golfcphoto

By Tracy Chen, CFA, CAIA

In a 12 months of nowhere-to-hide amid rate of interest shocks, the worldwide fastened revenue market has cheapened considerably. Nevertheless, with recession dangers looming in 2023, buyers should tread rigorously to keep away from credit score landmines. We at present see a number of engaging alternatives with cheaper valuations and minimal credit score dangers in high-quality company residential mortgage-backed securities (RMBS), company industrial mortgage-backed securities (CMBS), and AAA non-agency CMBS.

1. Company Mortgage-Backed Securities (MBS)

Mortgage charges have topped 7%, the very best since 2000, eliminating the chance for many present loans to refinance. On the similar time, housing affordability has deteriorated sharply. The housing market will decelerate drastically. Nevertheless, the tail threat in housing is way lower than the International Monetary Disaster (GFC). The present ranges of the housing market ought to stay supported by the dearth of provide, wholesome family steadiness sheets, and the dearth of distressed gross sales—a notable distinction to the GFC.

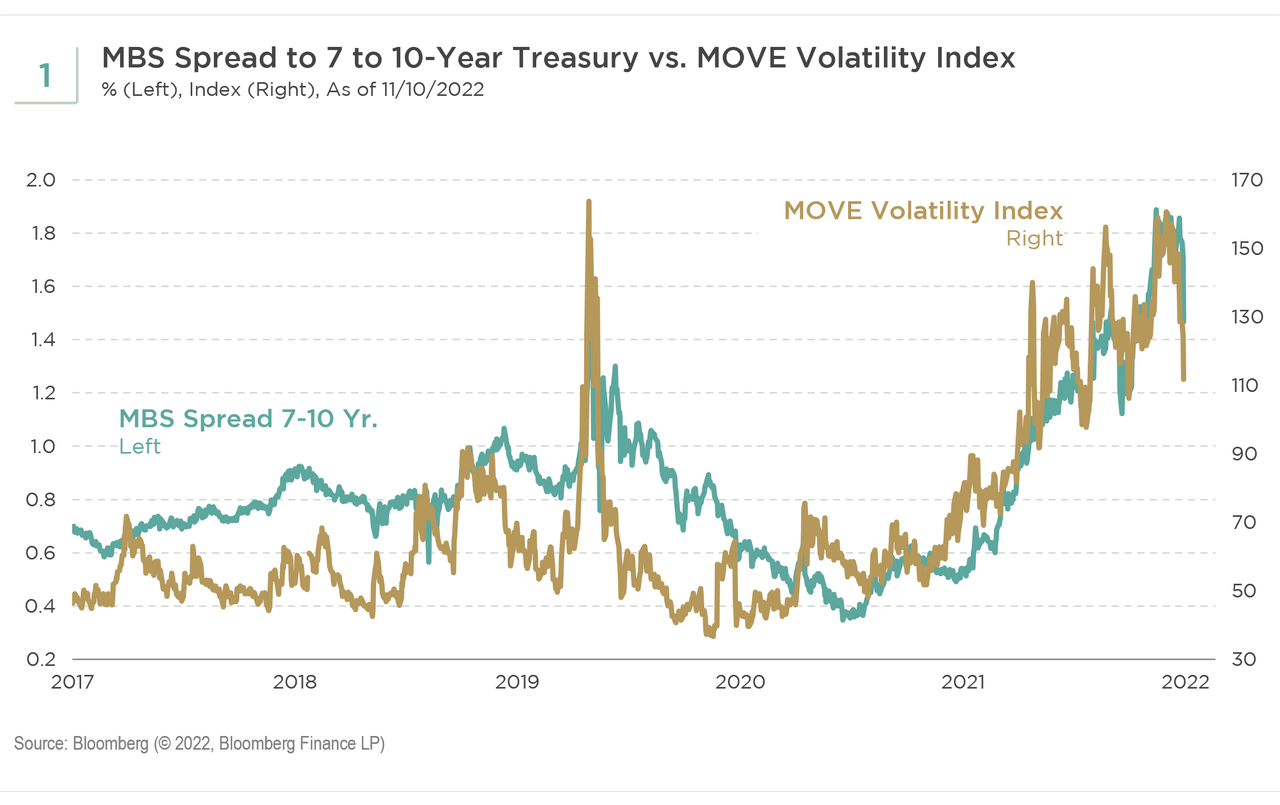

An MBS funding comes with an embedded brief on prepayment choices, therefore its unfold to Treasury bonds has a constructive correlation with curiosity volatility (see Determine 1). Pushed by charge volatility and exit of the most important purchaser, the Federal Reserve (Fed), mortgage spreads are as soon as once more on the widest of the post-GFC interval, and MBS valuations are very engaging. We imagine the heightened rate of interest volatility ought to peak, which ought to bode effectively for MBS. Moreover, convexity is close to the very best ranges because of the out-of-money standing. MBS are infamous for his or her detrimental convexity, however now given the excessive rate of interest, the convexity is the least detrimental.

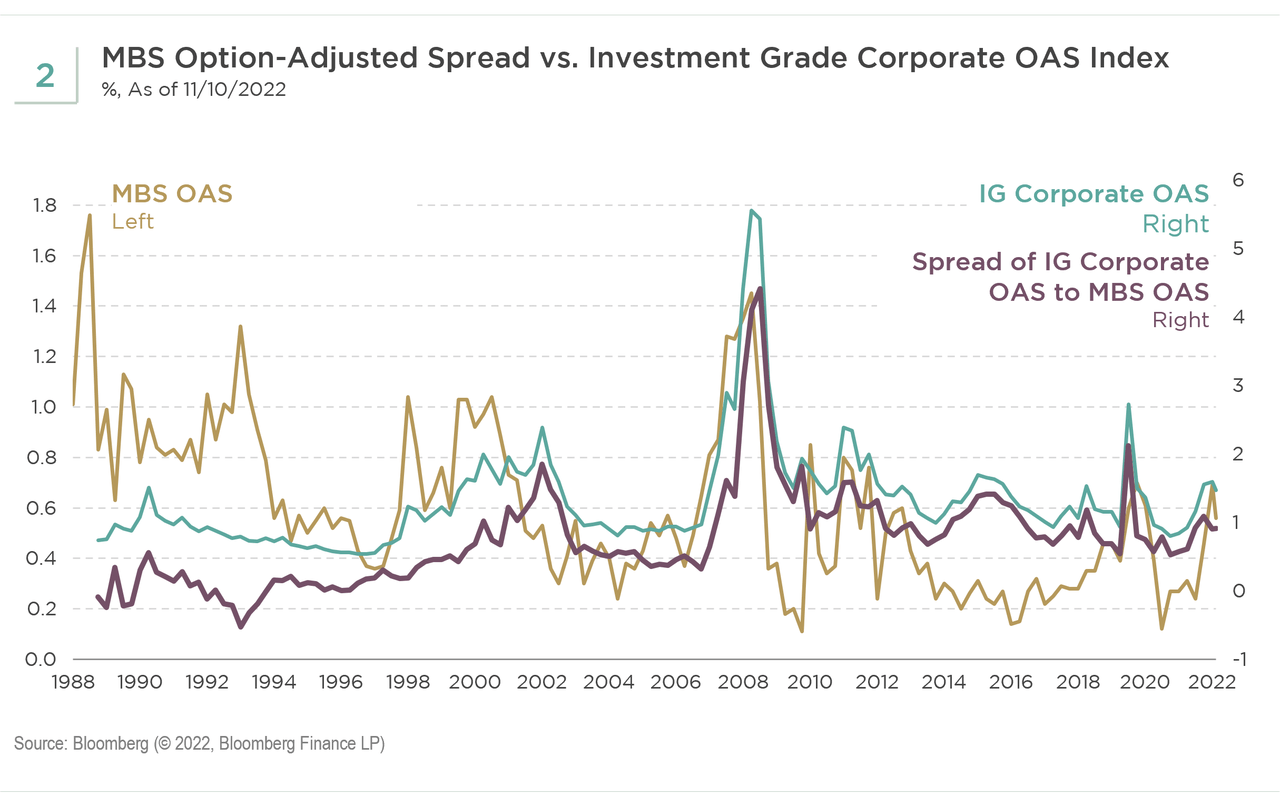

The widening in mortgage spreads has considerably outpaced the widening in funding grade (IG) company spreads this 12 months. Consequently, IG corporates’ pickup in unfold relative to MBS (purple line) is near the post-GFC tight, in comparison with the IG company option-adjusted unfold (OAS) (teal line) and MBS OAS (gold line) (see Determine 2).

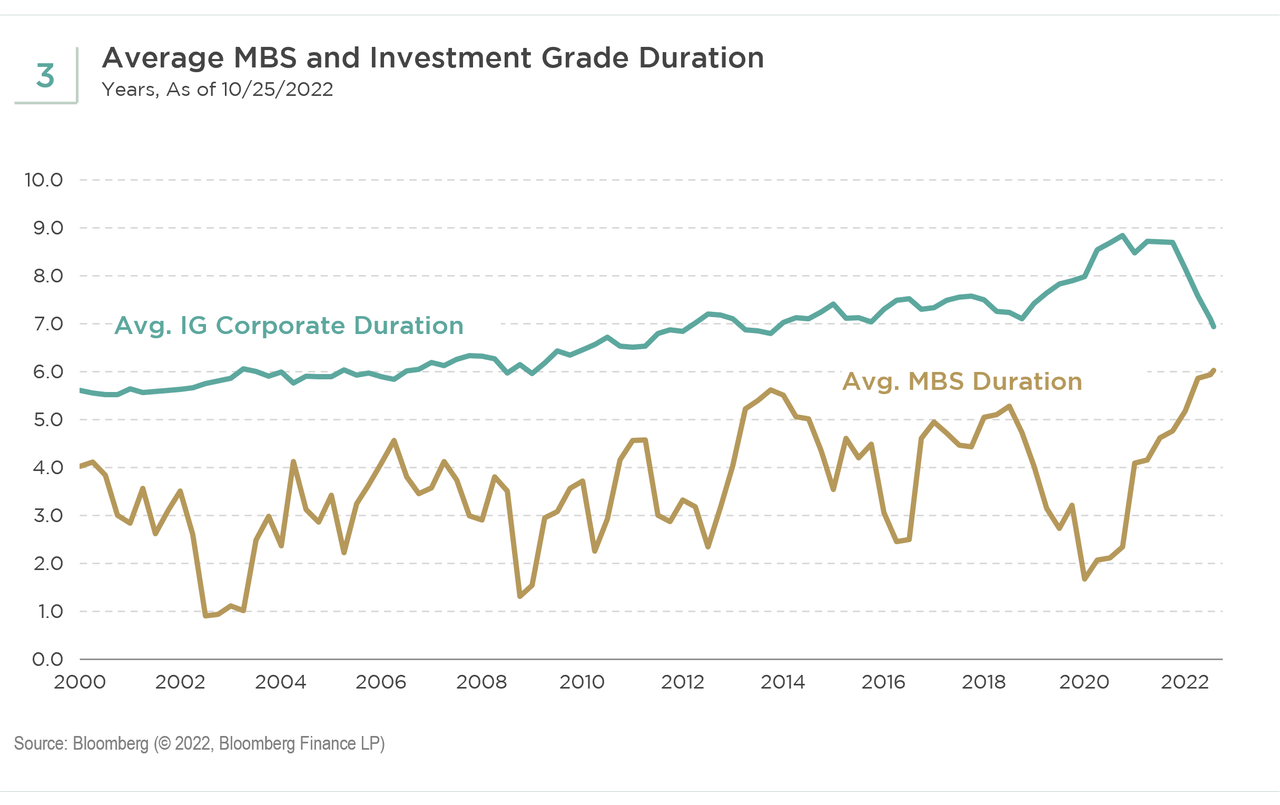

Basically, excessive mortgage charges put roughly 99% of debtors out of cash to refinance, extending the MBS length to its historic excessive of over 6 years (gold line) (see Determine 3). On the similar time, the length for IG company bonds fell beneath 7 years (teal line). Due to this fact, if we needed to seize the unfold tightening transfer, MBS is at much less of an obstacle versus IG corporates from the length perspective.

Lastly, we’ve got more and more noticed a extra favorable market technical. Difficult housing affordability inevitably reduces housing exercise and mortgage origination, therefore much less MBS provide. On the similar time, engaging valuation meets with the primary indicators of inflows into MBS funds. With this mentioned, there’s nonetheless some uncertainty in demand from the Fed, banks, overseas patrons, cash managers, REITS, and government-sponsored enterprises (GSE), like Freddie Mac and Fannie Mae.

2. Company Business Mortgage-Backed Securities (CMBS)

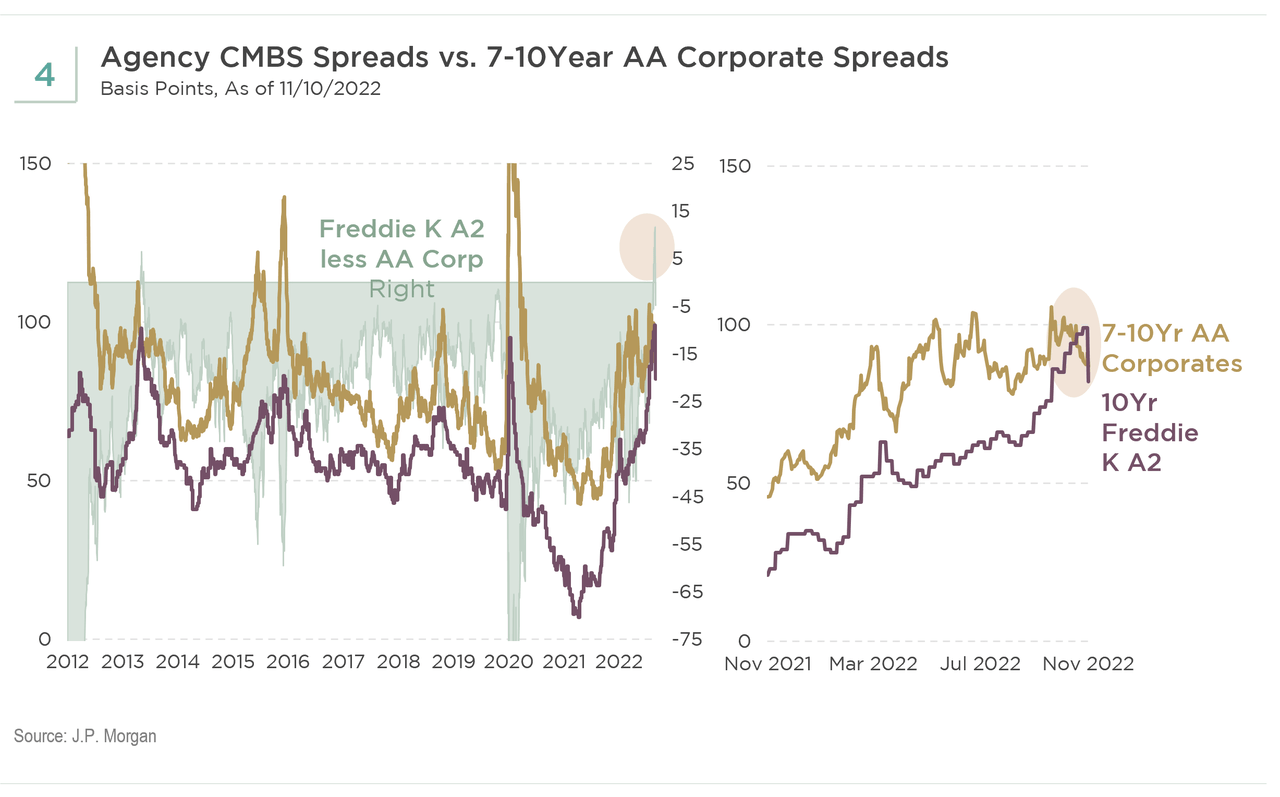

Authorities assured company CMBS with name safety at the moment are cheaper than 7 to 10-year AA company bonds, a uncommon case in historical past (See Determine 4).

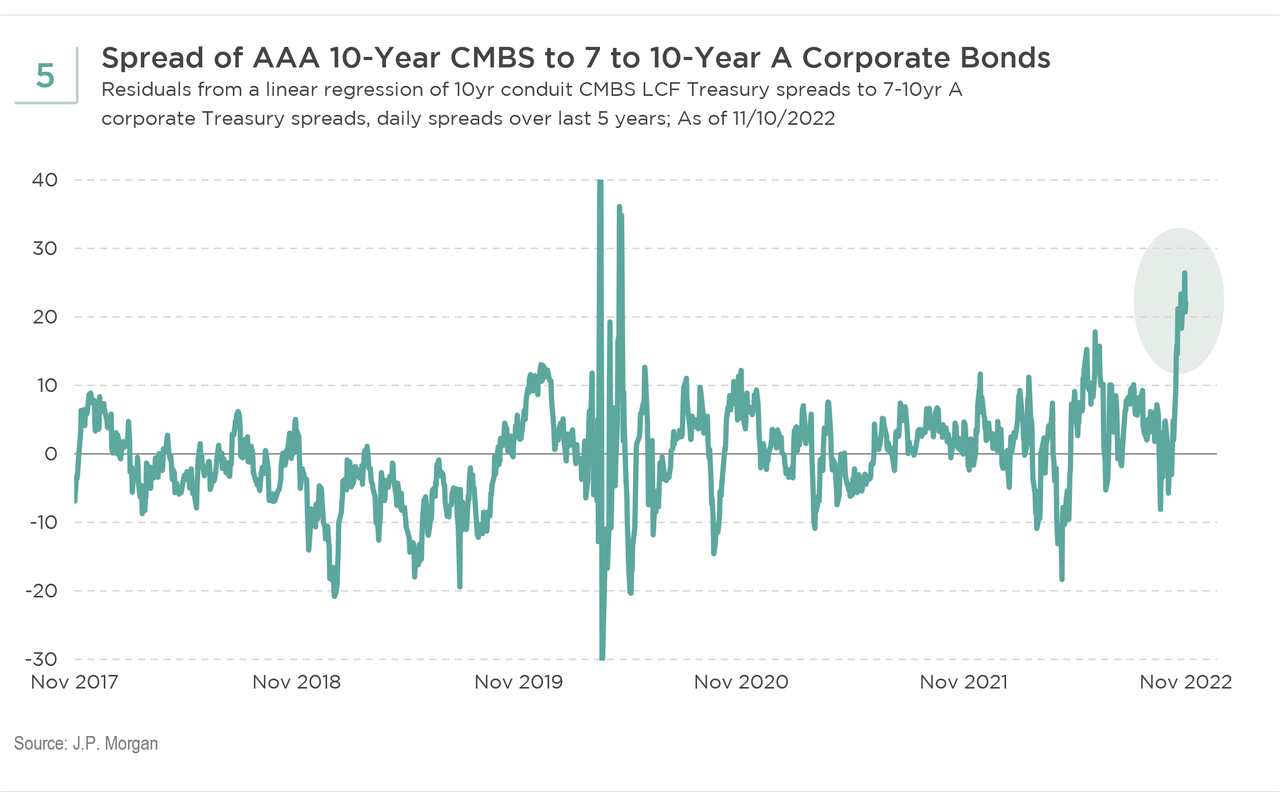

3. Non-agency CMBS

Presently, AAA-rated conduit CMBS look cheaper than comparable length single-A company bonds (See Determine 5).

There are additionally engaging alternatives in different AAA-rated sectors like AAA collateralized mortgage obligations (CLO), AAA non-qualified mortgage securities, AAA subprime auto asset-backed securities (ABS), IG-rated credit score threat transfers (CRT), and so on. Traders with bigger threat appetites can also discover alternatives in BBB or equal CLO, CMBS, or CRT, which supply double-digit yields that assist compensate for the credit score dangers.

It’s almost unattainable to time the market bottoms precisely, and the above property can nonetheless get cheaper if the Fed overtightens and Treasury charges climb considerably increased from right here. Nevertheless, we expect these structured credit score investments ought to repay over the medium to long run.

Conclusion

With high-quality structured credit score having cheapened a lot, we don’t must take extreme credit score threat to realize respectable returns. As recession threat looms in 2023, we imagine these structured credit score sectors ought to outperform throughout an financial downturn with minimal credit score dangers. Traditionally large spreads compensate for a lot of dangers. We imagine buyers ought to take into account making the most of these alternatives and the potential for engaging long-term returns.

Unique Submit

Editor’s Notice: The abstract bullets for this text had been chosen by Looking for Alpha editors.

{kind=link}