zorazhuang

Targa Assets Corp. (NYSE:TRGP) is a pure fuel liquids-focused midstream company that primarily operates within the state of Texas. The midstream sector typically has lengthy been among the many favourite areas for income-focused traders to be resulting from the truth that most of those corporations get pleasure from remarkably steady money flows and excessive dividend yields. Targa Assets is one thing of an exception to this because it does have money circulation stability nevertheless it falls considerably quick by way of yield. In truth, the corporate solely yields 1.92% on the present value, which is because of a dividend in the reduction of in 2020 that was then partially reversed final 12 months. The corporate will doubtless enhance its dividend at a while sooner or later, which we are going to see over the course of this text. Though Targa Assets doesn’t benefit from the excessive yield that we sometimes wish to see right here at Power Earnings in Dividends, it has prior to now and should as soon as once more. This is the reason I proceed to debate this firm on my service. General, there are fairly a number of causes to speculate on this firm right this moment because it has made nice progress in overcoming a number of of the issues that it had lately and is thus positioning itself pretty properly for the long run.

About Targa Assets

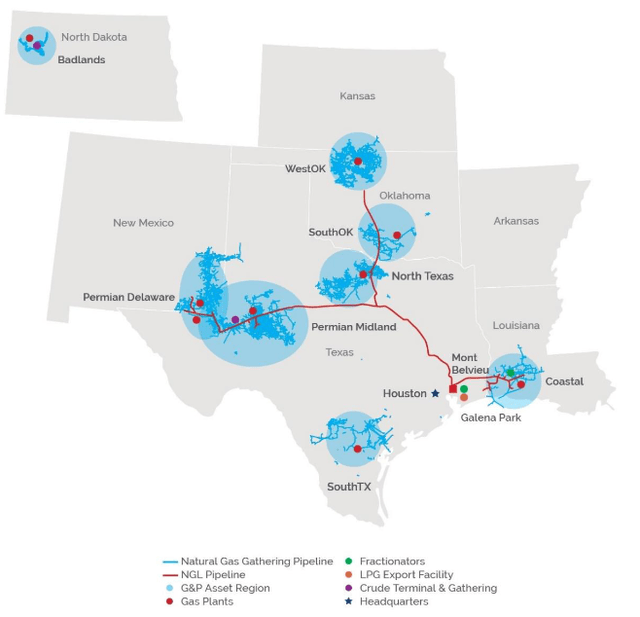

As acknowledged within the introduction, Targa Assets is a pure fuel liquids-focused midstream company that primarily operates within the state of Texas, though it does have some operations in North Dakota’s Williston Basin:

Targa Assets

In contrast to lots of its friends, although, we will see that the corporate’s pipeline infrastructure is pretty small. It is a bit deceptive nevertheless as Targa Assets truly has a reasonably substantial gathering and processing infrastructure community. A gathering pipeline is considerably totally different from the massive long-haul pipelines that carry sources throughout a state or a rustic. Moderately, these pipelines are pretty quick and low-capacity pipelines that merely seize the sources from the properly that extracts them from the bottom. The pipeline will then take the sources to the primary cease on their journey, which is often both a a lot bigger long-haul pipeline or a processing facility. Targa Assets does have a reasonably substantial pure fuel processing capability as it’s able to dealing with a complete of 11 billion cubic toes of pure fuel per day throughout its 53 processing crops. The processing of pure fuel is important as a result of pure fuel incorporates plenty of impurities and pollution when it’s faraway from the bottom, comparable to water and sulfur. The processing plant removes these impurities and converts the pure fuel right into a state that can be utilized by the top consumer. The corporate additionally owns 960,000 barrels per day of pure fuel liquids fractionation capability. A pure fuel liquids fractionator splits the sources into the assorted pure fuel liquids that we use in our on a regular basis lives, comparable to propane, butane, and ethane. General, then, Targa Assets is a reasonably main participant within the midstream house, though it doesn’t have substantial long-haul pipeline belongings.

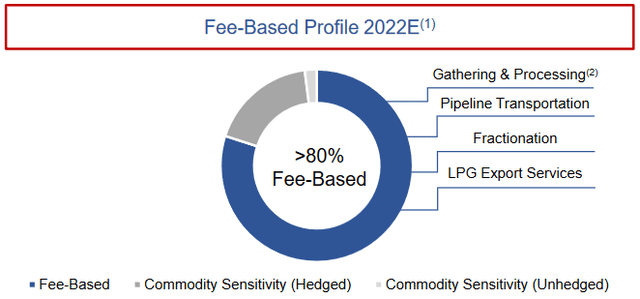

Within the introduction, I acknowledged that Targa Assets tends to get pleasure from remarkably steady money flows no matter situations within the broader economic system. That is because of the enterprise mannequin that the corporate makes use of. Briefly, Targa Assets enters into long-term (often 5 to 10 years in size) contracts with its clients. Underneath these contracts, the shoppers ship sources by Targa Assets’ infrastructure and compensate the corporate primarily based on the quantity of sources dealt with. This offers the corporate with a stunning quantity of insulation towards fluctuations in commodity costs. At this level, some readers would possibly level out that upstream useful resource producers have a tendency to scale back their output when power costs lower. This occurred again in 2020 when the COVID-19 pandemic broke out and brought on the demand for crude oil to plummet. Though Targa Assets doesn’t personal any crude oil infrastructure, pure fuel and pure fuel liquids are sometimes produced by the identical wells so the corporate would nonetheless be affected. Fortuitously, the corporate has a option to defend itself towards this. The contracts that it has with its clients include what are referred to as minimal quantity commitments, which specify a sure minimal quantity of sources that the client should ship by Targa Assets’ infrastructure or pay for anyway. Thus, it has a sure portion of its money circulation that’s usually unaffected by both power costs or useful resource manufacturing. In truth, 80% of the corporate’s working margin (a proxy for working revenue) comes from these recession-resistant contracts:

Targa Assets

That is one thing that’s sure to be engaging proper now as practically all economists agree that the American economic system will enter right into a recession someday in 2023. One of many traits of recessions is that the demand for power sources declines, which may affect the output of upstream producers a lot because it did again in 2020. The truth that greater than 80% of Targa Assets’ money flows are protected by this offers quite a lot of help for the corporate’s dividend and by extension our incomes.

We are able to see proof of this basic stability just by wanting on the firm’s working money flows over time. Right here they’re over the previous eleven quarters:

Searching for Alpha

This offers even additional proof that the corporate ought to have the ability to deal with any imminent recession with ease. In spite of everything, whereas its money flows did decline considerably in 2020, they nonetheless remained way more steady than could be anticipated contemplating what occurred to power costs throughout that 12 months. It’s all however sure that any recession that happens in 2023 is not going to be practically as extreme as it is rather unlikely that the federal government will as soon as once more try and lock us all down at dwelling and forbid us from pointless touring. Thus, power demand shouldn’t drop as a lot and we are going to doubtless not see practically as huge of a shock to the business.

Development Prospects

Naturally, as traders, we need to see greater than easy stability. We wish to see development. Fortuitously, Targa Assets is kind of well-positioned to ship on this space. As midstream infrastructure comparable to pure fuel gathering pipelines, processing crops, and fractionators solely have a restricted amount of sources that they deal with, and the corporate’s money circulation relies on the quantity of sources that transfer by its infrastructure, the traditional means for Targa Assets to generate development is to assemble new infrastructure. That is precisely what the corporate is doing, though it admittedly doesn’t have as many development tasks within the works as some friends comparable to Enbridge (ENB) or Kinder Morgan (KMI). One of many firm’s main tasks is the Daytona NGL Pipeline. The Daytona NGL Pipeline was introduced in November of 2022 and has an estimated value of $650 million. This undertaking was initially envisioned as a three way partnership with Blackstone Power Companions, though Targa Assets purchased out Blackstone’s stake final week. The Daytona NGL Pipeline is meant as an growth to the Grand Prix NGL system that constitutes one of many largest pure fuel liquids pipeline networks in Texas. The Grand Prix NGL system is able to carrying 550,000 barrels of pure fuel liquids per day however the Daytona NGL Pipeline is considerably lower than that as a result of it’s not the one pipeline that’s feeding your entire system. Throughout its third-quarter convention name, Targa Assets acknowledged that the Daytona NGL Pipeline can be able to carrying 400,000 barrels of pure fuel liquids per day when it begins working, though the corporate will have the ability to increase its capability if wanted. This form of expandable capability is kind of widespread because it helps to avoid wasting on development prices and future-proofs the undertaking. Clearly, these are issues that we should always respect as traders.

Targa Assets can be working to increase its pure fuel processing capability. Additionally in November 2022, the corporate introduced that it’ll start development of a brand new pure fuel processing plant to serve the Permian Basin. This new plant, dubbed Wildcat II, can be able to processing roughly 275 million cubic toes of pure fuel when it begins operation in early 2024. Because the Daytona NGL Pipeline is anticipated to come back on-line in late 2024, Targa Assets will thus be bringing a number of new tasks on-line throughout that 12 months.

The good factor about these tasks is that Targa Assets has already obtained contracts for his or her use from its clients. This serves two functions, each of that are helpful for the corporate. The primary of those functions is clearly that we will be assured that the corporate will not be spending an infinite sum of money to assemble infrastructure that no one needs to make use of. As well as, we will be sure that every of those tasks will start producing cash as quickly as they turn out to be operational in 2024 so we will anticipate regular development over the course of that 12 months from these two tasks coming on-line. The second goal is that the corporate is aware of upfront precisely how worthwhile the tasks can be so it is aware of that every undertaking will have the ability to generate a enough return to justify the funding. Sadly, Targa Assets has not specified precisely how worthwhile they are going to be so we can’t carry out an in-depth monetary evaluation presently. Kinder Morgan’s tasks often pay for themselves in 4 years whereas The Williams Corporations (WMB) has a few six-year payback so it’s doubtless that Targa Assets’ tasks are in that very same ballpark however that is under no circumstances sure. Regardless, we will be sure that they may present a really noticeable increase to the corporate’s money circulation.

Monetary Issues

It’s all the time important that we take a look at the way in which that an organization is financing itself earlier than we make an funding in it. It’s because debt is a riskier option to finance an organization than fairness as a result of debt have to be repaid at maturity. As few corporations have enough money readily available to fully repay their debt because it matures, that is sometimes completed by issuing new debt and utilizing the proceeds to repay the maturing debt. This will trigger an organization’s curiosity bills to extend following the rollover relying on the situations out there. Along with this, an organization should make common funds on its debt whether it is to stay solvent. Thus, an occasion that causes an organization’s money flows to say no might push it into monetary misery if it has an excessive amount of debt. Though Targa Assets has remarkably steady money flows, we should always not ignore this threat as bankruptcies have occurred within the midstream sector.

One metric that we will use to guage an organization’s monetary construction is the online debt-to-equity ratio. This ratio tells us the diploma to which an organization is financing its operations with debt versus wholly-owned funds. As well as, the ratio tells us how properly the corporate’s fairness will cowl its debt obligations within the occasion of a chapter or liquidation occasion, which is arguably extra essential.

As of September 30, 2022, Targa Assets had a web debt of $11.0646 billion in comparison with $4.7314 billion of shareholders’ fairness. This provides the corporate a web debt-to-equity ratio of two.34. At first look, this ratio appears extremely excessive for any firm however allow us to evaluate it to among the firm’s friends to get a greater thought of whether or not that is right:

Firm

Web Debt-to-Fairness

Targa Assets

2.34

Kinder Morgan

0.98

The Williams Corporations

1.62

MPLX (MPLX)

1.50

Crestwood Fairness Companions (CEQP)

1.51

Click on to enlarge

As we will clearly see, Targa Assets is relying significantly extra on debt to finance its operations than any of its friends. It is a clear signal that the corporate is utilizing an excessive amount of leverage and thus might have better dangers of monetary misery than lots of its friends. That is, in truth, one of many issues that we’ve had with respect to this firm. I’ve mentioned this in lots of earlier articles right here at Power Earnings in Dividends.

In the end although, the corporate’s capacity to hold its debt is extra essential than the sheer quantity of debt. The same old means that we decide that is by wanting on the leverage ratio, which is also referred to as the online debt-to-adjusted EBITDA ratio. This ratio primarily tells us what number of years it can take for the corporate to fully repay its debt if it have been to commit all of its pre-tax money circulation to that job. Within the third quarter of 2022, Targa Assets reported an adjusted EBITDA of $768.6 million, which works out to $3.0744 billion yearly. This provides the corporate a leverage ratio of three.60x, which is kind of cheap. As I’ve identified in varied earlier articles, analysts usually contemplate something underneath 5.0x to be cheap however I’m extra conservative and wish to see this ratio underneath 4.0x with a purpose to add a margin of security to the funding. All the advisable corporations right here at Power Earnings in Dividends are properly underneath this 4.0x threshold however traditionally Targa Assets has not been. The corporate now seems to be, which is definitely good to see. The largest purpose why Targa Assets minimize its dividend again in 2020 was to repay its debt and it has seemingly loved quite a lot of success at this job. That is due to this fact fairly good to see.

Dividend Evaluation

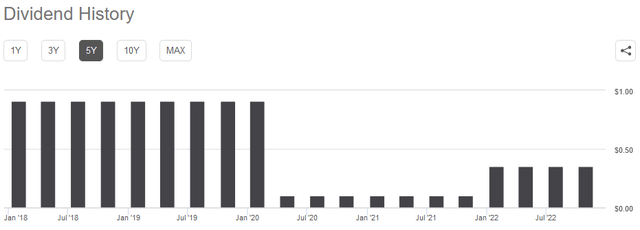

One of many greatest the explanation why we put money into midstream corporations is the excessive dividend yields that these corporations are likely to pay out. Targa Assets is sadly a notable exception to this rule as the corporate solely yields 1.92% at its present value. It’s because the corporate minimize its dividend again in 2020 and, whereas it did enhance it in early 2022, it nonetheless stays properly under its peak:

Searching for Alpha

Along with this, the corporate’s inventory has appreciated by 28.31% over the previous twelve months, which has additionally suppressed the yield considerably. The truth that the corporate did minimize its dividend in 2020 is more likely to be a little bit of a turn-off, particularly since there are various different midstream corporations that didn’t want to chop their payout. Nevertheless, it is very important understand that anybody buying the corporate’s shares right this moment will obtain the present dividend on the present yield and so does not likely want to fret in regards to the firm’s disappointing previous. Subsequently, the essential factor for our functions is how properly the corporate can preserve its present dividend. In spite of everything, we don’t need to discover ourselves the victims of one other dividend minimize since that would scale back our incomes and nearly definitely trigger the inventory value to say no.

The same old means that we decide a midstream firm’s capacity to pay its dividend is by taking a look at its distributable money circulation. Distributable money circulation is a non-GAAP determine that theoretically tells us the amount of money that was generated by the corporate’s peculiar operations and is obtainable to be distributed to the widespread stockholders. Within the third quarter of 2022, Targa Assets reported a distributable money circulation of $594.9 million however solely paid $81.0 million in dividends. This provides the corporate a distribution protection ratio of seven.34x, which is way above the 1.20x that analysts sometimes contemplate cheap and sustainable. It is usually properly above the standard 1.30x that we wish to see from an organization that we’re invested in. This extremely excessive protection ratio is without doubt one of the the explanation why I recommended earlier on this article that Targa Assets might enhance its dividend in some unspecified time in the future since it may clearly afford to and appears to have gotten its debt considerably underneath management. We must always total not have to fret in any respect a few minimize right here.

Conclusion

In conclusion, Targa Assets may definitely have potential regardless of not being a high-yielding inventory. The corporate has made nice strides at addressing the debt issues that we’ve had in regards to the firm prior to now, though the debt-to-equity ratio is unquestionably nonetheless a bit excessive. The corporate additionally has some vital development prospects which are more likely to play out over the following two years. After we mix this with an actual probability of a dividend enhance, we will see some actual causes to buy the corporate right this moment.

{kind=link}