Marcio Silva/iStock through Getty Pictures

It’s been a tricky 12 months for the semiconductor area, to say the least. We’ve expanded our protection this quarter, publishing a number of instances on 23 of the world’s most vital semiconductors. We finish each quarter reviewing our rankings and finding out how our predictions have panned out over the previous couple of months. We work in a forward-looking market, however consider reviewing our funding theses is important to do what we do and do it effectively.

Our high-risk, high-reward shares:

Whereas we acquired quite a lot of backlash for non-consensus rankings on Nvidia (NVDA), Superior Micro Units (AMD), and reminiscence large Micron (MU), we’ve seen our predictions for the three pan out this quarter. We’ve upgraded NVDA, AMD, and MU since, though the inventory costs for all stay risky within the close to time period. We’ve additionally upgraded Intel (INTC) after the final quarterly report.

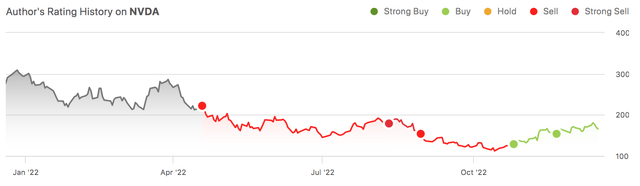

1. NVDA

NVDA’s been certainly one of our biggest calls this 12 months. We acquired quite a lot of backlash for our promote score for NVDA, however we consider our thesis relating to NVDA’s publicity to crypto-mining-related GPU gross sales has panned out and been adopted by a pointy correction in 2H22. We upgraded NVDA on the finish of October as we consider the gaming weak spot has been priced into the inventory.

We had been a bit involved in regards to the influence of U.S. DoC export restrictions on Chinese language clients. Nonetheless, we anticipated new product cycles and stock hoarding by Chinese language clients to offset the U.S. laws. We noticed NVDA carry out constantly with our predictions when the corporate shocked everybody with the brand new A800 that substituted the A100 getting round U.S. laws. We consider the worst is behind for NVDA and keep our purchase score. The inventory’s been creeping again up since our improve, and we anticipate the inventory to rally in 2023.

The next graph outlines NVDA’s inventory efficiency and our rankings.

SeekingAlpha

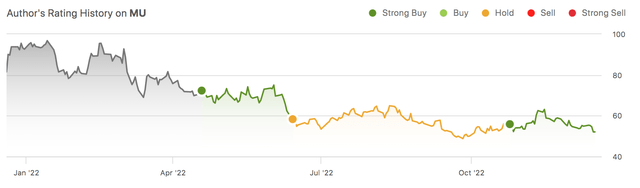

2. MU

2022 was particularly tough for the reminiscence business; we consider weakening client spending took a slice of MU’s income streams earlier this 12 months. Whereas we’ve been bearish on MU for a lot of the 12 months, we upgraded the inventory in late October based mostly on our perception that the worst of reminiscence weak spot has been priced in.

The inventory rallied for a bit after our improve, adopted by a sell-off. The inventory worth is risky, however we keep our bullish sentiment as we consider MU has de-risked its steerage, pricing within the macroeconomic weak spot.

The next graph outlines MU’s inventory efficiency and our rankings this 12 months.

SeekingAlpha

3. INTC

INTC was one other attention-grabbing inventory this year- we upgraded INTC this quarter as we consider the corporate’s monetary efficiency will enhance in 2023. We consider the corporate’s plans to turn into a U.S.-based fab will take capital and time. We don’t see INTC turning into a significant fab participant earlier than 2024. INTC’s inventory efficiency isn’t the prettiest, however we anticipate the corporate will slowly recuperate towards 2H23.

The next graph outlines our rankings on INTC YTD.

SeekingAlpha

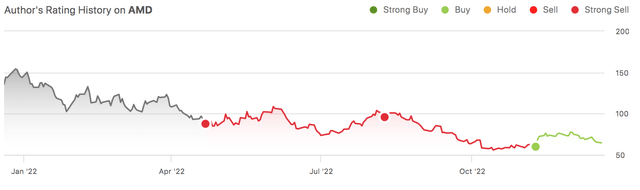

4. AMD

We upgraded AMD in mid-November and have seen the inventory slowly decide again up. We consider most, if not all, the draw back from weaker PC and gaming GPU demand have been priced into the corporate’s outlook. We anticipate AMD to outperform in 2023 and suggest shopping for the inventory whereas it’s close to the underside.

The next graph outlines our score historical past on AMD.

SeekingAlpha

Our still-bearish picks:

Whereas we’re extra optimistic in regards to the semi area than we had been 1 / 4 in the past, we stay bearish on particular shares. Our greatest issues this quarter have been within the space for storing, particularly Western Digital (WDC) and Seagate (STX).

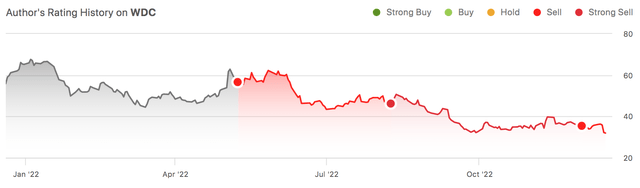

1. WDC

WDC has dropped almost 44% since we first revealed our promote score on the inventory. We anticipate WDC to proceed to underperform based mostly on our perception that client weak spot is spreading into business markets. We consider the corporate will face demand headwinds in its flash and Exhausting Disk Drives (HDDs).

The next graph outlines our score historical past on WDC.

SeekingAlpha

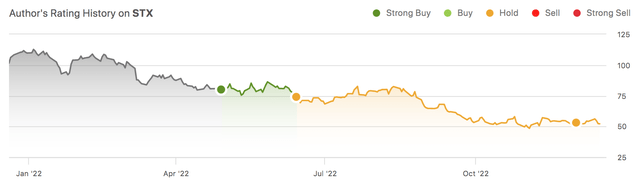

2. STX

STX can also be on our listing of bearish shares this quarter. We’ve been hold-rated on the inventory since July. In line with our beliefs, STX reported a 26% sequential decline and a 38% Y/Y drop in gross sales in 1Q23. We consider client weak spot has slipped into storage demand and suggest buyers wait on the sidelines for a greater entry level on the inventory.

The next graph outlines our score historical past for STX.

SeekingAlpha

3. International Foundries (GFS)

GFS has been a brand new addition to our protection. We’re sell-rated on GFS regardless of the chip-maker reporting an impressive 3Q22. We consider ASP will increase drove income progress prior to now 12 months. In 2Q22, GFS reported a 16% enhance in ASP per wafer whereas solely reporting a 6% enhance in unit shipments. Unit cargo remained low in 3Q22, rising solely 5% Y/Y. We consider the corporate gained’t be capable of keep income progress by way of elevated ASP and therefore suggest buyers exit the inventory at present ranges.

We consider the corporate had room to extend ASP this 12 months because of the inflationary atmosphere and provide shortages. We don’t consider they’ll have the identical alternative once more with unit shipments normalizing because of the macroeconomic atmosphere. We don’t see GFS rising meaningfully towards 1H23.

Timing is every part; the place we might’ve gone higher:

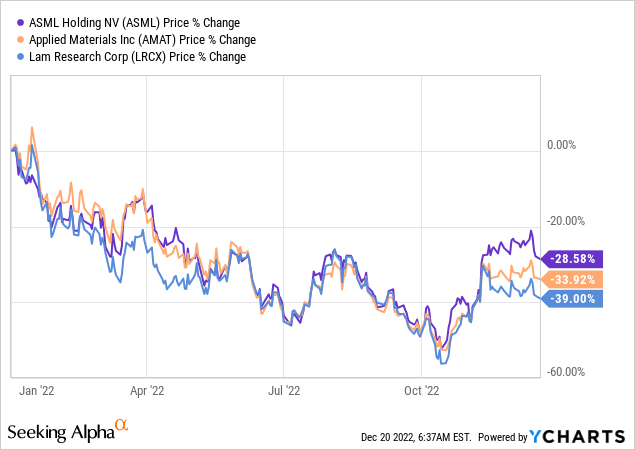

We wish to look again on the quarter and see what calls might have gone higher. AMAT and LRCX had a bumpy 12 months. Whereas we’re bullish on each shares now, we should always have downgraded them to a promote earlier than the dip in October. The semiconductor business is cyclical and reacts to the market. In flip, we anticipate to see the semi area start to recuperate, headed by the semi cap shares ASML, Utilized Supplies (AMAT), and Lam Analysis (LRCX). Whereas we consider our expectations will pan out in the direction of 2023, we should always have downgraded earlier than the dip after which upgraded once more close to the underside to keep up our slogan of purchase low, promote excessive.

We’re constructive on the semi-cap, as we anticipate the semiconductor enlargement into U.S.-based fabs will enhance demand for semi manufacturing tools. We’re seeing the semi-cap slowly decide up after a deep dip in October.

The next graph outlines our high picks within the semi-cap area over YTD.

TechStockPros

What we suggest you do with the shares:

All through our protection of the semiconductor area, we’ve maintained a non-consensus outlook of the business. We’ve been extra bullish this quarter, as we consider the semi area offers favorable entry factors that we haven’t seen because the market dip at first of the pandemic. This quarter’s greatest takeaway from the semiconductor business has been: to purchase into the world’s most vital semis as soon as the weak spot has been priced in. As provide improves and stock corrections are underway, we anticipate the semi area to slowly however certainly recuperate. We’ll proceed to be forward-looking and monitor how our rankings materialize or fail to. The semi area ought to stay risky over the approaching quarters, however we consider we’re using the upward pattern greater in 2023.

{kind=link}