Andy Feng

Q3 recap and thesis

I have been writing a collection of articles on NIO (NYSE:NIO) since Could 2022 to warning readers of the numerous headwinds it is dealing with. Undoubtedly, I see all the nice issues that the bulls like about this inventory. Nevertheless, I see even stronger headwinds. For instance, in an article printed in August 2022, entitled “A Easy Actuality Test“, I cautioned readers about its lack of revenue and its unsustainable valuation. The inventory was nonetheless buying and selling at about $21 per share at the moment.

Quick ahead to now, NIO simply launched its Q3 earnings report (“ER”). Its Q3 Non-GAAP EPS (i.e., earnings per ADS) got here in at -$0.30 and missed consensus estimates by $0.14. Car margin was compressed by one other 160 foundation factors to 16.4% in contrast with 18.0% a yr in the past. Its inventory costs plunged 12.4% after its Q3 ER into the single-digit vary ($9.25 as of this writing, earlier than the market open on Nov 10, 2022).

Now wanting forward, I keep my bear thesis. And extra particularly, on this article, I’ll argue that NIO’s inventory costs would stay within the single digits within the close to time period (say the subsequent 1~2 yr or so). I acknowledge its long-term headwinds, together with China’s secular shift in the direction of EVs, its main branding energy, and its aggressive automobile supply plans. However I see the unfavorable catalysts to have the higher hand within the close to time period resulting from a mess of robust headwinds, as detailed subsequent.

Robust supply and high line development

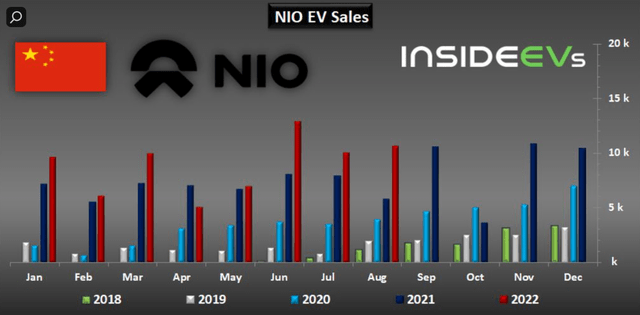

To have a full view, let’s first overview the positives earlier than we dive into the headwinds. NIO enjoys main manufacturing and supply scales amongst China’s home EV gamers. It has demonstrated a strong ramp-up of manufacturing and supply capability previously constantly as you may see from the next chart. particularly, in its September supply report, it supplied the next replace for its 2022 Q3 deliveries, boasting one other quarter of quarterly deliveries and a virtually 30% YoY development fee.

NIO delivered 10,878 autos in September 2022 NIO delivered 31,607 autos within the three months ended September 2022, rising by 29.3% year-over-year and attaining record-high quarterly deliveries Cumulative deliveries of NIO autos reached 249,504 as of September 30, 2022

In its Q3 ER, it reported a complete automobile supply exceeding 10k through the October month, translating right into a 174.3% YOY (however a slight 7.5% decline MOM). And for its This autumn outlook, it goals at a supply goal within the vary of 43k to 48k autos, translating right into a development fee of 71.8% to 91.7% YoY. Complete revenues are projected to develop in tandem 75.4% to 94.2% YOY.

Supply: InsideEVs (NIO)

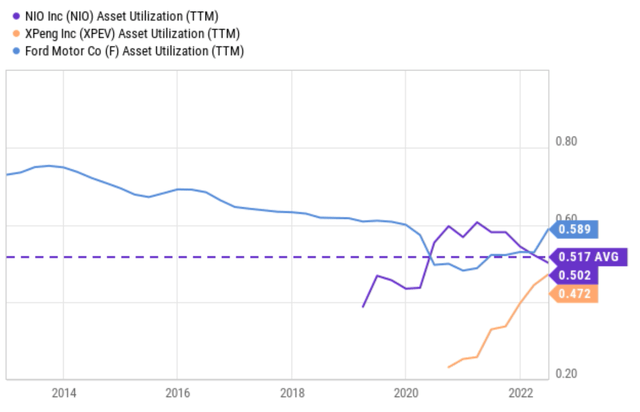

On the similar time, its scale helps it to take care of wholesome operation effectivity as you may see from the next comparability of its asset utilization (“AU”) towards its home peer XPeng (XPEV) and U.S. peer Ford (F). NIO’s AU present stands at 0.50x, barely beneath its long-term common of 0.517x largely because of the lockdowns in China resulting from latest COVID case resurgences. Regardless of the latest decline in its AU, it’s nonetheless above XPEV’s 0.47x and similar to F’s long-term common ranges.

Supply: Searching for Alpha information

Margin strain and lack of revenue

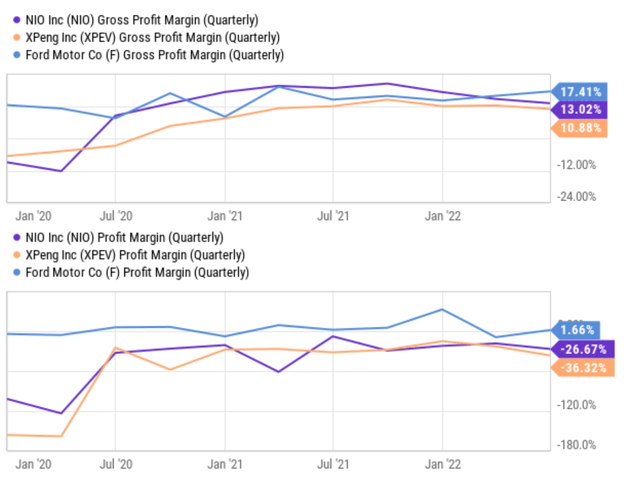

Nevertheless, the enterprise has been struggling margin strain on the underside line and is but to earn a constructive revenue. As seen, its gross revenue margin (“GPM”) peaked round 18% throughout 2H of 2021, surpassing Ford. However lately, the GPM has been beneath strain and contracted to the present stage of 13% by about 500 foundation factors. Now its GPM is decrease than F’s 17.4% by hole (though nonetheless higher than XPEV’s 10.8%). When it comes to revenue margin, as proven within the backside panel, the image is much more regarding. Its internet revenue margin has at all times been within the negatives and is -26.7% at present.

Supply: Searching for Alpha information

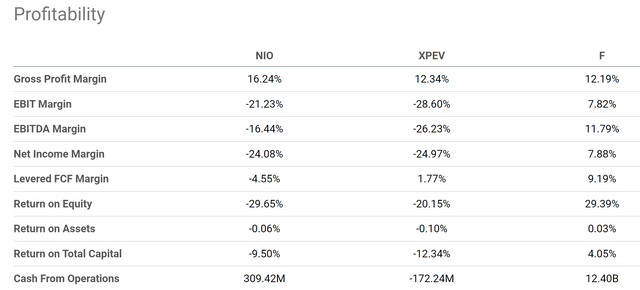

The image doesn’t enhance as we broaden the view to incorporate different metrics as seen within the chart beneath. Its metrics are unfavorable throughout the board starting from EBIT margin, EBITDA margin, and FCF margin.

Trying ahead, I see a number of key headwinds to maintain its earnings within the unfavorable moreover the macroeconomic components resembling political uncertainties and authorities insurance policies. First, I count on the capital necessities to proceed because it pursues the enlargement of charging infrastructures. And notice that its money from operations sat at solely $309M, removed from with the ability to meet such necessities. To fulfill clients’ wants, administration might want to hold spending on each battery swap stations and likewise charging stations. Secondly, I count on a few of its manufacturing issues and likewise the worldwide provide chain disruptions to persist. For instance, it reported early about a difficulty involving the low yield fee of its mega-casting components with its suppliers. This seemingly arcane subject truly can bottleneck its manufacturing ramp-up and effectivity, and it’ll take NIO time to unravel its or discover various suppliers amid provide chain disruptions.

Subsequent, we are going to see that regardless of the shortage of revenue, the inventory remains to be valued at an elevated stage regardless of the big worth corrections.

Supply: Searching for Alpha information

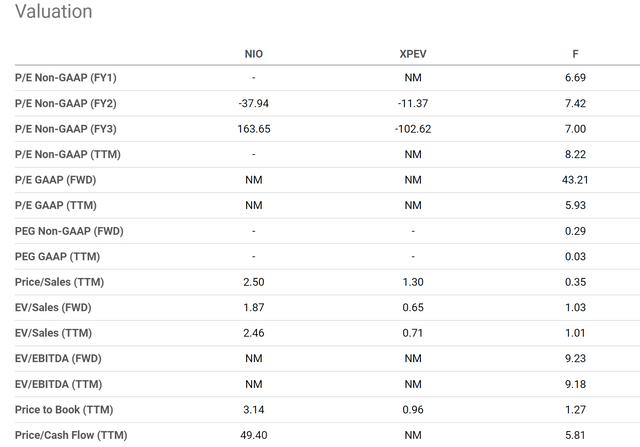

Valuation nonetheless too costly

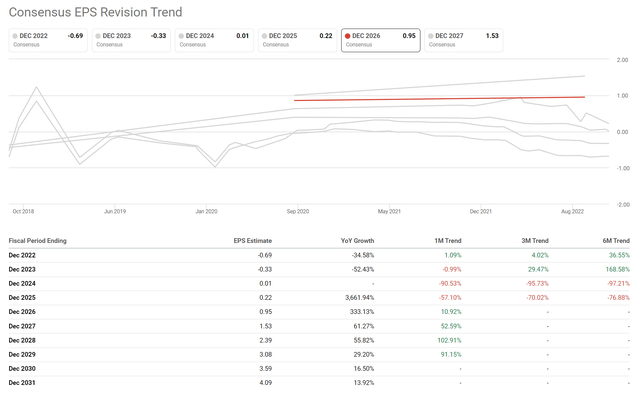

When it comes to valuation, NIO remains to be buying and selling at a big premium each in absolute and relative phrases. Its lack of revenue makes bottom-line oriented metric meaningless as seen within the chart beneath. Even FY3 PE stands at 163x, examine to about 6~7x for F. Moreover, due to the numerous headwinds as analyzed above and its blended Q3 outcomes, its earnings outlook is each bleak and extremely unsure as mirrored within the consensus estimates within the second chart beneath. NIO’s earnings revisions for the final 3 months paint a extremely pessimistic and unsure image. A complete of 11 analysts submitted EPS forecasts, and a complete of 9 analysts revised the EPS downward by as a lot as 70% to 95% in 2024.

Utilizing top-line valuation metrics, its P/Gross sales ratio remains to be at 2.5x regardless of the worth corrections, on par with the S&P 500 index, about 2x larger than XPEV’s 1.3x, and seven.1x larger than F’s 0.35x. I discovered such a valuation unjustifiable given its lack of revenue and the numerous headwinds it’s dealing with. And once more, its topline development is very unsure too as mirrored within the consensus estimates. A complete of 21 analysts submitted income forecasts, and a complete of 17 analysts revised the revenues downward.

Supply: Searching for Alpha information Supply: Searching for Alpha information

Different dangers and remaining ideas

To conclude, in the long run, NIO may gain advantage from the secular shift in China in the direction of EVs, its capability ramp-up, and its robust branding relative to its home friends.

Nevertheless, I see too many robust forces within the close to time period to strain the inventory costs into the single-digit vary. The inventory has but to report a constructive earnings. To this point, it has been trapped within the dreaded vicious cycle: the extra autos it sells, the more cash it loses.

The probabilities of decrease authorities subsidies and insurance policies change may also shift the danger calculus dramatically. The mix of elevated valuation and lack of internet revenue would additionally hold a lid on the inventory costs. China’s Zero Coverage on COVID is one other uncertainty. NIO needed to briefly droop manufacturing at two of its vegetation in Hefei throughout Q3 resulting from native COVID management necessities. And such suspensions are more likely to recur within the close to future. And eventually, the inventory might face the danger of securing new financing as its excessive CAPEX necessities persist whereas its natural earnings stay low or unfavorable.

{kind=link}