zorazhuang

Funding thesis

Agora (NASDAQ:API) has proven resilience within the face of adversity, surviving a crackdown on the educational tutoring sector in China, which as soon as made up nearly all of its income. The corporate has been in a position to make up for the shortfall by rising its income in markets exterior of China. Agora’s elevated funding in R&D, led by its technical founder Tony Zhao, is prone to strengthen its enterprise moat. Tony Zhao has doubled down on Agora and just lately dedicated private funds of US$30 million to share buybacks. That is along with a US$200 million share repurchase program already applied by the corporate earlier this yr. Whereas money stream remains to be unfavorable, Agora’s ample money reserves assure a few years of runway.

Non-financial metrics

Excluding Easemob, energetic prospects had been 2877, a rise of 17.5% yoy. Greenback-based web growth charge (DBNER), which measures the p.c enhance in income from present prospects on a year-over-year foundation, was 130% for US and worldwide prospects and 80% for China prospects. Which means that, on a year-over-year foundation, income from US and worldwide prospects has been growing, whereas income from China prospects has been lowering. Provided that China comprised 70% of income in 2021, it’s no shock then that Agora has had hassle rising income.

Monetary evaluation

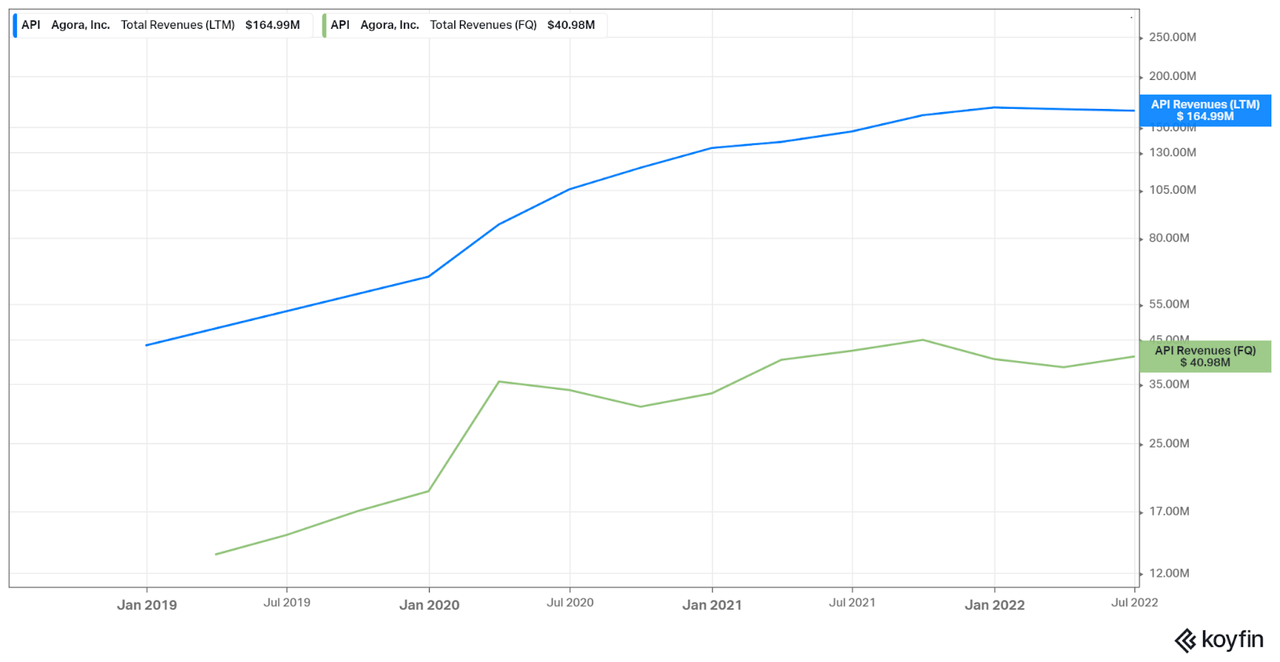

Whereas complete income barely rebounded quarter-on-quarter to US$41 million, the rebound was inadequate to forestall a slight decline on a TTM foundation. Administration attributes this to decreased utilization within the Okay-12 educational tutoring sector in China, which in 2021 made up greater than 70% of all income. The silver lining in that is that future income affect as a result of decreased utilization can be minimal, as income contribution from the Okay-12 educational tutoring sector in China declined to US$1 million in 2022Q2 from US$12 million final yr.

Koyfin

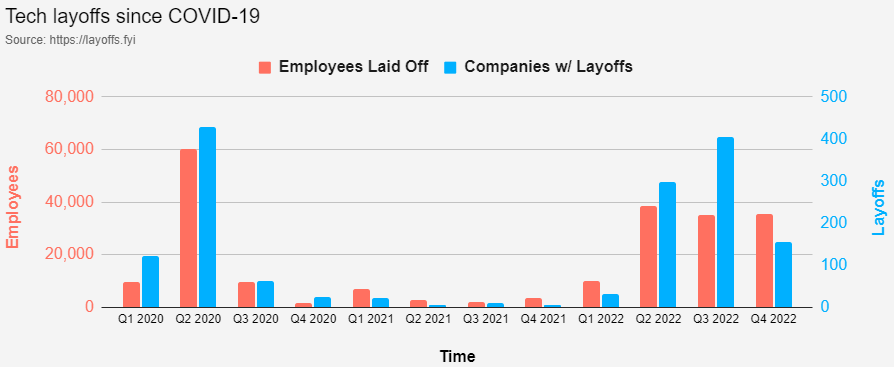

Not like income, working bills have continued to climb. As a proportion of income, quarterly TTM opex reached 126% of income, growing by 6% qoq and 34% yoy. Administration has attributed this to elevated personnel prices in all 3 opex classes. Growing personnel prices run counter to the overall pattern within the tech trade, which has seen growing layoffs for the reason that begin of 2022.

layoffs.fyi

Of the three opex classes, R&D bills elevated essentially the most, reaching 74% of income on a TTM foundation. R&D bills are prone to stay elevated sooner or later, as CFO Jingbo Wang revealed within the earnings name that regular state R&D can be round 30% of income, greater than most SAAS or PAAS companies. Hovering opex contributed essentially the most to web loss, which continued its downward pattern and, at -US$31 million, broke new lows this quarter.

Unsurprisingly, free money stream additionally continued its downward pattern and reached new lows this quarter. Of observe was a US$34.2 million buy of land use rights in Yangpu district, Shanghai for the aim of constructing new headquarters. This was the most important merchandise on the money stream assertion and resulted in an unlevered free money stream of USD -$78.4 million. On the optimistic facet, the corporate has loads of money. Money and short-term investments had been at US$641 million, that means that the corporate is unlikely to expire of money anytime quickly.

Searching for Alpha

Share-based compensation has continued to climb, each completely and as a proportion of income. Share-based compensation as a proportion of income was 4.2% in 2019Q4 however quintupled to 22% in 2022Q2. On a optimistic observe, the corporate has began to step up its share repurchase program, first introduced in Feb 2022.

Searching for Alpha

Repurchase of widespread inventory elevated to USD $12.2M from USD $7.6M final quarter. Apparently, founding CEO Tony Zhao just lately introduced that he would use his private funds to purchase as much as USD $30M value of peculiar shares, signaling the CEO’s perception that the corporate’s present share costs are undervalued.

Valuation

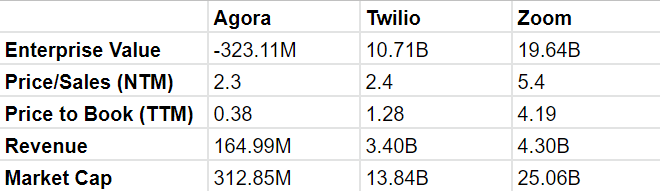

We examine Agora to Twilio (TWLO) and Zoom (ZM), two tech corporations that present comparable companies, to get a way of the way it ought to be valued. Agora’s enterprise worth (EV) is USD -$314M, as a result of money holdings drastically exceeding the sum of its market capitalization and complete debt. Thus, we’ll have a look at Agora’s worth/gross sales ratio as an alternative of its EV/gross sales ratio.

Writer

In comparison with Twilio and Zoom, Agora appears to be the extra enticing funding. Its worth/gross sales and price-to-book ratios are the bottom of the three corporations, at 2.3 and 0.38 respectively. Searching for Alpha’s Quant Issue Grades additionally thinks favorably of Agora’s current valuation, assigning it an A+ score. An necessary caveat right here is that Agora’s income and market cap are magnitudes decrease than these of Twilio and Zoom.

Dangers

Weak Macro Atmosphere

Within the US, Fed rate of interest hikes have battered the inventory market. For the reason that final Fed assembly, futures merchants have raised expectations for the terminal charge to achieve 5%. Powell communicated clearly that there wouldn’t be any dovish pivot within the foreseeable future, because the unemployment charge had not risen and the expansion charge had not fallen beneath pattern. Expectedly, inventory markets tanked after Powell’s announcement. Whereas the inventory market rallied final Friday following a dovish CPI print, extra ache could also be lurking across the nook, because the treasury yield-curve inversion reached a four-decade excessive, signaling a attainable recession.

In China, the place Agora derives greater than 70% of its income, inventory markets rallied on information of COVID easing. The information got here as China reported greater than 5000 new, regionally transmitted instances, the best quantity since Could 2, when the nation’s business capital of Shanghai was put underneath a crushing lockdown. Nonetheless, the Chinese language financial system continues to be underneath strain, with its property market, the most important asset class on the earth, persevering with to underperform. Repeated lockdowns throughout China’s main cities have disrupted provide chains and dampened shopper spending. City unemployment stays at traditionally excessive ranges, growing to five.5% in September 2022 from 5.3% in August.

In Europe, the probability of a recession continues to rise. Eurozone composite PMI fell to a 23-month low of 47.3 in October, with new orders and future output PMIs suggesting that worse is but to come back. Based on Eurostat, inflation is predicted to achieve a file excessive of 10.7% in October, pushed primarily by vitality costs, which have risen greater than 40% year-on-year. Eurozone GDP development is predicted to be unfavorable between 2022Q3 and 2023Q1, and stagnant in 2023.

Delisting

Delisting stays a danger for Agora, having been added to the conclusive listing of issuers recognized underneath the HFCAA in Could 2022. Nonetheless, Agora’s probability of being delisted has been considerably diminished since China agreed to let PCAOB inspectors audit Chinese language corporations listed on US Exchanges. Moreover, Agora may observe within the footsteps of NIO and listing by the use of introduction on the HKEX. Doing so would scale back the liquidity affect of delisting, since US ADRs and Hong Kong shares are totally fungible. Nonetheless, the liquidity affect of delisting wouldn’t be utterly eradicated, given the big distinction in liquidity between the Hong Kong and US inventory markets.

Conclusion

We like the truth that Agora has been profitable at recovering misplaced income from the educational tutoring sector in China. Provided that the sector solely contributed USD $1M in 2022Q2, we consider that Agora’s income decline (on a TTM foundation) will quickly reverse. Whereas Agora’s free money stream continues to worsen, its money balances are greater than enough to supply a few years of runway. Agora’s rising opex has been primarily as a result of elevated funding in R&D which, given CEO Tony Zhao’s technical background, ought to enhance its enterprise moat over time.

Then again, we don’t like the truth that Agora has been more and more passing on prices to traders within the type of elevated SBC. Moreover, the macro atmosphere is weak within the US, Europe, and China. Within the US, a current dovish CPI print weakened the Fed’s resolve, and the implied terminal charge stays just below 5%. In China, a brand new wave of COVID outbreaks threatens to set off a recent spherical of lockdowns. Within the Eurozone, excessive inflation and low PMIs counsel that development is prone to be unfavorable in 2023.

Within the subsequent few quarters, we wish to see the 130% DBNER for US and worldwide areas translate into income development. We’d additionally prefer to see SBC and opex development sluggish or cease utterly. Till then, we assign a maintain score to Agora.

{kind=link}