filo/E+ by way of Getty Pictures

Funding Thesis

Because of the a number of CEO modifications over the previous few years, it’s evident that Petróleo Brasileiro S.A. – Petrobras (NYSE:PBR) (NYSE:PBR.A) is in additional for uncertainties forward. As with predecessors, the President-elect Luiz Inacio Lula da Silva will set up a brand new administration staff over the following few months, but once more, triggering extra sweeping modifications throughout the board. The one most keenly watched would be the firm’s dividend technique, for the reason that new President has been most vocal about his intention to minimize dividend payouts.

As highlighted in our earlier article, PBR’s LTM dividend yield of 38.11% was not sustainable, as a result of lately moderated oil/fuel costs and rising political threat. Now that the inventory has retraced by a tragic -36.81% from the current highs, is it a safer purchase now? Properly, it is dependent upon particular person buyers, actually.

PBR will stay underneath state management for the foreseeable future, with any hopes for privatization completely dashed certainly. So, one should perceive that sudden administration and coverage rehaul will stay a standard incidence for the corporate. Then once more, these dangers may be buttressed by the candy dividend yields of roughly 31.1% in FY2023 and 12.9% in FY2024, made even sweeter after the Lula low cost. Due to this fact, highlighting the inventory’s suitability for these with larger threat tolerance and eager eye for short-term advantages. No ache, no acquire, certainly.

PBR’s Dividends Will Be Reduce, However Nonetheless Improved From Pre-Pandemic Ranges

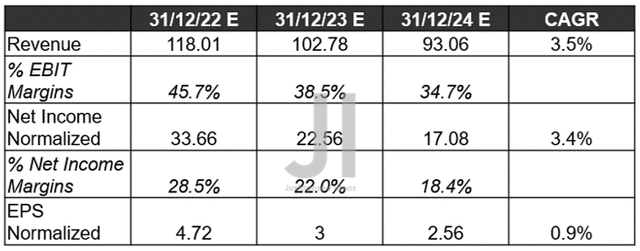

PBR Projected Income, Internet Revenue (in billion $) %, EBIT %, and EPS

S&P Capital IQ

Regardless of the painful inventory plunge over the previous few weeks, it’s obvious that Mr. Market has quietly upgraded PBR’s prime and backside line by 3.73% and 9.21% via FY2024, respectively, since our earlier evaluation in July 2022. Thereby, bettering its EBIT and web earnings margins to 34.7% and 18.4%, in comparison with FY2019 ranges of 23.4% and 12.2%, respectively. Consequently, we could probably witness adj. EPS of $2.56, indicating a straightforward doubling in its profitability since FY2019.

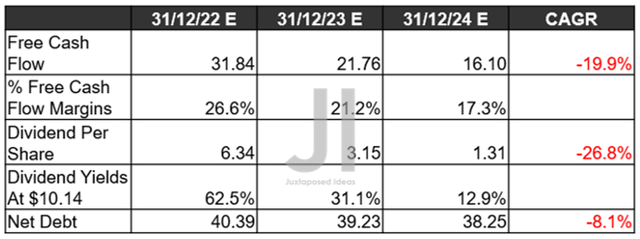

PBR Projected FCF (in billion $) %, Money owed, and Dividends

S&P Capital IQ

Within the quick time period, PBR’s dividends stay protected, for the reason that Brazilian Federal Court docket has blocked the prosecutors’ movement to droop the $8.5B in dividend payouts for FQ3’22. Barring any main political upheaval, we anticipate the corporate to proceed paying a beneficiant a part of its Free Money Movement (FCF) technology as dividends from FQ4’22 onwards, roughly at 30% versus the present 60%, as witnessed throughout Lula’s earlier Presidency between 2003 and 2010.

Moreover, PBR is predicted to nonetheless report wonderful FCF margins of 17.3% by FY2024, regardless of the supposed larger capital expenditure in direction of renewable power and oil refineries underneath Lula’s administration. Not too unhealthy certainly, although notably decrease in comparison with FY2019 ranges of twenty-two.4% and FY2021 of 37.3%.

Due to this fact, analysts predict PBR’s dividends to be minimize by -50.31% by FY2023 and one other -58.41% by FY2024. Nonetheless, $1.31 per share is nothing to sneeze at, for the reason that quantity signifies a greater than respectable yield of 12.9% primarily based on present share costs of $10.14. In any other case, a superb 15.41% yield if the inventory continues to fall to $8.5 over the following few weeks. We’ll see, since issues stay unsure till the Fed really pivots and terminal charges freeze.

Within the meantime, we encourage you to learn our earlier article, which might allow you to higher perceive its place and market alternatives.

Petrobras: Extra To Fall – Extra Political Danger Than Ever

So, Is PBR Inventory A Purchase, Promote, or Maintain?

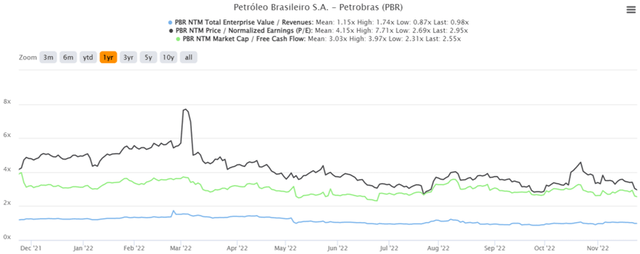

PBR YTD EV/Income and P/E Valuations

S&P Capital IQ

PBR is at present buying and selling at an EV/NTM Income of 0.98x, NTM P/E of two.95x, and NTM Market Cap/FCF of two.55x, nearer to its YTD low of 0.87x, 2.69x, and a couple of.31x, respectively. The inventory can also be buying and selling at $10.14, down -37.86% from its 52 weeks excessive of $16.32, nearing its 52 weeks low of $9.56.

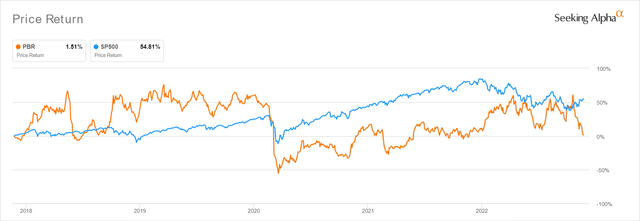

PBR 5Y Inventory Worth

Looking for Alpha

Nonetheless, it’s unattainable to disregard the cyclical nature of the oil/fuel shares, given the tip of this supercycle by the tip of 2022, as additionally witnessed in the course of the begin of the pandemic. Crude oil costs have continued to average to $77.51 on the time of writing, in comparison with $123.70 in early March, $122.11 in mid-June, and $92.61 in early November 2022. Market analysts are additionally predicting that spot costs will fall additional to the low $70s via 2024, indicating the tip of war-driven oil heydays, although nonetheless at a notable premium from the pre-pandemic common of $60s. Mixed with PBR’s rising political threat, the inventory is certainly speculative and solely appropriate for many who are on the lookout for short-term features.

Nonetheless, PBR additionally appears extra engaging at present blood-bath ranges with an improved margin of security now. Assuming that market analysts had been proper, the corporate can also be anticipated to disburse wonderful dividend yields of 31% over the following few quarters. Thereby, negating a number of the political headwinds, since it might take a while for these administration modifications to be carried out anyway. Due to this fact, we’re re-rating the PBR inventory as a speculative Purchase now, although portfolios must also be sized appropriately, since we are going to expertise extra volatility within the quick time period.

{kind=link}