monsitj

CVS Well being (NYSE:CVS) is without doubt one of the shares for which I see excessive development potential within the years to return. For my part, the inventory is clearly undervalued and will commerce a lot larger. I do know it typically takes time for a inventory to return to its intrinsic worth (really, shares fairly seldom commerce for his or her intrinsic worth however are largely over- or undervalued). However, CVS continues to commerce clearly beneath the intrinsic worth I calculate for the inventory and it’s a bit irritating.

It’s not that I get impatient. CVS is paying me a quarterly dividend and my place, which I inbuilt 2019 and 2021 is up about 65% and each positions clearly outperformed the S&P 500 (SPY). My 2019 place greater than doubled the efficiency of the S&P 500 and the 2021 place returned 38% whereas the S&P 500 returned 5% in the identical timeframe.

And even when being actually assured a couple of place – or particularly then – we should always query our thesis regularly and ask ourselves if our premises, our assumptions and our conclusion are right. So: Am I fallacious about CVS?

Valuation

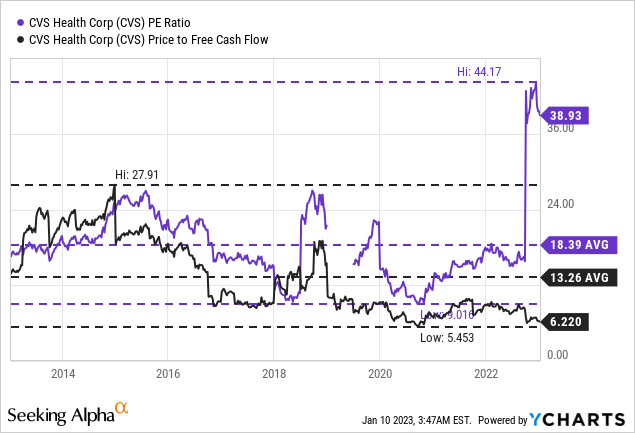

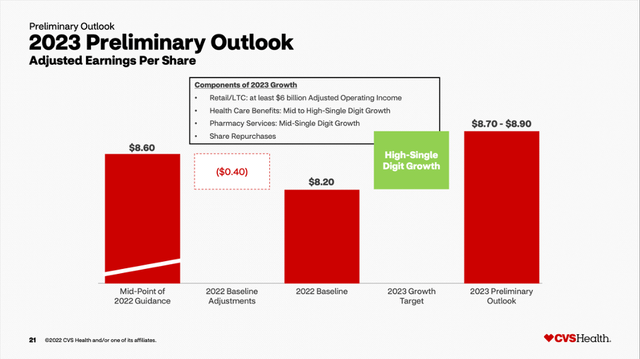

We may begin by taking a look at easy valuation metrics and with a price-earnings ratio of 39, the inventory appears to be clearly overvalued. However to clarify that fairly excessive P/E ratio we should take into consideration the opioid litigation and recorded pretax costs of $5.2 billion for authorized settlements (we’ll get to this). When wanting on the adjusted numbers as a substitute (administration is anticipating adjusted EPS to be round $8.60) we get a P/E ratio of solely 10.6.

And one may now argue to not use adjusted numbers however when wanting on the price-free-cash-flow ratio we see even decrease valuation multiples. Based on the chart above, CVS is buying and selling for less than 6.2 instances free money stream. This isn’t solely beneath the 10-year common of 13.26, however a particularly low valuation a number of for any enterprise that’s wholesome and rising. Nevertheless, I don’t actually know the way that metric was calculated. CVS Well being is anticipating free money stream for fiscal 2022 to be round $11.1 billion (midpoint of steering) which might result in a P/FCF ratio of 11 – nonetheless very low-cost.

As common, I’ll pay extra consideration to a reduction money stream calculation to find out an intrinsic worth for the inventory. Administration is anticipating free money stream to be $11.1 billion in fiscal 2022 (midpoint of present steering). And from now until perpetuity let’s assume 5% development (much like my earlier articles about CVS). When calculating with these assumptions and a ten% low cost price in addition to 1,315 million in excellent shares we get an intrinsic worth of $168.82 for CVS and the inventory would commerce about 45% beneath its intrinsic worth.

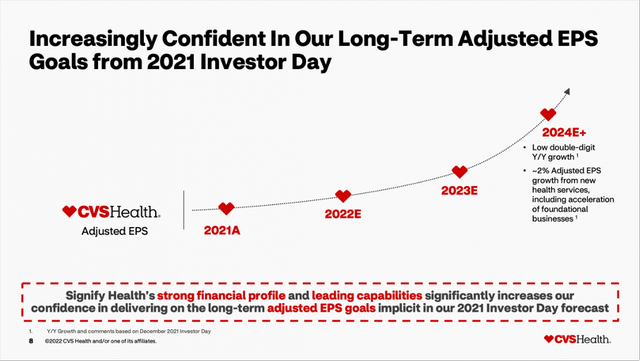

And the idea of 5% annual development can also be in-line with previous development charges in addition to the corporate’s long-term steering. When taking a look at previous development charges, CVS grew with a CAGR of 8.76% within the final ten years. And since 2000, earnings per share grew with a CAGR of 9.30% and since 1990 earnings per share grew with a CAGR of 6.28%. When taking a look at these development charges, 5% development until perpetuity appears cheap. And administration is much more optimistic within the years to return. From 2024 going ahead, the corporate is anticipating earnings per share to develop within the low double digits year-over-year.

CVS Signify Well being Acquisition Presentation

We are able to additionally supply a distinct perspective. Even when CVS just isn’t capable of develop within the years to return, the intrinsic worth could be $84.41, and the inventory would virtually be pretty valued. And don’t overlook: That is calculated with a ten% low cost price and due to this fact assuming a return on our funding of 10% yearly, which continues to be strong.

Quarterly Outcomes

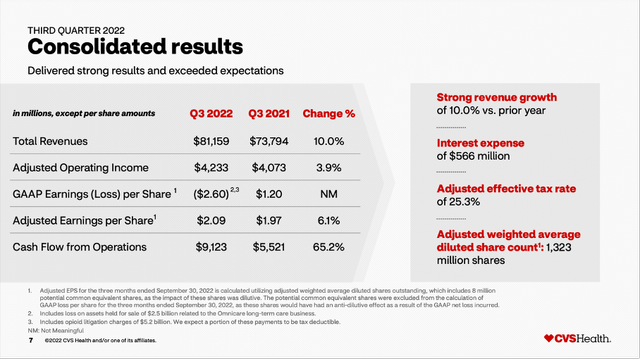

One more reason for a poor efficiency could possibly be quarterly outcomes and CVS disappointing buyers. However not solely did CVS beat estimates for earnings per share in addition to income, the outcomes had been additionally strong. Income elevated from $73,794 million in Q3/21 to $81,159 million in Q3/22 – leading to 10.0% year-over-year development. However whereas the highest line may improve with a strong tempo, CVS needed to report an working lack of $3,931 million in Q3/22 – as a substitute of an working revenue of $3,061 million in Q3/21. And diluted earnings per share additionally “switched” from $1.20 earnings per share in Q3/21 to $2.60 loss per share in Q3/22.

CVS Q3/22 Presentation

Adjusted earnings per share nevertheless elevated 6.1% year-over-year from $1.97 in Q3/21 to $2.09 in Q3/22. And the foremost cause for the destructive working revenue and loss per share (in line with GAAP) are $5,220 million in opioid litigation costs (we’ll get again to this).

When wanting on the totally different segments, all three may contribute to development. Retail/LTC generated $26,706 million in income (reflecting a rise of 6.9% YoY development) and Pharmacy Service Segments reported a income of $43,216 million (a rise of 10.7% year-over-year). Lastly, the Well being-Care Advantages Section reported a income of $22,511 million (leading to a rise of 9.9% YoY).

CVS Q3/22 Presentation

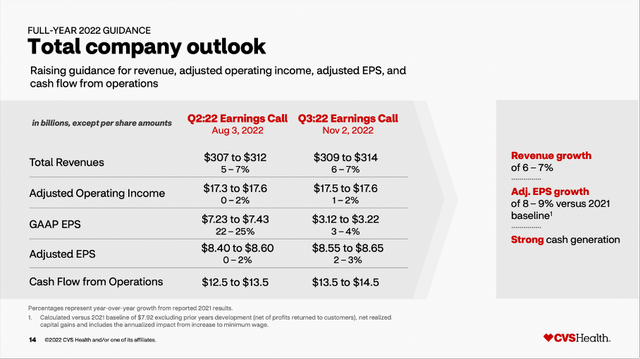

One more reason for a mediocre efficiency could possibly be a lowered steering. However CVS raised its steering – for income, adjusted EPS and money stream from operations. Solely GAAP EPS estimates needed to be decrease. Moreover, CVS additionally seems barely optimistic for 2023.

CVS Q3/22 Presentation

Recession

One more reason for the efficiency could possibly be the looming recession. However previously, CVS was fairly recession resilient (I’m not essentially speaking in regards to the inventory worth). I already argued in my previous article that CVS may stand up to previous recessions fairly effectively and can most definitely carry out strong within the subsequent potential recession.

Opioid Litigation

We already talked about the opioid litigations briefly – and so they could possibly be another excuse for the mediocre inventory worth efficiency and a cause why CVS is buying and selling for such an enormous low cost (for my part). Firstly of November 2022, it was additionally reported that CVS is near settlement of practically all opioid-related lawsuits and claims. Over the last earnings name, administration commented on the method:

This morning, we made an essential announcement on our ongoing opioid authorized matter. In late October, we started a mediation to resolve considerably all opioid lawsuits and claims towards CVS Well being by states, political subdivisions and tribes. We reached an settlement in precept to pay roughly $5 billion over 10 years starting in 2023, an end result that’s in the most effective curiosity of all events and one that may assist put a a long time previous concern behind us as we proceed to concentrate on delivering a superior well being expertise for the hundreds of thousands of customers who depend on us.

If the deal is finalized, CVS must pay about $5 billion to states and political entities, however the funds will likely be unfold over the subsequent ten years (beginning in 2023). CVS has already reported $5.2 billion in pre-tax opioid litigation costs within the third quarter of fiscal 2023 resulting in a GAAP loss per share of $2.60.

Acquisition

When on the lookout for additional explanation why CVS Well being continues to be buying and selling beneath what I contemplate a good worth for the inventory, we are able to additionally point out acquisitions. Perhaps buyers assume that acquisitions are a mistake (which is usually true) that don’t add a lot worth to an organization – or CVS Well being on this case.

In the previous couple of quarters, CVS Well being generated numerous headlines on account of acquisitions, potential acquisitions, and rumors about acquisitions. And contemplating that the acquisition of Aetna was one of many main causes the inventory tanked and clearly underperformed since 2016, CVS as soon as once more making (main) acquisitions would not appear to be the most effective information for buyers – it is also one of many explanation why the inventory is buying and selling clearly beneath its intrinsic worth for my part (we’ll get to that). Alternatively, acquisitions have been part of CVS’s technique for a very long time – in 2015 the corporate acquired Omnicare in addition to 1,600 pharmacies from Goal (TGT). And the Aetna acquisition has additionally been a significant success – for my part.

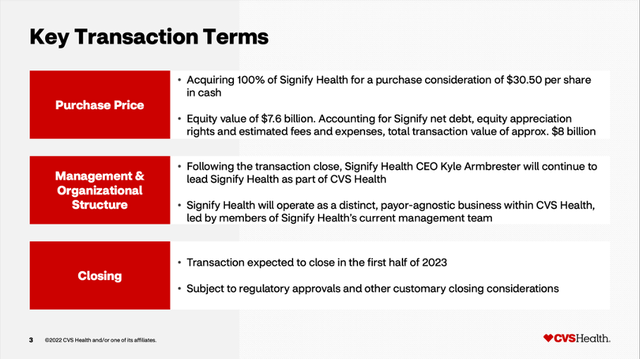

In September 2022, the corporate introduced the acquisition of Signify Well being (SGFY) and bought the corporate for $30.50 per share leading to a complete transaction worth of roughly $8 billion (together with web debt in addition to estimated charges and bills). The acquisition was paid all in money from CVS’ steadiness sheet.

CVS Signify Well being Acquisition Presentation

The transaction is predicted to shut within the first half of 2023 and the deal will add about 10,000 contracted docs and clinicians to CVS Well being. It was additionally reported that different corporations had been fascinated about Signify Well being as effectively – together with UnitedHealth (UNH) and Amazon (AMZN).

And apart from this particular acquisition, there have been many rumors and talks about potential acquisitions. Because the summer season of 2022, there have been rumors a couple of potential acquisition of Cano Well being (CANO). Firstly of October 2022, it was reported that CVS Well being is in unique talks to amass Cano Well being, however about two weeks later it was reported that CVS walked away from the deal and as consequence Cano Well being went into freefall. I don’t know if that is the tip of story, however Cano Well being could be extraordinarily low-cost (and greater than 90% beneath the implied price of $14 per share).

However, CVS Well being seems nonetheless fascinated about acquisitions within the major well being care house and on Monday it was reported that Oak Road Well being (OSH) could be a possible goal. Oak Road Well being is providing healthcare companies and operates about 130 major care facilities in 19 totally different states. The corporate has been seen as a possible acquisition goal for a number of months and it was already speculated about CVS being a possible purchaser. Speculations see a deal being price about $10 billion, which might be an enormous premium in the marketplace cap of about $5 billion earlier than the primary information broke.

Steadiness Sheet

I don’t know the way to place myself in the direction of one other acquisition. On the one hand, CVS Well being is producing greater than $10 billion in free money stream yearly and on September 30, 2022, it had $17,197 million in money and money equivalents on its steadiness sheet in addition to $2,792 million in short-term investments. CVS Well being nonetheless should pay about $8 billion for the acquisition of Signify Well being leading to about $12 billion in liquid belongings for an additional acquisition.

Therefore, CVS Well being wouldn’t have so as to add debt to its steadiness sheet – even when it could purchase Oak Road Well being for $10 billion – and I actually don’t wish to see further debt on the steadiness sheet. CVS Well being ought to fairly concentrate on decreasing debt ranges. It nonetheless has $1,363 million in short-term debt in addition to $50,848 million in long-term debt. When evaluating the whole debt to the whole stockholder’s fairness of $71,011 million we get a debt-equity ratio of 0.74 – which is appropriate. However when evaluating the whole debt to the trailing twelve-month working revenue of $14,788 million it could nonetheless take about 3.5 years to repay the excellent debt. That is no cause for concern, however I want to see CVS carry down its debt ranges additional – particularly contemplating $78,066 million in goodwill on the steadiness sheet (a particularly excessive quantity for a $120 billion market cap firm).

CVS Investor Story Deck

In fact, CVS Well being will handle to repay its excellent debt and will additionally pay for an additional acquisition. I identical to to see administration make sensible and strategic determination by buying nice companies for an affordable worth – and never simply purchase corporations to proceed rising.

Additional Dangers

And naturally, there are a lot of further dangers and headwinds. Nevertheless, I don’t see any of them as an issue CVS Well being can’t deal with. Till 2024, CVS is planning to shut about 900 shops and naturally, this isn’t the most effective information, however doesn’t create an enormous downside immediately and might result in larger profitability for the present shops in a couple of years from now.

One other downside could possibly be the mediocre star scores CVS acquired from the Heart for Medicare & Medicaid Providers in early October. Within the 8-Ok the corporate said:

On October 6, 2022, the Facilities for Medicare & Medicaid Providers (“CMS”) launched its 2023 Star Scores for Medicare Benefit (“Medicare Half C”) and Medicare Half D prescription drug plans. Primarily based on the newly launched 2023 Star Scores, which is able to influence revenues in 2024, the proportion of Aetna Medicare Benefit members in 4+ Star plans is predicted to drop to 21% (primarily based on present enrollment and contract affiliation), as in comparison with 87% primarily based on the 2022 Star Scores. The primary driver of this lower was a 1 Star lower within the Aetna Nationwide PPO, which dropped from 4.5 to three.5 Stars, whereas many different Aetna plans stay rated at 4+ Stars.

Consequently, the inventory fell about 4.7% throughout pre-market buying and selling that day. However over the past earnings name, administration was optimistic that the destructive influence in 2024 will nonetheless be manageable for CVS:

Let me speak in regards to the ’24 headwinds a little bit bit extra particularly. We mission the mixed influence of [stars] (PH) and Centene on 24 to be roughly $2 billion on an unmitigated foundation. My feedback at the moment concerning repurchases and reaching our Investor Day commitments assume that we’re profitable in mitigating roughly half of this headwind. And that work is in course of and underway, however not 100% sure at this stage. That would depart a headwind of about $1 billion or $0.55 a share for 2024.

And eventually, CVS is going through reimbursement headwinds and a change of the regulatory surroundings can have a big impact on the enterprise – at the very least in concept.

Conclusion

No doubt, there are a number of dangers and headwinds for CVS proper now. However for my part none of those dangers can have a big impact on CVS’ enterprise and will hold CVS from rising at the very least within the low single digits. The opioid litigations appear virtually settled (and is already included within the Q3/22 outcomes), CVS can stand up to recessions fairly effectively and as a enterprise working within the healthcare sector it shouldn’t be affected a lot by recessions. All in all, CVS is a transparent purchase for my part and will reward buyers at the very least with double-digit returns within the years to return.

{kind=link}