Neustockimages/E+ through Getty Photos

“If Santa Claus ought to fail to name, bears might come to Broad and Wall.”

I’ve been getting requests for my predictions for 2023. Earlier than I’m going into that train, I’ve to deal with the truth that I used to be calling for a year-end rally these final two months. Let’s go away apart the militant Powell, who had a really huge hand in repressing the bull this 12 months. We additionally had large tax loss promoting, a rebalancing for pension and sovereign funds transferring funds from equities to bonds. You is perhaps shocked to be taught that this quarter shares did higher than bonds. So these establishments nonetheless adhere to 60/40 equities to bonds. Lastly, there was large “window dressing”, fund managers needed to reduce holding the “losers” of their portfolios, in order that they dumped the big-cap tech names. Sure, the inventory market can rally with out the large caps, it simply isn’t as simple to do with out them.

So the place will shares be in ‘23?

Let me begin off by saying it’s the top of folly to truly make a projection going out for 12 months. There are such a lot of elements to weigh, they usually don’t line up neatly. Is inflation falling, sure it actually is.

This previous Friday’s core PCE ex-food and vitality fell to 4.7%, which is similar stage we have been at approach again in July. The height was again in September at 5.2%, there isn’t a one saying that inflation isn’t falling. The complaints are that it isn’t quick sufficient or that it’s “sticky” and that’s as a result of unemployment is so low. Not solely that however there are too many open jobs per out there employee. All that is well-known, but practically day-after-day we’re listening to about large layoffs that aren’t having the specified impact. The final weekly unemployment quantity was simply 216K, which isn’t a recession-level quantity. To me, because of this these skilled employees are being eagerly snapped up by smaller firms that desperately want their expertise. I’ve largely repeated comparable statistics for months now and doubtless seems like a damaged report. These stats can’t be misplaced on Powell’s Fed, so the query should be why is Powell so militant? At the same time as he’s beginning to ease (going from .75% to .50%), he must preserve strain on the cash provide. We’ve to acknowledge the inconvenient fact, that the inventory market can gush cash. Powell feels that rising wealth will add extra strain on demand which in return pushes up wages (after which inflation). So the Fed plans to go to a traditional fee regime of .25% from .50%, and arrive at +5% as a terminal fee. If the speed rises to the purpose of throwing the US right into a recession, so be it; some suppose Powell WANTS a recession. So the hazard of the inventory market stays in a bear marketplace for a number of months and even the whole 2023 the Fed may care much less. As a result of the Terminal Fed Funds Charge is predicted to be +5%, various commentators at the moment are speaking in regards to the S&P 500 dropping to pre-pandemic ranges. With a fee this excessive and a looming recession, the S&P earnings expectations are simply too excessive. The basic analysts count on 2023 earnings to generate solely $200, and at 15 instances that offers us 3,000, the technicians aren’t rather more beneficiant as they’re at 3200 for the S&P. So the conclusion is, 2023 might be one other horrible 12 months.

Not so quick

Final week we have been handled to the information that the ultimate revision of Q3 GDP was 3.2%. So at the same time as Milton Friedman says “fiscal coverage works with lengthy and variable lags’ ‘, that signifies that the final a number of fee raises might not have had their full impact. But, the sentence “variable lags” may imply that many of the fee raises have already made their mark. But, right here we’ve got a GDP of OVER 3%. What if we not solely have a rising GDP, however earnings stand as much as the onslaught or greater charges? My conjecture is, earnings for This autumn will stay secure and the earnings for 2023 might be extra like $230 than $200, it’ll get us near the present stage of the S&P 500. The greenback is falling so all of the big-cap tech will be capable to report extra favorable worldwide earnings with the weaker greenback. My conjecture is that now that the speed rises are coming to the tip, an earnings recession will take over and slam the indexes down from 3000 to 3200. The subsequent piece is that as inflation strikes again into the background, PE ratios will re-expand, getting us into the low-4000s. I additionally strongly imagine that the treasuries are telling us that the precise terminal FFR might be near 4.1% to 4.49%. The financial system has been working at these elevated charges for months now. Additionally, the infrastructure invoice ought to be kicking on this 12 months, so regardless of the lengthy and variable lags of the speed rises, the financial system can’t solely develop, however shares can no less than preserve the present vary from 3800 to 4200. Add to that, the rarity of two years in a row of a bear market is exceedingly excessive, so the possibilities of 2023 leading to losses for shares are low.

So the place do I stand?

I hate to depart you hanging, however I actually don’t know what’s going to occur. It actually all comes right down to the psyche of 1 man. Will Jay Powell be glad by the gradual retreat of inflation? Or will he proceed with successive fee raises, albeit in smaller increments? In some unspecified time in the future, the financial system will lastly get the proverbial “straw that breaks the camel’s again”, after which the Fed must furiously back-pedal. Subsequently I would not be terribly stunned to see yet one more fee rise, earlier than the Fed halts. I see Q1 for inventory as a continuation of This autumn buying and selling. If earnings do comparatively effectively, shares will deal with us higher than anticipated. So I conclude with a tepid reply, Regular as she goes. Although with one caveat, let’s watch the earnings pre-announcements. If we don’t hear of any reducing of expectations from the likes of Microsoft (MSFT) due to overseas alternate, or from Adobe (ADBE) from longer contract cycles, then the notion of a pointy sell-off due to an “Earnings Recession” simply is not going to be there. If we’ve got a string of warnings, and any trace of the inflation dragon rearing up then 3200 right here we come.

What to do

The primary rule of the Money Administration Self-discipline is to begin trimming positions as quickly as we see a recognized danger. Earnings season is all the time fraught however this This autumn has lots using on it. Moreover, we have to take note of reducing earnings expectations bulletins. Are they extra in quantity than typical? Are the revisions deeper than typical? I’ve been asking the Twin Thoughts Neighborhood members to start trimming 1% to three% of previous positions every day into the primary week of January. Our purpose might be 20% to 30% money. I additionally advocate hedging; it has by no means been really easy to hedge as it’s now. There are various inverse ETF primarily based on the most important indexes. I’d wait till earnings really start earlier than I’d construct an considerable quantity of such equities. Please research the 3X inverse ETFs. The tremendous print urges you to solely maintain them for twenty-four hours, so I’d decrease the size of time in them for as quick a time as potential. If the market sells off onerous, they’ll carry out their protecting mission. Nonetheless, like all highly effective device, it could actually work in opposition to you if the market soars. Proper now it is a extremely unlikely state of affairs however not inconceivable. I cannot provide the symbols, please do your homework and perceive what it’s you might be placing your {dollars} into.

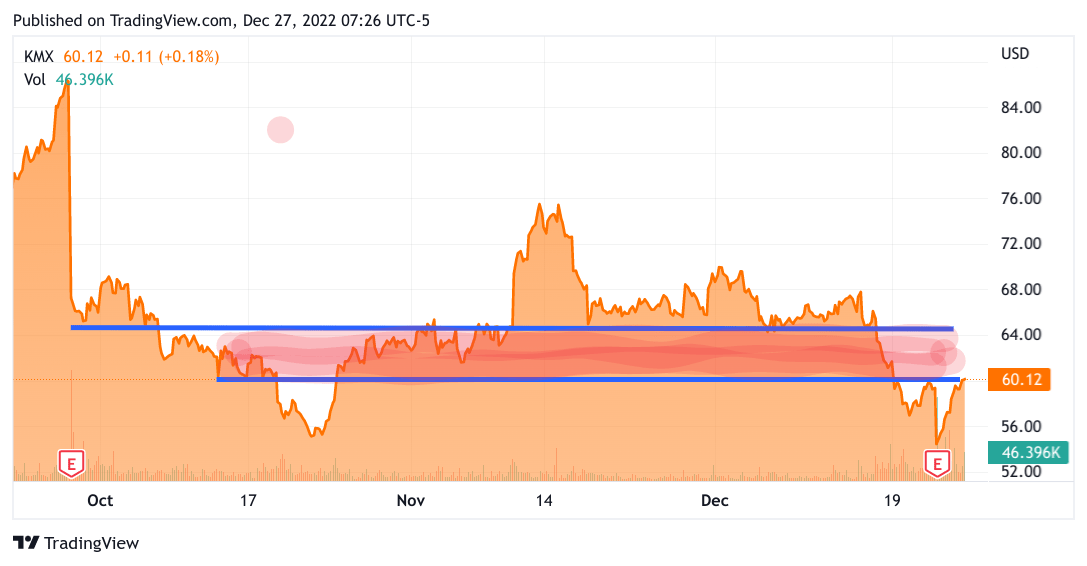

The subsequent stage is to hunt out susceptible shares which can be more likely to go down anyway. It takes some getting used to however if you’re comfy with inventory selecting you simply have to coach your thoughts to search for the alternative of what you’d usually put money into. Will the concern of recession come to actuality? Onerous to know, however there is perhaps shares that might be susceptible to greater prices, or sharper competitors, or waning client curiosity. Right here’s an instance, used automobiles. Not too way back some latest mannequin used automobiles have been promoting at costs greater than once they have been model new! Not, used automotive costs have cratered. So should you promote used automobiles, you’ve already taken successful on the costly automobiles to procure simply this previous Fall. Furthermore, new automobiles are lastly changing into plentiful, and being supplied for 1.9% financing. Think about competing with new automobiles for reasonable financing. It’s not simply automobiles, after all, it’s simply the perfect one I can consider. Perhaps going after a Nordstrom (JWN) might be a greater draw back play. That simply flew into my head however it really seems like a good suggestion, I’m going to look into the “aspirational” retailers as one thing to go on the quick facet. I exploit Put choices to generate alpha on shares that I believe are susceptible proper now. Perhaps there may be extra of a draw back to the FANG names, I’ll search for a option to categorical that with Places. Why? This can be a type of hedging as effectively. If I’m appropriate and the market trades sideways and even down, the strain on shares that I imagine are susceptible will hopefully greater than make up for the shares I’m lengthy in. Why not simply hedge on the indexes? I do each. I do each as a result of I are inclined to hate being a bear. So I have a tendency to shut out my hedges on the indexes too shortly. So by searching for susceptible sectors and shares in these sectors, I can maintain on utilizing my conviction on a specific identify. So the used Automotive firm I discussed is CarMax (KMX). They’d a horrible ER. Unusually the inventory rose after the dismal earnings report. I imagine it was quick masking. So as we speak I executed some Places on that identify with a February expiration and a $60 Strike. There is no such thing as a scarcity of candidates to go after, sadly.

Under is a chart of KMX. This can be a 3-Month chart and as you may see there are two parallel traces over that 60 stage. That is what we name “congestion”. It’s exhibiting there’s a large provide of stranded patrons on this identify anxious to be made complete. The second the inventory will get into that space there might be a deluge of prepared sellers. However, there are patrons that bought into KMX at beneath 56 just some days in the past which may wish to get out whereas they’ll. All this factors to promoting strain, and that’s the reason I’ve Places on it. I’ve no in poor health will to the administration, nor to used automotive salesmen, or the used automotive business. I’m simply making an attempt to create some steadiness in my portfolio to cope with the bearish potentialities. The wonderful thing about searching for susceptible firms is that if the market turns towards the bulls, you should still earn a living on bearish bets.

TradingView

These are powerful instances. You’ll be able to select to shut your portfolio and never take a look at your shares or you may take an lively hand and navigate to calmer waters. I solely commerce with a small portion of my portfolio. I’ve a long-term account that I’ve a very totally different method with, There I search for good dividend-paying shares and ETFs. There are a smaller variety of long-term bets that I’m prepared to carry and see what occurs. I favor earnings era most of all. Research have proven that in instances of slower financial progress, shares with dividends generate most of their positive aspects by means of earnings. So if my suggestion of taking an lively function is just not your cup of tea, there’s a nice alternative in holding shares for the long run as effectively.

{kind=link}