Marcin_P_Jank

Within the waning days of 2021, I wrote the article 3 Greatest Lengthy-Time period Shares For Traders In 2022 recommending AbbVie (NYSE:ABBV), VICI Properties (NYSE:VICI), and Google-parent Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL).

It is time for an replace with 2022 drawing to a detailed. My apologies prematurely for the size of the article (I do know you are busy!), I reduce the place I may, however I wished to incorporate all of the crucial data.

Time really flies, and it is exhausting to consider almost a 12 months has handed. On the similar time, a lot has occurred that it is powerful to consider all of it occurred in just one 12 months. Time is an interesting phenomenon.

Many traders will likely be glad to see 2022 within the historical past books, however I’m wondering if I’m one among them. I’m far more snug constructing long-term positions on this market than in 2021.

The drop has offered a terrific probability to open new positions like Adobe (ADBE) and reinitiate others, like Cloudflare (NET). There have additionally been incredible possibilities so as to add to holdings like Texas Devices (TXN) and common down in others, like CrowdStrike (CRWD).

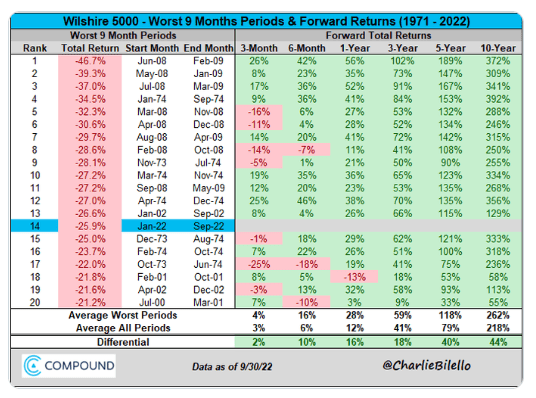

A number of respected research present that traders underperform the market by attempting to time it. This occurs as a result of lacking just some of the market’s greatest days crushes long-term returns. And lots of of as of late come once we would least count on them – inside a number of weeks of the worst days. Returns following a bear market are usually glorious for long-term traders, as proven beneath.

Compound Advisors

Greenback-cost averaging is a wonderful technique. So is setting restrict orders on favourite shares on the desired worth and decrease intervals in growing numbers of shares. The benefits are that you just get your worth after which leverage it down. The disadvantages are that the inventory could not drop to the specified worth and that it takes endurance.

Now again to the enterprise at hand.

Let’s evaluation the state of affairs in late 2021.

Rates of interest had been nonetheless close to zero, inflation was close to 7%, Russia hadn’t invaded Ukraine, many people had been nonetheless beneath COVID-19 masks mandates, and the Nasdaq (QQQ) was close to 16,000 when the article was written. Oh, and Elon Musk hadn’t even began the Twitter rumblings.

Nonetheless, the writing on the wall was coming into focus, so two of the three suggestions centered on profitable dividends reasonably than progress. This labored out tremendously nicely. Then again, I anticipated Alphabet to climate the tech storm a lot better than it did. Now Google is going through extreme headwinds in promoting and cloud providers, and it is determination time.

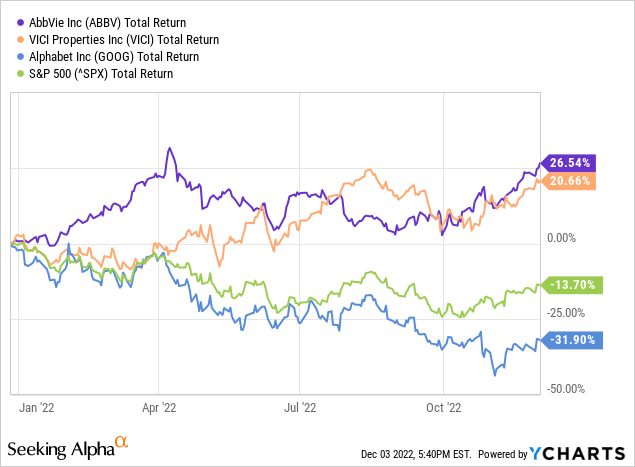

The result’s two excellent performers and one large disappointment, as proven beneath.

AbbVie and VICI outperformed the S&P500 by 40% and 34%, respectively, whereas Alphabet lagged by 18%.

My final article centered on the success of AbbVie and Alphabet’s downfall, however VICI deserves among the limelight, so let’s begin there.

VICI defies the REIT crumble: Is it nonetheless a purchase?

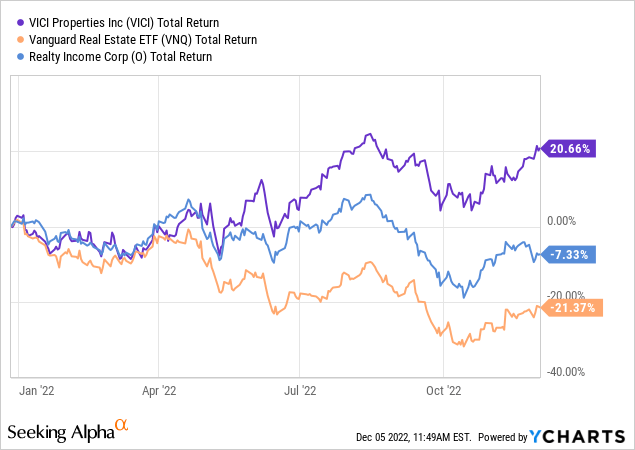

Actual property funding trusts (REITs) have had a tough time in 2022 as rising rates of interest have prompted traders to flee. However no less than one has thwarted the development massively.

VICI Properties has outperformed the Vanguard Actual Property ETF (VNQ) by over 40% for the reason that article’s publishing date. As proven beneath, even the very best high quality REITs, like Realty Revenue Corp (O), have struggled.

What separates VICI?

VICI is among the world’s largest on line casino and leisure property holders. Its possession of “trophy properties” like Caesars Palace, The Venetian and Palazzo, Mandalay Bay, and quite a few different one-of-a-kind areas units it aside.

VICI is considerably shielded from inflation resulting from computerized lease escalators tied to the buyer worth index (CPI) – rents improve mechanically when inflation is excessive. Lots of the will increase are capped, typical of rental agreements; nonetheless, 47% are uncapped.

Some may marvel if proudly owning leisure properties heading right into a recession is dangerous. VICI collected lease and even raised dividends in the course of the worst pandemic on line casino closures in 2020. Investing within the landlord just isn’t the identical as investing within the casinos themselves. In reality, VICI has reported 100% lease assortment because it was shaped in 2017.

What occurred in 2022?

-The accretive acquisition of MGM Progress Properties was accomplished in Q2 2022, which solidified the portfolio. In whole, VICI holds 44 properties in 15 states.

-VICI joined the S&P 500 index in June.

-Achieved investment-grade debt scores from all three main companies.

-Adjusted funds from operations (AFFO) rose 57% YOY by means of Q3 2022 and 83% YOY in Q3. Nonetheless, the share depend additionally rose significantly to finance acquisitions. AFFO per diluted share is marginally increased this 12 months. It’s important to look at AFFO on a per-share foundation with REITs.

Is VICI nonetheless a purchase?

VICI’s dividend is the secret. The dividend has risen 8% compounded yearly for the reason that firm’s creation and eight.3% this 12 months. The share worth rise has pushed the yield down close to latest historic lows, as proven beneath.

In search of Alpha

VICI nonetheless wants progress, and the plan has a number of initiatives. VICI has a fund that gives capital to tenants for enlargement. Principally, VICI offers cash for the tenant to increase after which collects lease on the event, which VICI owns. An instance is the Century Casinos deal simply introduced.

The corporate additionally appears at gaming alternatives overseas and non-gaming properties within the U.S., like golf programs and resort lodges.

The dividend is protected as VICI hovers close to its focused payout ratio of 75% of AFFO. The corporate’s debt is 100% fastened fee with a median of seven years to maturity. That is very important, with curiosity rising quick this 12 months.

In brief, VICI is a terrific car for a strong and rising yield; nonetheless, near-term share worth will increase could possibly be muted, barring a big acquisition.

For my cash, VICI Properties is now a strong maintain.

Can AbbVie preserve crushing the market?

AbbVie made the highest choose listing due to its fascinating yield and resilience to an financial downturn. Prescribed drugs outperform throughout market turmoil as a result of their merchandise are typically not luxuries. As predicted, traders flocked to AbbVie as a haven this 12 months.

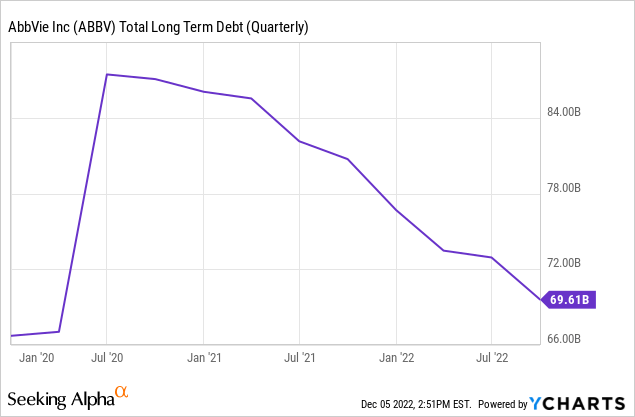

Revenues by means of Q3 rose 4% to succeed in $42.9 billion. Money from operations fell 1% to $17.5 billion. In the meantime, administration continued to aggressively pay down debt taken on in 2020 when the corporate acquired Allergen, as proven beneath.

The acquisition continues to repay with important positive factors in gross sales from Botox Beauty (+23%), Botox Therapeutic (+12%), Vraylar (+19%), and regular gross sales of Juvederm.

What concerning the Humira biosimilar risk?

AbbVie’s blockbuster drug, Humira, may have competitors within the U.S. from biosimilars beginning in 2023.

The gross sales positive factors above are crucial to filling the hole that will likely be left as soon as biosimilars for Humira hit the market. Judging by the decline in gross sales internationally, the place biosimilars are already out there, Humira gross sales will probably be reduce in half inside three years. This will likely be an enormous blow; nonetheless, administration has made important strides to handle the problems.

As not too long ago as Q1 2020, Humira accounted for 55% of whole income. This was all the way down to 38% in Q3 2022. In the meantime, mixed Skyrizi and Rinvoq gross sales rose 68% by means of Q3 2022 to $5.3 billion. AbbVie has confirmed steering of $15 billion in gross sales from these two by 2025. All advised, the corporate is on observe to interchange misplaced Humira gross sales.

Is AbbVie nonetheless a purchase?

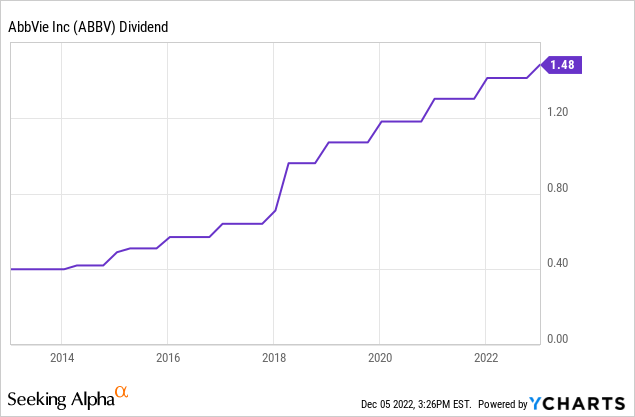

Like VICI, AbbVie’s important draw is the protected and rising dividend. AbbVie has raised the dividend every year since its inception, as proven beneath.

Shareholders acquired a modest 5% increase this 12 months.

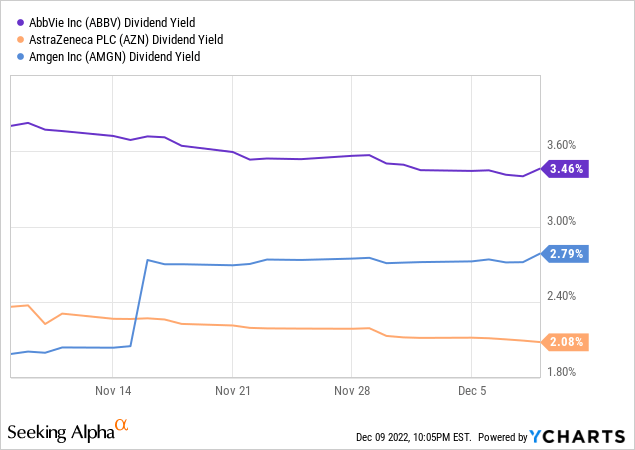

Principally, shareholders get a strong inventory that’s not vulnerable to wild downswings and a protected yield that opportunistic traders can snag over 4%. The yield is increased than opponents like Amgen (AMGN) and AstraZeneca (AZN) due to the priority over Humira, as proven beneath.

AbbVie’s common yield in 2021 was 4.5%, down to three.7% this 12 months due to the share worth improve. Wall Avenue is beginning to consider the corporate will thrive even with the Humira cliff.

AbbVie stays a rock-solid choose for constant returns; nonetheless, it’s far more engaging above a 4% yield. Because of this, I think about the inventory a maintain till the worth drops beneath $150 per share.

Google: Common down or reduce losses?

Google inventory has been slaughtered this 12 months, falling greater than 30%. Income progress has been acceptable, however controlling prices has confirmed tough.

The way in which I see it, long-term traders have two affordable selections: persist with Google inventory by averaging down (buying extra inventory at a lower cost to scale back the fee foundation) or reduce losses and make investments elsewhere.

There are convincing arguments on each side, so it will likely be enjoyable and hopefully informative to make every case and see which is extra highly effective.

Level: Traders ought to persist with Alphabet – and purchase extra whereas it slumps.

1. Everyone knows that gross sales progress like we noticed in 2020 and 2021 would not final without end, however Alphabet continues to be rising. Gross sales are up greater than 13% YOY thus far in 2022.

2. Working revenue is powerful at $57 billion by means of Q3 – matching final 12 months’s whole regardless of document inflation. Working money circulation elevated barely, reaching $68 billion on a 33% margin. Occasions are powerful, however this is not precisely a crumbling enterprise.

CEO Sundar Pichai has disclosed the objective of turning into 20% extra environment friendly, which is welcome information.

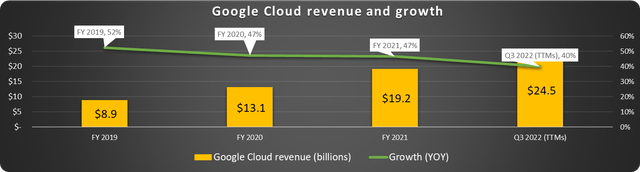

3. Google Cloud has made large strides in rising gross sales, as proven beneath.

Information supply: Alphabet. Chart by creator.

Income has almost tripled since 2019, and this phase nonetheless has large potential. It trails solely Amazon Net Companies (AMZN) and Microsoft Azure (MSFT) in market share.

4. The steadiness sheet is rock strong. Alphabet has $166 billion in present belongings in opposition to simply $66 billion in present liabilities and solely $14.5 billion in long-term debt (a piddly 1% of the present market cap).

5. Lastly, essentially the most compelling motive to extend holdings at these ranges is the indispensability of Google Search. Google Search is so pervasive that Google is now a verb. Severely, it is listed in Merriam-Webster’s dictionary. Advertisers know they should be on web page one, which provides Alphabet great pricing energy.

Counterpoint: It is time to promote Alphabet inventory.

1. Bills are ballooning quicker than income as a result of administration just isn’t controlling prices.

The corporate elevated its headcount by 24% within the final 12 months from 150,000 to almost 187,000. Sadly for workers, layoffs could also be so as now. Hiring and onboarding are costly, and this appears like poor foresight.

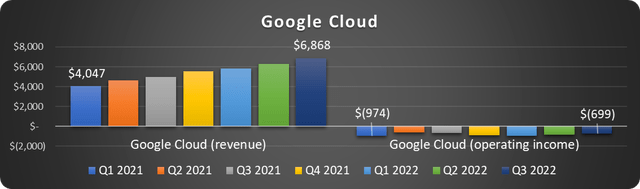

2. Certain, the Google Cloud phase is rising, however it’s a significant cash pit. I’ve written about this intimately right here. Whereas Amazon is raking in money from AWS, Alphabet has misplaced $15.8 billion from the Google Cloud phase operations since 2019.

I’ve shared beneath latest income progress juxtaposed with the continued working losses.

Information supply: Alphabet. Chart by creator.

Gross sales progress will additional gradual in 2023 if latest business outcomes are indicative.

3. 2023 may see advertisers make sizable price range cuts, additional chopping into progress and income. That is almost a given, and it will likely be as much as administration to streamline operations. They have not confirmed this skill but.

What we in the end do is determined by perception in administration, time-frame, and danger urge for food. I added modestly at $85.50.

All in all, 2022 was a irritating 12 months. But there have been successes like AbbVie and VICI. Bear markets may be terrific for long-term traders to arrange great future income. Keep in mind to dollar-cost common, give attention to the lengthy haul, and preserve a snug danger profile.

Look ahead to 2023 picks coming quickly!

{kind=link}