gremlin/E+ by way of Getty Photos

To carry, or to not maintain, that’s the query. This mockery of Shakespeare’s well-known epigram fits my current rumination whether or not to keep up a place in Abroad Shipholding Group, Inc. (NYSE:OSG). The inventory has carried out handsomely this 12 months, up ~51% YTD, however its ascension could have run its course. After a gradual climb beginning in July, OSG sputtered in late September on information of insider promoting. Curiosity has remained tepid ever since.

With that mentioned, future steering suggests the inventory may transfer larger over the approaching quarters. Administration foresees a promising ’23 pushed by ample free money technology and alternatives to broaden into new markets. This forecast is bolstered by daring insider shopping for from the corporate’s CEO. There was, nonetheless, an equal quantity of institutional promoting, which suggests administration’s outlook could be overly optimistic.

General, OSG’s fundamentals stay stable, with an distinctive managerial outlook, and the corporate seems undervalued relative to friends. However, this 12 months’s worth appreciation means that at the least among the outlook is already baked in. Due to this fact, OSG is advisable as a Purchase and the earlier worth goal of $3.10/sh stays intact

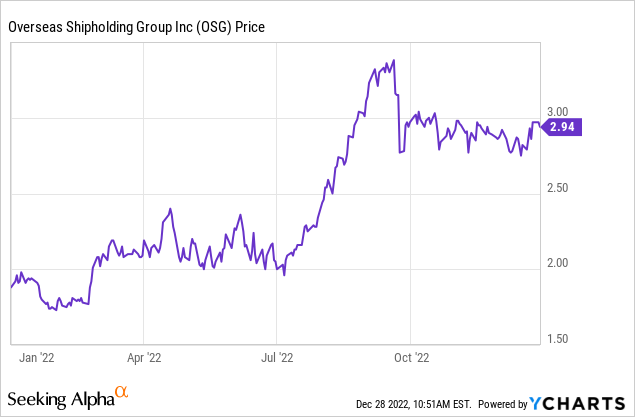

Inventory Appreciation

OSG skilled robust worth appreciation earlier this 12 months, with the top off 50%-plus year-to-date. It hit a multi-year intraday excessive of $3.39/sh in September:

The inventory’s run was poised to proceed till it was interrupted by the information that Anja Manuel, an OSG unbiased director, offered 54% of her place at $3.17/sh. The inventory offered off subsequently and has traded narrowly since.

Steering

Ahead steering contravenes latest worth motion. Within the Q3’22 convention name, administration guided for FY’22 TCE revenues “at about $420 million and adjusted EBITDA ought to exceed $133 million.” Moreover, OSG anticipates, after share repurchases, year-end money balances between $90 million and $100 million. The money steadiness places OSG in a wonderful place to return capital to shareholders within the near-term.

Moreover, OSG is anticipating FY’23 to be nearly as good, if not higher, as FY’22 regardless of returning three vessels to American Transport Firm (OTCQX:ASCJF) earlier this month. Redelivery of the ASC vessels will scale back annual mounted fee obligations by ~$27m/12 months but the corporate expects to keep up comparable operational efficiency as FY’22. FY’23 TCE revenues for 2023 are anticipated to be ~$400m with adj. EBITDA between $100m and $135m.

To this finish, administration acknowledged “OSG vessels are basically absolutely dedicated properly into the center of subsequent 12 months” with “92% of obtainable (Jones Act) vessel working days [] coated for all of 2023.” The corporate is also making inroads into the renewable diesel commerce. On the decision, administration famous OSG has:

… negotiated time charters with 4 completely different charters engaged in renewable diesel commerce with the outcome that by the center of subsequent 12 months, 50% of (the corporate’s) typical tanker fleet will probably be employed in trades associated to renewable diesel, with a number of of those contracts extending past the tip of 2023.

As for ’23 money circulation, OSG anticipates FY’23 FCF, after debt service and capex, between $50m and $55m. Including that to ’22 year-end steadiness, OSG is heading in the right direction to have ~$140m-$155m in money on the shut of ’23. With that quantity, the corporate may simply retire a considerable chunk of debt, purchase a brand new vessels, or probably return a portion to shareholders.

Share Possession

OSG’s rosy outlook has made its CEO, Samuel Norton, bullish on the corporate’s inventory. Earlier this month, he introduced buying 350k @$2.92/sh from Cyrus Capital Companions – OSG’s second largest exterior shareholder. The acquisition put Mr. Norton’s whole place in OSG at 2.45m shares (~3.1% of OSG). Cyrus’ divestiture is the second sale the agency has fabricated from OSG’s shares within the final two months. In November, Cyrus offered 5m @$2.86/share to OSG in a non-public transaction. Whereas there are a number of the reason why one sells, there’s just one motive for getting. Mr. Norton’s buy evokes confidence that OSG will proceed to create shareholder worth regardless of this 12 months’s capital appreciation.

Valuation

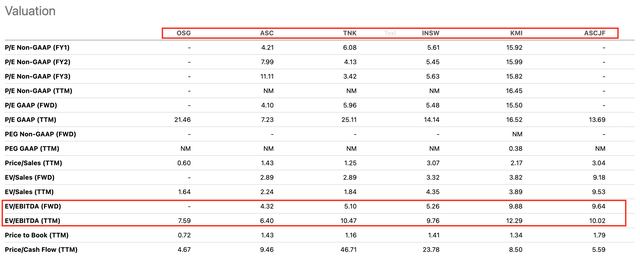

OSG at the moment has an enterprise worth of ~$685m (inclusive of its marketable securities and working and monetary leases, at honest market). OSG’s FY’23 Adj. EBITDA between $100 – $135m implies the corporate trades 5.1x – 6.8x FWD EBITDA, with a midpoint of 6.0x. This compares to a mean 6.8x for OSG’s friends:

Looking for Alpha – OSG Friends, Personalized

Nonetheless, Kinder Morgan (KMI) and American Transport Firm – OSG’s Jones Act rivals – commerce at ~9.8x FWD EBITDA. Whether or not or not OSG may fetch the same a number of as its Jones Act friends is speculative, though not unrealistic. However even when it had been to commerce at 7x FWD EBITDA, nonetheless a considerable low cost to Jones Act friends, the inventory may commerce north of $4/sh.

All issues thought of, OSG stays a Purchase and is one to observe over the approaching quarters.

{kind=link}