Derick Hudson

1. Introduction

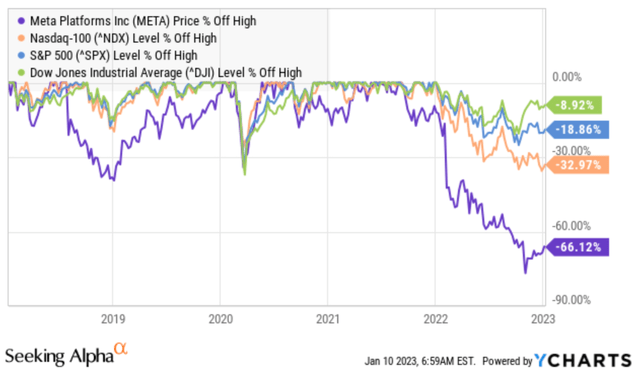

We’re within the midst of a bear market and Meta Platforms (NASDAQ:META) collapsed round 62% from its 52-week-high of $337.

Consequently, Meta has underperformed all the most important indices, such because the S&P 500, Dow Jones as properly because the Nasdaq (see chart).

Value % off excessive – Meta vs main indices (YCharts)

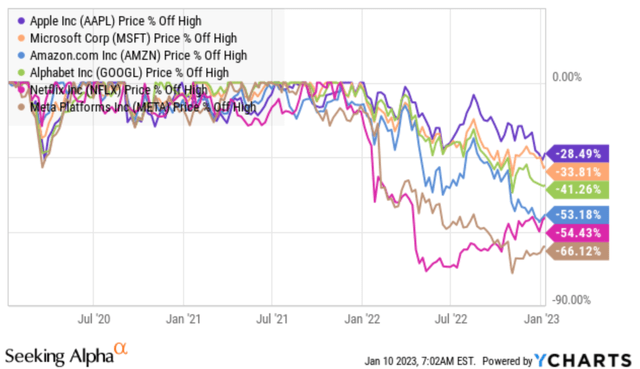

Meta has additionally vastly underperformed its so-called FAANG friends (see chart).

Meta vs so-called FAANG friends (YCharts)

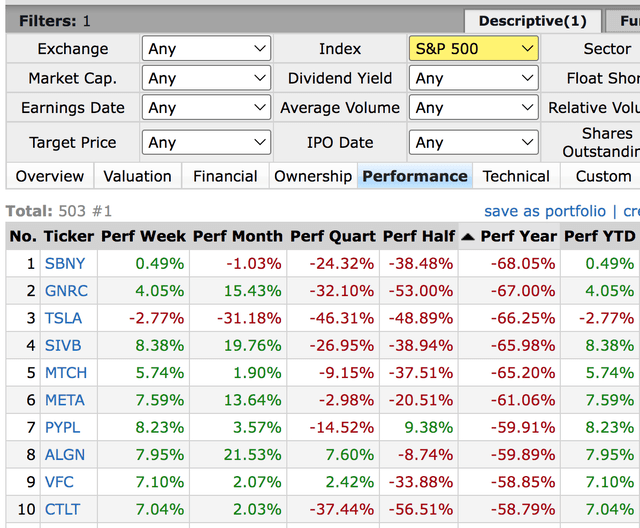

Moreover, Meta is among the many 10 worst performing S&P 500 shares in the middle of the final 12 months (see chart).

Meta vs. S&P 500 shares (Finviz)

So, is now a tempting alternative to purchase?

2. Elementary Evaluation

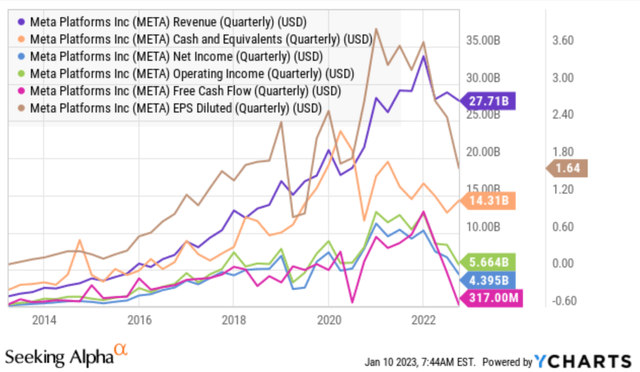

As you’ll be able to see within the following determine, Meta’s key efficiency metrics are deteriorating since 2021. With key efficiency metrics I imply revenues, money & money equivalents, internet earnings, working earnings, free money circulate and earnings per share.

I count on the deterioration to accentuate if the macroeconomic surroundings worsens, i.e. we enter right into a recession, or administration retains struggling to show the tide.

Meta key efficiency metrics deteriorate since 2021 (YCharts)

3. Technical Evaluation

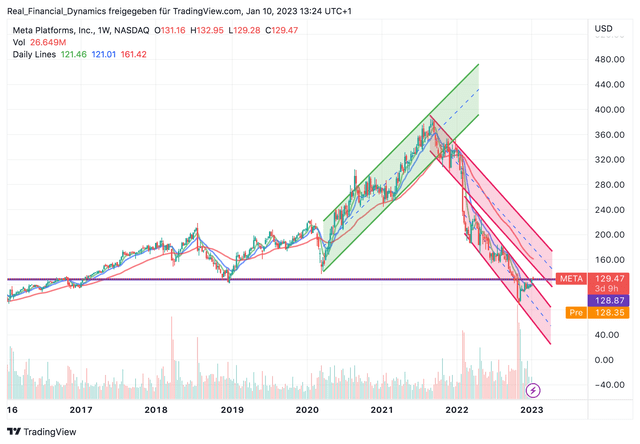

Wanting on the chart, it’s placing that Meta is caught in a downtrend, which favors an extra decline within the share value (see following chart).

At one level, the share value had even accelerated its downtrend and entered a steeper downtrend (see decrease crimson channel within the chart).

On the one hand, the inventory erased all Publish-COVID good points. Then again, for those who have a look at Meta’s historic value actions, the present value may function a assist and/or resistance.

Nevertheless, the inventory appears to be making an attempt a break-out from the steeper downtrend to the upside. A break-out above may briefly transfer the inventory to round $166 (the higher line of the primary downtrend channel). A failure and shut under $129, nevertheless, may result in a a lot additional collapse.

Consequently, the risk-reward ratio would not appear very tempting but from a technical viewpoint.

Meta weekly chart – caught in a downtrend (TradingView)

4. Honest Worth Calculation

I ready two valuation fashions as a way to make a extra correct evaluation of the valuation. I’ve chosen a conservative strategy because of the financial tightening section of central banks on a worldwide scale and the associated quickly rising rate of interest surroundings. Different components favoring a conservative strategy embrace the unsure macroeconomic and political surroundings and rising recession dangers, which have in all probability not but been absolutely priced in.

Moreover, settle for it or not, Meta at the moment has a struggling enterprise mannequin and Zuckerberg is making an attempt to re-invent the corporate. Moreover, the promoting enterprise, the place Fb generates 98% of its revenues, is cyclical and subsequently weak to financial cycles.

Given the deteriorating key efficiency metrics and resulting from a turnaround hypothesis, I’ve chosen a development price of 0% in each valuation fashions. Why? As a result of as a (worth) investor I desire a affordable margin of security and it’s tough to estimate when Zuckerberg will reach turning the tide once more.

Moreover, I’ve chosen 12% because the low cost price. Meta has sturdy financials with $42 billion in money, however as we now have seen, the money is at the moment melting away and the online debt place is deteriorating for the third yr now (see following chart).

Meta whole and internet debt (Searching for Alpha)

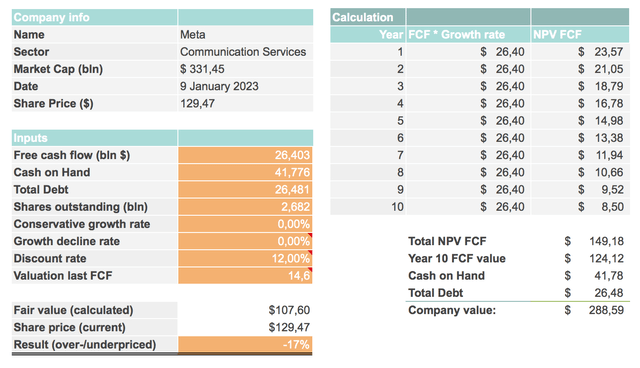

The primary valuation methodology is predicated on a DCF calculation. When it comes to Value/Money circulate a number of, I’ve chosen a a number of of 14.60 for the final FCF, which represents the present common FCF a number of of the S&P 500 and is properly above Meta’s present FCF a number of of 6.56 however near its 5-year-average of 16.80, in line with Morningstar.

Within the first valuation methodology based mostly on a DCF calculation, the honest worth is $107.60, which corresponds to an overvaluation of the inventory of 17% (see determine under).

Meta honest worth calculation based mostly on DCF (Writer’s calculation)

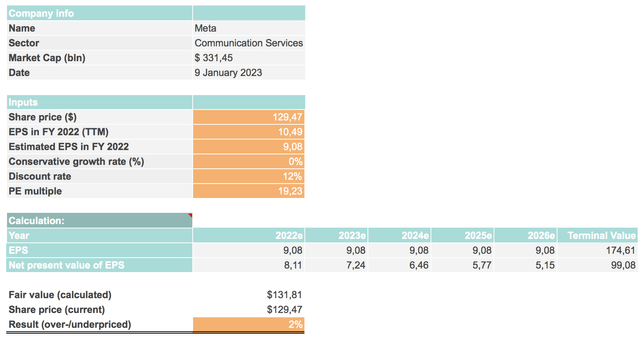

The second valuation methodology is predicated on an earnings-per-share calculation. When it comes to P/E a number of, I’ve chosen a a number of of 19.23 for calculating the terminal worth, which represents the present P/E a number of of the S&P 500 and is properly above the present P/E a number of of Meta of 12.35, in line with Morningstar.

Within the second valuation methodology the honest worth is $131.81, which corresponds to a slight undervaluation of the inventory of two% and thus signifies a present honest valuation (see determine under).

Meta honest worth calculation based mostly on EPS (Writer’s calculation)

5. Conclusion

In abstract, the elemental, technical and enterprise development at Meta is clearly pointing downwards.

So long as Zuckerberg doesn’t reach turning the tide, the inventory will in all probability not have the ability to get better sustainably any time quickly.

Whereas Fb is turning into more and more out of date for at this time’s younger individuals, Meta has additionally did not invent or purchase one other notable money cow apart from the Instagram acquisition.

Whereas prices additionally appear to have run uncontrolled prior to now, margins, money circulate and earnings are actually dwindling as properly.

In the long run, I may think about a split-up of Meta if the turnaround won’t achieve success. In my view, Zuckerberg at the moment has just one possibility to show issues round: land a fortunate coup just like the Instagram takeover.

My honest worth calculation based mostly on a DCF methodology exhibits a present overvaluation of 17% and my honest worth calculation based mostly on an EPS methodology signifies a good valuation, leaving no margin of security.

The present unsure macroeconomic surroundings and the central banks’ speedy financial tightening course of ought to additional weigh on the inventory.

Consequently, the risk-reward ratio appears far too unhealthy to contemplate an funding on the present stage.

To conclude, it’s unhappy to say that Meta first reworked from a superior development inventory to a worth funding and now has change into a speculative turnaround guess.

{kind=link}