Scott Olson

By Valuentum Analysts

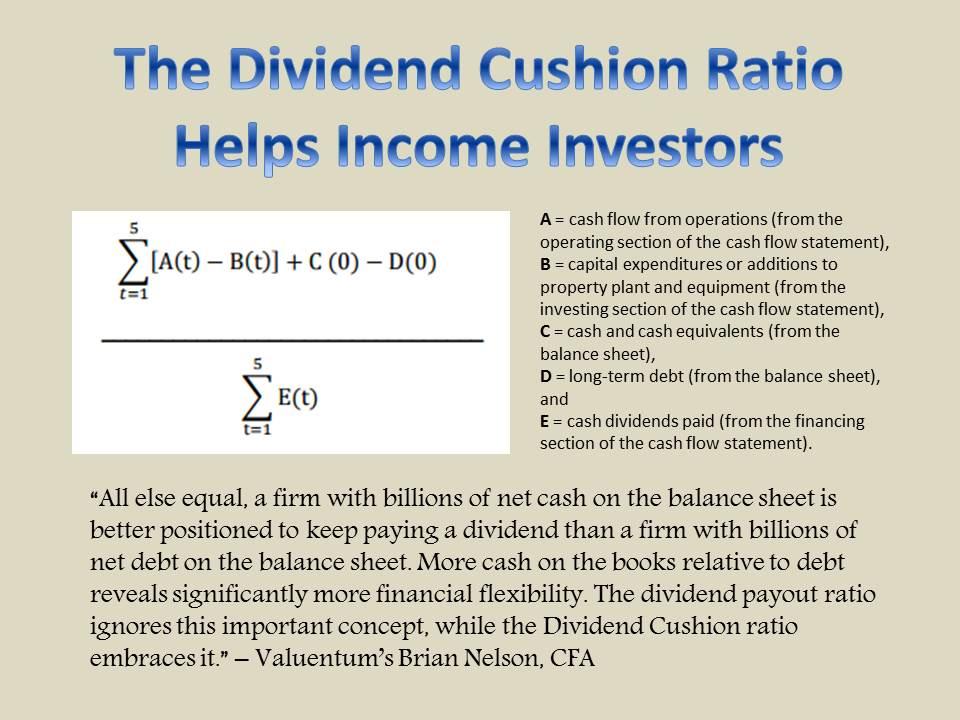

At Valuentum, we like to make use of a metric referred to as the Dividend Cushion ratio to guage an organization’s dividend well being. At its core, the Dividend Cushion ratio is designed to offer the dividend progress investor and the revenue investor with a forward-looking, free-cash-flow primarily based opinion of the power and future progress potential of an organization’s dividend. The ratio not solely highlights dangers related to potential dividend cuts, however the ‘cushion’ behind the Dividend Cushion reveals simply how a lot capability a agency has to proceed rising its dividend sooner or later, above and past present expectations.

The Dividend Cushion ratio is without doubt one of the strongest monetary instruments an revenue or dividend progress investor can use along with qualitative dividend evaluation. The ratio is one-of-a-kind in that it’s each free-cash-flow primarily based and ahead wanting. Since its creation in 2012, the Dividend Cushion ratio has forewarned readers of roughly 50 dividend cuts. We estimate its efficacy at ~90%. (Picture Supply: Valuentum)

The muse behind the measure–assessing future free money flows relative to future money dividend funds within the context of an organization’s steadiness sheet–remains as related as ever.

For instance, Lumen Applied sciences (LUMN) introduced November 2 that it might eradicate its payout. The attention-grabbing factor about Lumen Applied sciences was that it had a robust dividend payout ratio and free money move protection of the dividend, however what it didn’t have was a robust internet money on the steadiness sheet. The truth is, it had an enormous internet debt place, and administration reduce the dividend. The place different dividend metrics did not establish the dangers of the payout, the Dividend Cushion ratio handed with flying colours.

Now, let’s check out Finest Purchase (NYSE:BBY) in the identical systematic dividend framework, however some background first.

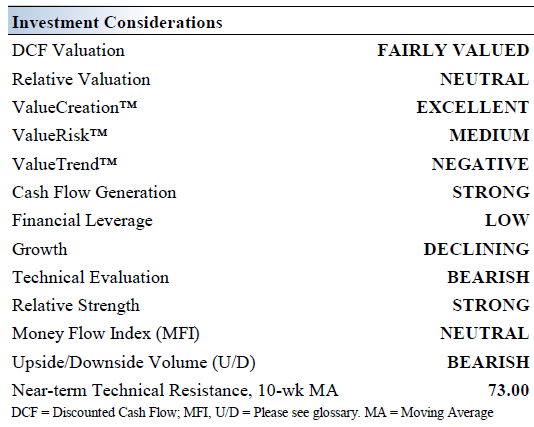

Finest Purchase’s Key Funding Issues

Picture Supply: Valuentum

Finest Purchase is the worldwide chief in shopper electronics so far as huge field retailers go. The corporate should proceed to reinvent itself to mitigate aggressive pressures from on-line powerhouses together with Amazon (AMZN). Finest Purchase has notable market share in areas similar to residence theater, notebooks, and desktops. It was based in 1966 and has managed the ups and downs of many financial cycles.

In October 2021, Finest Purchase launched its Totaltech membership program that amongst different issues affords discounted and free Geek Squad companies, free warranties on certified merchandise, particular reductions, and cheaper and sooner transport charges.

Gross sales of shopper electronics surged within the wake of the COVID-19 pandemic as households turned to work-from-home and school-from-home actions. Going ahead, these tailwinds are turning into headwinds, and Finest Purchase will possible not be capable to maintain that stage of income progress. The agency is leaning on its e-commerce operations to stay related within the digital period.

Finest Purchase accomplished its exit of Mexico in fiscal 2021. The corporate goals to maintain its remaining bodily footprint related by specializing in the client expertise (retaining a employees educated of tech services) and by providing related tech product and repair help, and set up companies.

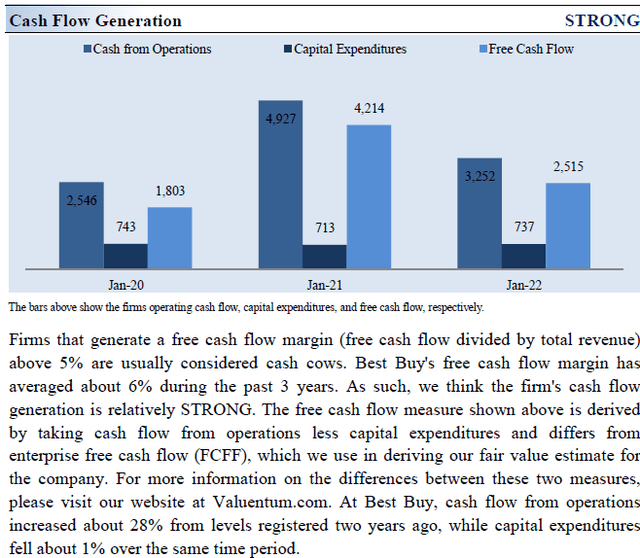

Finest Purchase continues to be a strong generator of free money move. The corporate’s e-commerce enterprise has impressed of late, however value pressures from rising labor and transportation bills can’t be ignored.

Newest Quarterly Outcomes

We final wrote up Finest Purchase on Looking for Alpha means again in August 2018, and the corporate continues to battle on-line competitors and discover methods to innovate to maintain its huge field presence alive. The corporate reported its fiscal second-quarter outcomes on August 30 (for the interval ending July 30, 2022), and whereas enterprise comparable retailer gross sales confronted strain, its two-year stacked comp was nonetheless wholesome at 7.5% — two-year stacked comps are derived by including the comparable retailer gross sales share for the previous two year-over-year quarters. Here’s what administration needed to say concerning the quarterly efficiency:

We’re clearly working in an uneven gross sales setting. As we entered the 12 months, we anticipated the buyer electronics trade to be softer than final 12 months following two years of elevated progress pushed by unusually sturdy demand for know-how services and fueled partly by stimulus {dollars}. The macro setting has been extra challenged on account of a number of elements and that has put extra strain on our trade.

Inflationary pressures are hurting customers, however as Finest Purchase’s operations normalize after the uneven gross sales cycle that occurred throughout COVID-19, we count on it to beat challenges and stable-to-modest progress to renew. That stated, comparable retailer gross sales could proceed to say no a bit greater than expectations this 12 months given potential recessionary situations as we head into the all-important vacation season (troublesome year-over-year comparisons will not assist).

Free money move stays optimistic at Finest Purchase, coming in at $268 million in the course of the first half of its fiscal 12 months, but it surely fell in need of its money dividends paid of $397 million over the identical time interval. It is a purple flag. The corporate now not retains a internet money place on the finish of its fiscal second quarter both, with Finest Purchase now holding a internet debt place of $344 million. Its internet money place on the finish of July 2021 was ~$3 billion and $1.72 billion, excluding short-term debt (as proven within the Dividend Cushion calculations under), as of its final fiscal 12 months finish (January 29, 2022).

Readers ought to maintain these essential mid-year modifications in thoughts as we consider Finest Purchase’s Dividend Cushion ratio utilizing final fiscal 12 months’s internet money place and forecasts of free money move. For the Dividend Cushion ratio, we use an organization’s steadiness sheet from final fiscal 12 months and usually don’t make interim updates inside the Dividend Cushion ratio for the steadiness sheet given cash-flow concerns and seasonal modifications for retailers by the course of the 12 months (e.g. stock builds and the like).

Readers, nonetheless, ought to concentrate on what may very well be a giant anticipated swing within the Dividend Cushion ratio come subsequent fiscal 12 months on account of Finest Purchase’s steadiness sheet well being. Weakened free money move protection of the payout by the primary half of its fiscal 12 months and a internet debt place have occurred out of the blue at Finest Purchase, and we’ll present an adjusted interim Dividend Cushion ratio under to assist readers assess the state of affairs, along with final fiscal 12 months’s snapshot (which is offered within the picture).

Finest Purchase’s Dividend Well being Evaluation

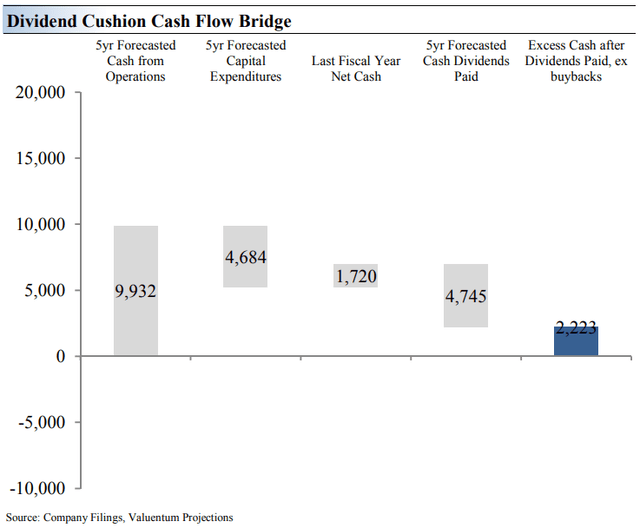

Dividend Cushion Money Movement Bridge Analysis (Picture Supply: Valuentum)

The Dividend Cushion Money Movement Bridge, proven within the picture above, illustrates the parts of the Dividend Cushion ratio and highlights intimately the various drivers behind it. Finest Purchase’s Dividend Cushion Money Movement Bridge reveals that the sum of the corporate’s 5-year cumulative free money move technology, as measured by money move from operations much less all capital spending, plus its internet money/debt place on the steadiness sheet, as of the final fiscal 12 months, is bigger than the sum of the following 5 years of anticipated money dividends paid.

As a result of the Dividend Cushion ratio is forward-looking and captures the trajectory of the corporate’s free money move technology and dividend progress, it reveals whether or not there shall be a money surplus or a money shortfall on the finish of the 5-year interval, making an allowance for the leverage on the steadiness sheet, a key supply of danger.

On a elementary foundation, we consider corporations which have a robust internet money place on the steadiness sheet and are producing a big quantity of free money move are higher in a position to pay and develop their dividend over time. Corporations which are buried below a mountain of debt and don’t sufficiently cowl their dividend with free money move are extra prone to a dividend reduce or a suspension of progress, all else equal, in our opinion. Typically talking, the higher the ‘blue bar’ to the fitting is within the optimistic, the extra sturdy an organization’s dividend, and the higher the ‘blue bar’ to the fitting is within the unfavorable, the much less sturdy an organization’s dividend.

As of final fiscal 12 months, issues had been wanting okay for Finest Purchase (as proven above). Nevertheless, after contemplating what may occur to the agency’s steadiness sheet on the finish of the its fiscal 12 months coupled with weakening free money move protection of the dividend, Finest Purchase’s Dividend Cushion ratio will possible come out nearer to 1 on the finish of the upcoming fiscal 12 months. We have a tendency to love firm dividends which have Dividend Cushion ratios effectively north of 1, not at parity (1), which is slicing it fairly shut. That stated, we’ll should see how Finest Purchase’s steadiness sheet finally ends up on the finish of the fiscal 12 months and if the corporate is ready to generate materials free money move effectively in extra of its money dividend paid in the course of the all-important vacation season to make up for the year-to-date shortfall–and then some. It will higher inform our forecasts of future free money move.

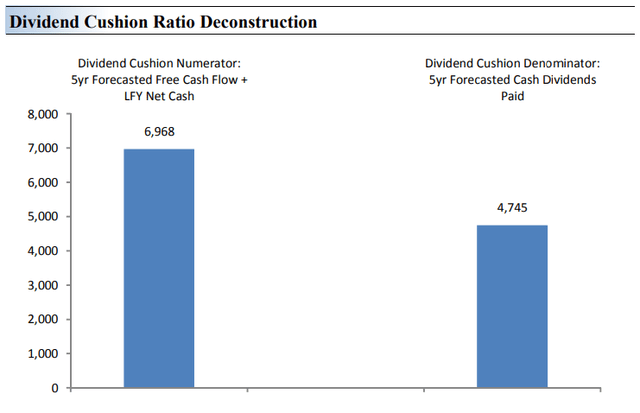

Dividend Cushion Ratio Deconstruction (Picture Supply: Valuentum)

The Dividend Cushion Ratio Deconstruction, proven within the picture above, reveals the numerator and denominator of the Dividend Cushion ratio — once more that is the calculation on the finish of Finest Purchase’s final fiscal 12 months (and issues have modified by the course of the 12 months). On the core, the bigger the numerator, or the more healthy an organization’s steadiness sheet and future free money move technology, relative to the denominator, or an organization’s money dividend obligations, the extra sturdy the dividend. Within the context of the Dividend Cushion ratio, Finest Purchase’s numerator is bigger than its denominator suggesting that it will possibly cowl its payout (because it has performed this 12 months), however once more, there are clouds on the horizon.

The Dividend Cushion Ratio Deconstruction picture places sources of free money within the context of economic obligations subsequent to anticipated money dividend funds over the following 5 years on a side-by-side comparability. As a result of the Dividend Cushion ratio and lots of of its parts are forward-looking, our dividend analysis could change upon subsequent updates as future forecasts are altered to mirror new data. That is what we’re emphasizing on this word. Proper now, Finest Purchase’s dividend appears okay, with a Dividend Cushion ratio of 1.5 (as derived within the photos above), however we count on its Dividend Cushion ratio to fall nearer to 1 upon its subsequent fiscal 12 months replace (and perhaps decrease), and dividend buyers ought to pay attention to the elevated dangers.

Finest Purchase’s Money Movement Valuation Evaluation

Picture Supply: Valuentum

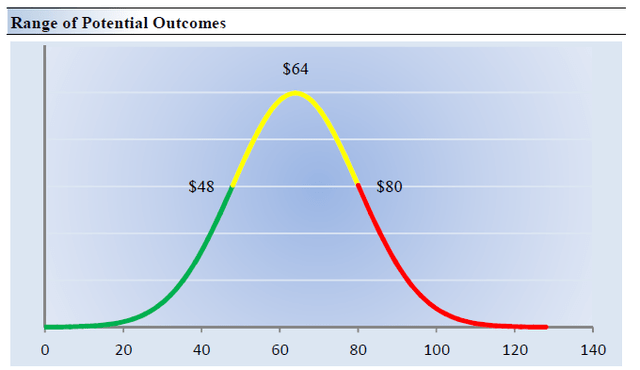

We expect Finest Purchase is price $64 per share with a good worth vary of $48-$80 (shares are buying and selling at ~$68 for the time being). The margin of security round our honest worth estimate is pushed by the agency’s MEDIUM ValueRisk ranking, which is derived from an analysis of the historic volatility of key valuation drivers and a future evaluation of them.

Our near-term working forecasts, together with income and earnings, don’t differ a lot from consensus estimates or administration steering. Our mannequin displays a compound annual income progress price of -0.8% in the course of the subsequent 5 years, a tempo that’s decrease than the agency’s 3- 12 months historic compound annual progress price of 6.5%.

Our valuation mannequin displays a 5-year projected common working margin of 4.7%, which is under Finest Purchase’s trailing 3-year common. Past 12 months 5, we assume free money move will develop at an annual price of 8.6% for the following 15 years and three% in perpetuity. For Finest Purchase, we use a 9.4% weighted common value of capital to low cost future free money flows.

Finest Purchase’s Margin of Security Evaluation

Picture Supply: Valuentum

Our discounted money move course of values every agency on the idea of the current worth of all future free money flows. Though we estimate Finest Purchase’s honest worth at about $64 per share, each firm has a spread of possible honest values that is created by the uncertainty of key valuation drivers (like future income or earnings, for instance). In spite of everything, if the longer term had been identified with certainty, we would not see a lot volatility within the markets as shares would commerce exactly at their identified honest values.

Our ValueRisk ranking units the margin of security or the honest worth vary we assign to every inventory. Within the graph above, we present this possible vary of honest values for Finest Purchase. We expect the agency is engaging under $48 per share (the inexperienced line), however fairly costly above $80 per share (the purple line). The costs that fall alongside the yellow line, which incorporates our honest worth estimate, signify an affordable valuation for the agency, in our opinion.

Concluding Ideas

Shares of Finest Purchase are buying and selling at ~$68 on the time of this writing, about in-line with our honest worth estimate. The corporate’s yield stands at ~5.2%. The agency continues to battle competitors, and whereas it’s dealing with an uneven gross sales cycle with troublesome year-over-year comparisons, sturdy efficiency in e-commerce has been a key driver, and we will by no means depend Finest Purchase out.

The agency had a internet money place on the finish of fiscal 2022, however this has modified by the course of its fiscal 12 months. The corporate continues to generate free money move, nonetheless, and whereas we’ll should see how issues shake out in the course of the all-important vacation promoting season, by the primary half of its fiscal 12 months, free money move has come up brief relative to money dividends paid. Each of those are huge modifications relative to final fiscal 12 months, and readers ought to count on a Dividend Cushion ratio a lot decrease than that of final fiscal 12 months’s, of which our systematic dividend methodology relies upon.

All instructed, it’s troublesome for us to get too enthusiastic about any huge field retailer given the threats posed by the proliferation of e-commerce and rising aggressive headwinds. We expect Finest Purchase’s dividend is okay for the time being (primarily based on final fiscal 12 months’s Dividend Cushion ratio), however buyers have to pay shut consideration to its trade backdrop and ever-increasing competitors to contemplate it to be sustainable over the long term. We’re additionally noticing some essential modifications in its financials which are elevating purple flags, suggesting a a lot decrease Dividend Cushion ratio subsequent fiscal 12 months and potential severe dangers to the payout. Readers ought to take word.

{kind=link}