Dilok Klaisataporn

The Simplify Curiosity Charge Hedge ETF (NYSEARCA:PFIX) offers a hedge to buyers apprehensive about rising rates of interest by means of a portfolio of OTC swaptions. Lengthy-term rates of interest are reaccelerating increased because the BOJ’s shock transfer to extend the 10Yr JGB rate of interest cap is inflicting billions in carry trades to be unwound. I’m a purchaser of PFIX as a hedge.

Fund Overview

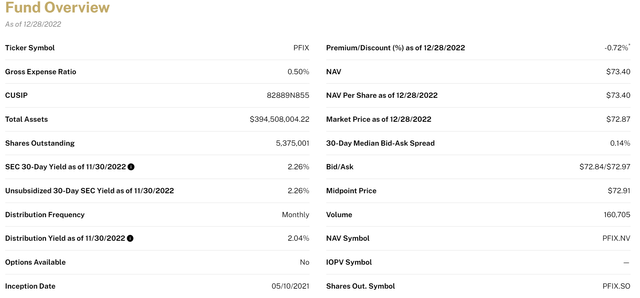

The Simplify Curiosity Charge Hedge ETF offers buyers with a hedge in opposition to rising long-term rates of interest. It additionally advantages when fastened earnings volatility will increase. The fund has virtually $400 million in belongings as of December 28, 2022 and prices a 0.50% gross expense ratio (Determine 1).

Determine 1 – PFIX fund overview (simplify.us)

Technique

The PFIX ETF seeks to realize its funding goal by primarily investing in over-the-counter (“OTC”) rate of interest derivatives that present convex publicity to giant upward strikes in rates of interest and rate of interest volatility.

Traditionally, OTC derivatives are solely accessible to institutional buyers (suppose ISDA settlement the film “The Massive Brief”). PFIX bridges the hole between retail buyers and instruments that institutional buyers use to hedge / speculate on the trail of rates of interest.

In line with the fund’s advertising and marketing literature, the PFIX ETF is “functionally much like proudly owning a place in long-dated put choices on 20-year US Treasury bonds”. For buyers within the PFIX ETF, this offers a easy and clear rate of interest hedge.

Wanting on the fund’s technique intimately, the PFIX ETF will initially make investments 50% of its NAV in 7-year OTC payer swaptions (pay fastened, obtain floating) on the 20-year treasury fee struck at 4.25%. The swaption advantages as rate of interest rises. The choice is reviewed and reset periodically or after excessive rate of interest strikes. PFIX chooses an prolonged time period and strike to reduce the price of possession (much less rebalancing) and maximize convexity.

Portfolio Holdings

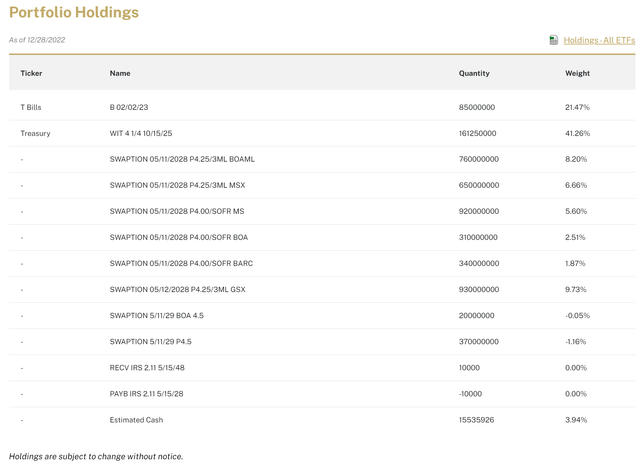

Determine 2 reveals the PFIX ETF’s holdings as of December 28, 2022. The ETF at present holds 33.4% internet belongings in swaptions paying between 4 and 4.25% in opposition to main funding banks similar to Goldman Sachs, Financial institution of America, and Morgan Stanley.

Determine 2 – PFIX holdings (simplify.us)

Returns

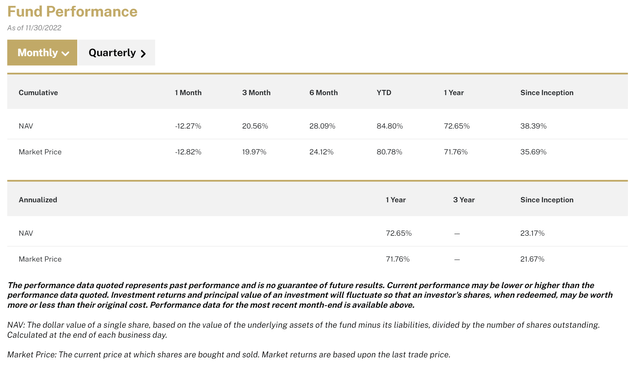

As 2022 has been characterised by world central banks elevating rates of interest on the quickest tempo in hisotry to fight inflation, PFIX has been a main beneficiary. YTD to November 30, 2022, the PFIX ETF has delivered 84.8% returns in its NAV. Since its inception on Might 10, 2021, the fund has returned 38.4% annualized (Determine 3).

Determine 3 – PFIX returns (simplify.us)

Distribution & Yield

The PFIX ETF pays a nominal trailing 12 month distribution of $0.45 /share or 0.6%.

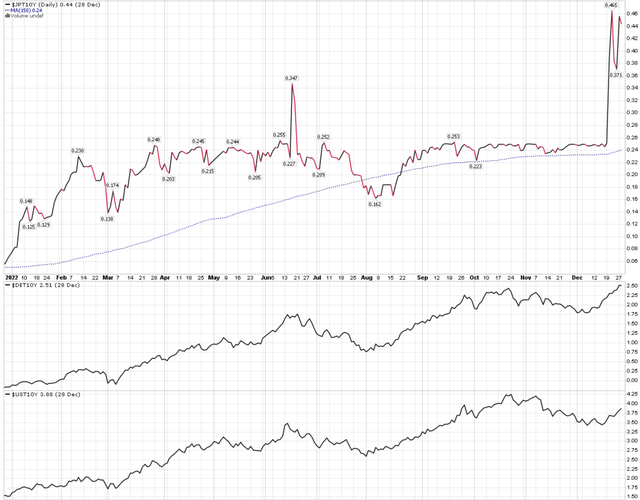

BOJ Triggering Subsequent Part Of Bond Volatility?

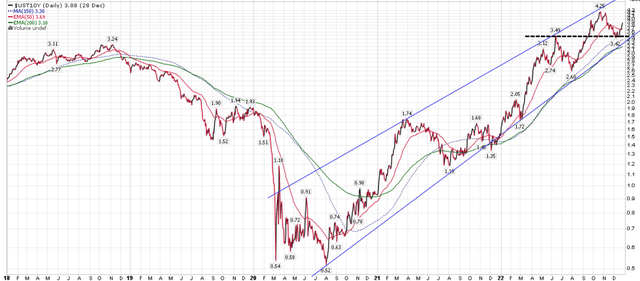

A number of weeks in the past, I wrote in an article on the ProShares UltraPro Brief 20+ 12 months Treasury ETF (TTT), suggesting the interval of rate of interest will increase was coming to an finish, as buyers begin to worth in a recession in 2023 and the Federal Reserve pivot to reducing rates of interest.

Nevertheless, in hindsight, my name might have been untimely, because the U.S. 10-year treasury yield started heading increased in current weeks, reversing close to the necessary help stage round 3.50% (Determine 4).

Determine 4 – 10 Yr treasury yield reaccelerating (Creator created with worth chart from stockcharts.com)

A lot of causes look like driving this reacceleration in rates of interest. First, the Federal Reserve reiterated its hawkish ‘increased for longer’ stance at its most up-to-date FOMC assembly on December 13-14. This message is in stark distinction to buyers’ expectations for the Fed to start out reducing rates of interest in H2/2023.

Second, financial information launched previously few weeks had been truly stronger than anticipated, with U.S. GDP rising at an annualized 3.2% in Q3/2022. Mockingly, good information is now thought of dangerous, because it provides the Federal Reserve cowl to stay to its ‘increased for longer’ coverage.

Lastly, maybe essentially the most impactful short-term motive for the rise in rates of interest was the shock transfer on by the BOJ to boost the yield restrict for 10Yr JGBs to 0.50%, from a earlier restrict of 0.25%. The ‘BOJ Christmas Shock’ caught many buyers off-guard, as most had been anticipating modifications to BOJ coverage solely after Governor Kuroda’s time period ends in April 2023.

10Yr JGB yields jumped virtually instantaneously to the 0.50% goal, even because the BOJ stepped in with limitless bond purchases. This BOJ transfer seems to have sparked a reacceleration of worldwide bond yields, with German 10Yr yields now above their October highs at 2.50% and U.S. 10Yr yields quickly rising as effectively (Determine 5).

Determine 5 – JGBs main world yields increased (Creator created with worth charts from stockcharts.com)

BOJ Might Have Blown Up The Yen Carry Commerce

Recall, the Japanese Yen is the funding forex behind tens, if not lots of of billions, in ‘carry trades’ – a macro commerce the place buyers borrow at extremely low Japanese rates of interest and make investments the proceeds in increased yielding belongings. The ‘BOJ Christmas Shock’ brought about the Yen to leap essentially the most in 24 years and certain blew up many carry commerce buyers, as leverage is often used to amplify the carry commerce returns. As carry trades are unwound, overseas belongings like U.S. treasuries are bought off, resulting in rising rates of interest.

Moreover, with increased rates of interest being supplied domestically, Japanese buyers have much less incentive to put money into overseas belongings like U.S. treasuries.

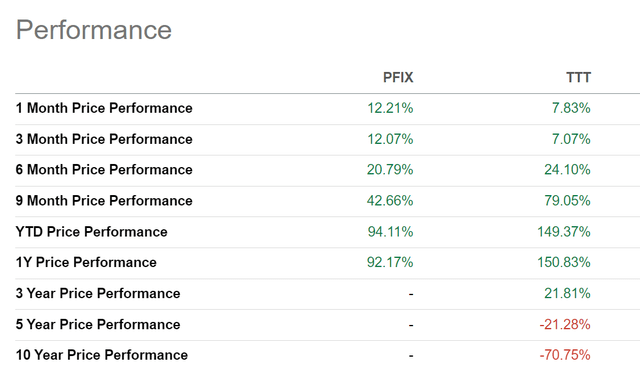

PFIX vs. Inverse ETFs

For buyers trying to hedge rate of interest publicity, I imagine the PFIX ETF could also be a superior car in comparison with inverse levered ETFs just like the TTT. That is due to the construction of their funding portfolios.

Whereas each the PFIX and TTT provides convex returns in opposition to rising rates of interest, if the ‘path’ of rate of interest enhance is unstable, the PFIX ETF ought to outperform, because it doesn’t undergo from volatility decay resulting from every day rebalancings (please discuss with my prior articles on levered ETFs for a extra detailed clarification of this time period). As a substitute, the PFIX may have a every day theta decay cost that needs to be small compared because of the portfolio’s long-dated nature.

For instance, the PFIX has outperformed the TTT on a 1 and three month timeframe (Determine 6) because the previous few months have been characterised by elevated volatility.

Determine 6 – PFIX vs. TTT returns (In search of Alpha)

In actual fact, as 10Yr rate of interest rises to the strike worth of PFIX’s swaptions (4% to 4.25%), we must always count on the worth of its portfolio to extend in a convex method.

Conclusion

The PFIX ETF offers a hedge to buyers apprehensive about rising rates of interest by means of a portfolio of OTC swaptions. Lengthy-term rates of interest are reaccelerating increased because the Fed is sticking to its ‘increased for longer’ coverage and the financial system seems extra resilient than anticipated. Most significantly, the BOJ’s shock transfer to extend the 10Yr JGB rate of interest cap is sparking a brand new wave of rate of interest volatility, as billions in carry trades are unwound. I’m a purchaser of PFIX as a hedge.

{kind=link}