Nikola Stojadinovic/E+ through Getty Photos

During the last yr, Nikola (NASDAQ:NKLA) turned across the enterprise transferring away from their fraudulent previous to truly producing BEV heavy-duty vehicles. The inventory grew to become fascinating because of the alternative forward, however traders have been warned to observe for optimistic developments on truck orders and capital raises earlier than diving into the inventory. My funding thesis stays Impartial on the inventory because of the lack of progress on said objectives.

BEV Delays

Nikola reaching manufacturing on the BEV Tres was an exceptional accomplishment after the founding CEO was discovered to have dedicated fraud. The corporate really promoting the vehicles has been a far totally different story because the sector shortly grew to become crowded with Tesla (TSLA) delivering their Semi truck to PepsiCo (PEP) at first of the month.

The most important query was whether or not Nikola had something proprietary and the shortage of orders would recommend in any other case. The hydrogen EVs have a much more compelling story, if not for the inventory valuation and capital wants.

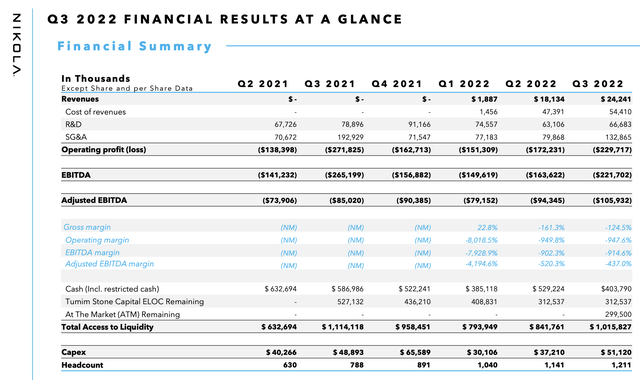

For Q3’22, Nikola reported revenues of solely $24 million on the supply of 63 BEV Tres. The corporate produced 75 vehicles within the quarter and solely mentioned the 100-truck buy order from Zeem Options.

The monetary image stays very murky with working losses and EBITDA widening as the corporate ramps up manufacturing. Nikola misplaced $230 million in Q3’22 and the EITDA loss was $106 million with capex spending of $51 million.

Supply: Nikola Q3’22 presentation

The big distinction between the losses was $103 million in stock-based compensation. Because of the SBC and ATM, Nikola has seen the share rely boosted to 438 million shares in Q3 with the diluted share rely far increased at over 490 million shares at yr finish.

Nikola wants much more orders and plans to provide past 3 BEV Tres over one every day shift with the capability for five vehicles per shift. The corporate expects to finish Part 2 development quickly pushing capability to twenty,000 items per yr, however Nikola is just producing what quantities to ~750 items a yr.

Traders ought to’ve observed how the earnings launch shortly shifted to discussing the vitality enterprise with solely a minor replace on the Tre BEV automobile in precise manufacturing. On the Q3’22 earnings name, the brand new CEO mentioned a number of the points with the truck market resulting in the deferring of the Part 3 growth till at the very least 2024:

The place we are able to enhance is on the business aspect of the enterprise. It is clear that there are macro headwinds proper now that in some unspecified time in the future will flip into macro tailwinds. We should take proactive steps to guarantee that now we have a business program in place that can enable us to completely profit when the market dynamics turn out to be extra favorable. I consider we are able to obtain this by growing our devoted gross sales efforts to raised perceive our clients and their wants. We have to turn out to be much less depending on sellers and as a substitute lead them in our business administration.

Our prior analysis had highlighted this danger as a first-rate purpose to stay on the sidelines. Nikola made spectacular progress getting the truck produced, however promoting vehicles for a revenue is an entire totally different story and the corporate had did not announce any significant orders.

The CFO did not even information to Tre BEV deliveries in This fall regardless of expectations for manufacturing of anyplace from 120 to 170 items. On the time, Nikola needs to be ramping up gross sales expectations and full velocity forward on promoting BEVs, however the firm is already headed to the following large alternative because of charging infrastructure points limiting orders and excessive prices limiting the interior want to promote extra vehicles.

Hydrogen Promise Is not Sufficient

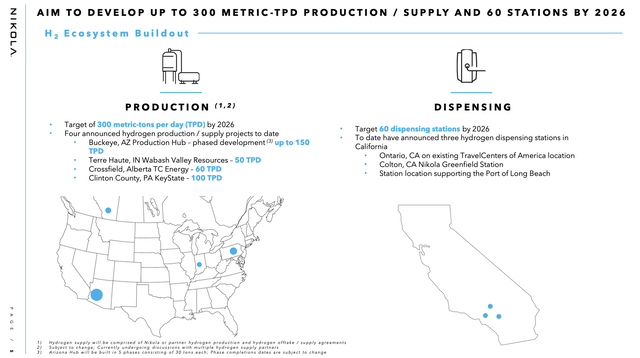

The odd a part of the Q3’22 earnings presentation and quite a lot of the information gadgets just lately is that Nikola seems to have shifted to an vitality firm from one targeted on producing heavy-duty vehicles and needing vitality provides for purchasers to gasoline the vehicles. Nikola now goals to develop a big community of hydrogen allotting stations with as much as 300 metric-bpd of manufacturing through 4 services round North America.

Supply: Nikola Q3’22 presentation

The corporate is engaged on a mortgage kind the federal government for the Phoenix Hydrogen Hub challenge offering the capital to completely develop the 150 metric-tpd manufacturing facility. As soon as ultimate funding selections and customary regulatory approvals are finalized, development of the primary section is anticipated to be accomplished in 2024.

Nikola even introduced a cope with Plug Energy (PLUG) for a 30-tpd liquefaction system on the Arizona hub and as much as 125-tpd of hydrogen by 2026, with 80% underneath a take-or-pay contract. The one fascinating facet of the deal is the acquisition by Plug of 75 Nikola Tre gasoline cell electrical automobiles to deliver inexperienced hydrogen to Plug clients with the primary supply in 2023.

Even with the joy round utilizing hydrogen as a gasoline supply and the supposed demand across the Tre FCEVs is that Nikola stays on the bleeding edge. The corporate burned ~$180 million in money throughout Q3 and the corporate has one other yr earlier than the brand new vehicles are even launched underneath the very best situation. As well as, our analysis has already recognized Plug Energy as an organization large on making bulletins and low on delivering outcomes.

Nikola ended the final quarter with a money steadiness of solely $404 million with the opposite sources for liquidity inflicting large dilution with the inventory all the way down to solely $2. A big authorities mortgage would possibly present a stable supply of liquidity for the hydrogen ecosystem, however the firm has to indicate how the enterprise transitions from the bleeding edge and ever makes a revenue after the BEV failure.

Takeaway

The important thing investor takeaway is that traders ought to proceed watching Nikola from the sidelines. The corporate has transitioned to with the ability to construct vehicles, however the government workforce hasn’t proven any capacity to transition to promoting vehicles and working a rising firm. The most important concern now’s the shortage of proprietary expertise in an more and more crowded house.

{kind=link}