We’re but to search out out what lies in retailer for the inventory market in 2023. Nevertheless, we do know that the earlier 12 months was one of many worst ever, with the S&P 500 placing in its seventh most abject annual efficiency since 1929.

Whichever approach you have a look at it, then, most traders didn’t benefit from the previous 12 months’ market motion. One optimistic takeaway, nonetheless, is that the general bearish development has pushed share costs down throughout the board and that has left some shares at ranges that at the moment are simply too low cost to disregard.

That’s definitely the view of the analysts at JPMorgan. The banking titan’s analysts have pinpointed a chance in two names whose valuations have contracted considerably in latest instances – undeservedly so, they consider. Does the remainder of the Avenue agree they’re going for reasonable? Let’s take a better look.

Palomar Holdings (PLMR)

We’ll begin with Palomar Holdings, an insurance coverage firm with a distinction. As a substitute of specializing in conventional insurance coverage protection, Palomar targets what it phrases ‘underserved’ markets, comparable to earthquake, flood and hurricane insurance coverage. The corporate provides its shoppers a variety of versatile merchandise and tailor-made pricing plans utilizing its knowledge analytics and cutting-edge expertise platform.

2022 was panning out slightly nicely for the specialty insurance coverage firm’s inventory, however then Palomar launched its Q3 earnings report, and it was not what traders needed to see.

Whereas income climbed 17.2% year-over-year to of $79.3 million, that determine missed the consensus estimate by a big $14.18 million. Likewise, on the bottom-line, the analysts had been anticipating adj. EPS of $0.52, however that determine got here in at $0.23. The consequence of those delicate metrics was a downward spiral for the shares; the inventory is now down by 47% from final 12 months’s October highs.

Whereas cognizant of the delicate quarterly efficiency and aware of the “headwinds that may probably strain PLMR’s outcomes by 2023,” JPM’s Jimmy Bhullar thinks the inventory’s sell-off “appears too steep.”

Story continues

“We expect that the present inventory value ignores near-term enhancements in enterprise tendencies which might be already materializing (PLMR has signaled a restoration in premium development in binary strains after a softer 3Q22) and the varied steps PLMR is taking to offset the impression of upper reinsurance pricing (albeit with a delayed impression),” the analyst went on to say. “Moreover, we consider that the above-average development profile of PLMR stays intact given alternatives in its core earthquake market and in new strains. At its present inventory value, PLMR is buying and selling in keeping with giant industrial friends on 2024 earnings already decreased for the above elements with out receiving any valuation profit for its superior margin or development profile in subsequent years.”

Accordingly, Bhullar charges PLMR shares an Chubby (i.e. Purchase) whereas his $75 value goal makes room for 12-month upside of ~56%. (To look at Bhullar’s monitor report, click on right here)

The Avenue’s common goal is sort of the identical; at $75.40, the expectation is that the inventory will generate returns of 57% over the approaching 12 months. All in all, primarily based on an 3 Buys and Holds, every, the inventory claims a Average Purchase consensus ranking. (See PLMR inventory forecast on TipRanks)

TransUnion (TRU)

Subsequent up on our listing of JPMorgan low cost shares is TransUnion, a US credit score reporting company. Alongside Experian and Equifax, the corporate is taken into account one of many prime three credit score companies. Offering providers to greater than 65,000 shoppers in over 30 international locations, TransUnion gathers and combines knowledge on greater than a billion particular person shoppers, 200 million of which reside within the U.S. Client credit score studies, danger scores, analytical providers to mitigate danger, and decisioning capabilities to produce info throughout the buyer credit score lifecycle are among the many items and providers supplied by the corporate.

Within the newest quarterly report – for 3Q22 – income elevated by 26.2% year-over-year to $938 million, but that determine fell $7.58 million shy of the analysts’ forecast. Nevertheless, delivering adj. EPS of $0.93, the corporate managed to trump the $0.91 consensus estimate. For the fourth quarter, the corporate expects income within the vary between $896 million to $916 million, in comparison with Avenue expectations for $940.71 million. Adj. EPS is anticipated to be within the $0.80-$0.86 vary. Consensus had $0.91.

That, nonetheless, was not the explanation behind the inventory’s lackluster efficiency in 2022, throughout which the shares shed 52% of their worth. Typically talking, the backdrop of a softening shopper setting amidst rates of interest pushing larger isn’t nice information for credit score reporting companies. However JPMorgan’s Andrew Steinerman credit traders doubts across the acquisition of identification decision firm Neustar (closed December 2021) as the principle issue behind the shares’ decline.

Calling TRU his “favourite 2023 concept inside Data Companies,” the analyst lays out the bull-case for the expanded firm.

“We consider that the TRU inventory is simply too low cost to disregard and that its Neustar acquisition will improve the corporate’s anti-fraud and digital advertising and marketing capabilities within the years forward,” Steinerman stated. “We view Neustar as complementary to TRU’s knowledge analytics portfolio and suppose Neustar is enhancing TRU’s anti-fraud and digital advertising and marketing capabilities. In 2022, TRU had been integrating its knowledge property onto Neustar’s OneID platform, and in 2023, TRU plans to combine OneID into the corporate’s options to develop new joint merchandise. We acknowledge that the primary 12 months of integration has encountered some bumps alongside the highway, however we consider TRU will obtain its targets for Neustar to boost TransUnion’s natural income development and margins.”

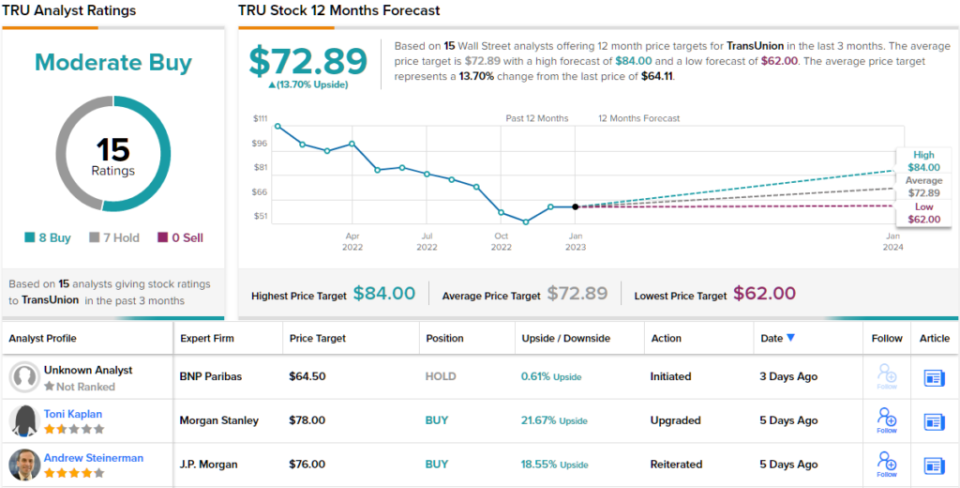

All instructed, Steinerman charges TRU shares an Chubby (i.e. Purchase), backed by a $76 value goal. The implication for traders? Upside of ~19% from present ranges. (To look at Steinerman’s monitor report, click on right here)

Wanting on the consensus breakdown, primarily based on 8 Buys vs. 7 Holds, the analysts’ view is that this inventory is a Average Purchase. Going by the $72.89 common goal, the shares will climb ~14% larger within the 12 months forward. (See TransUnion inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is vitally vital to do your personal evaluation earlier than making any funding.