in its coffers in the meanwhile. I believe it’s seemingly that numerous the FY23 capital bills could possibly be delayed resulting from regulatory points with the photo voltaic plant at Ergo.

Nevertheless, margins may shrink considerably if gold costs proceed to say no, and because of this I price DRDGold as a speculative purchase. For my part, the corporate may climate an extended interval of low gold costs because of its massive money place, however the share worth is more likely to fall. I believe it could possibly be greatest for risk-averse buyers to keep away from this inventory.

{kind=link}