Vladimir Zakharov

In a bleak 12 months for fairness traders globally, a number of rising markets (EMs) have been among the many finest performers on a relative foundation. Though the financial and financial photos differ dramatically amongst EMs, creating economies broadly are additional forward than developed markets in their financial tightening and fairness derating cycles.

This cyclical positioning and the resilient macroeconomic fundamentals of EMs lead us to imagine that EMs are higher positioned for fairness positive aspects in 2023 than developed economies.

We look at key financial and funding themes dealing with EM traders and spotlight a number of vital areas. We additionally have a look at the long-term tendencies we imagine are creating an more and more engaging EM funding alternative set for fairness traders.

5 Themes Shaping the EM Fairness Panorama

Lots of the core points confronting developed markets—inflation, financial tightening, equity-market derating, and downward earnings changes—are taking part in out in another way in EMs. In lots of circumstances, EMs are additional alongside in working by way of these points, creating optimism for traders.

Inflation

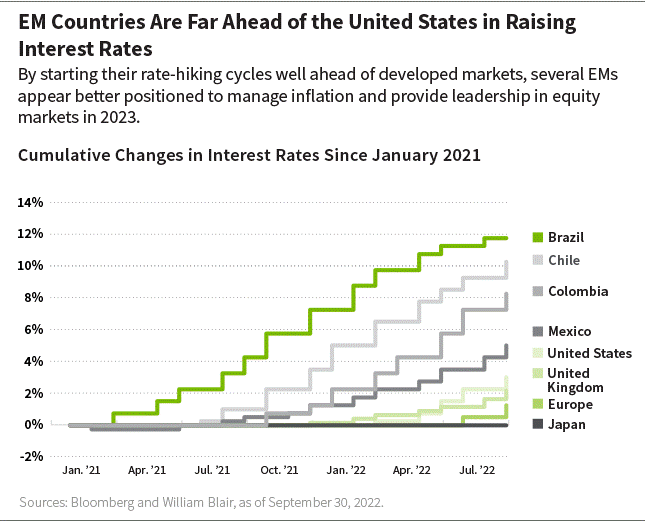

EM economies, usually, have much less of an inflation downside than developed economies. This offers EM central banks extra coverage choices, together with restimulating into a worldwide downturn.

Brazil, Mexico, and different Latin American nations started elevating rates of interest effectively earlier than america and Europe. Brazil moved furthest; its coverage charge was 13.75% as of October 2022, which explains why the Brazilian actual has been the top-performing forex towards the U.S. greenback in 2022, up 7.3% by way of November 2022. Inflation charges in these nations stay average to excessive however have began to development down. All of those nations exhibit constructive actual rates of interest, in contrast to america and Europe.

Inflation in Asia is comparatively modest. China, particularly, is experiencing inflation effectively under the EM common, giving Chinese language policymakers room to change into much more stimulatory in 2023.

Valuations and Earnings Estimates

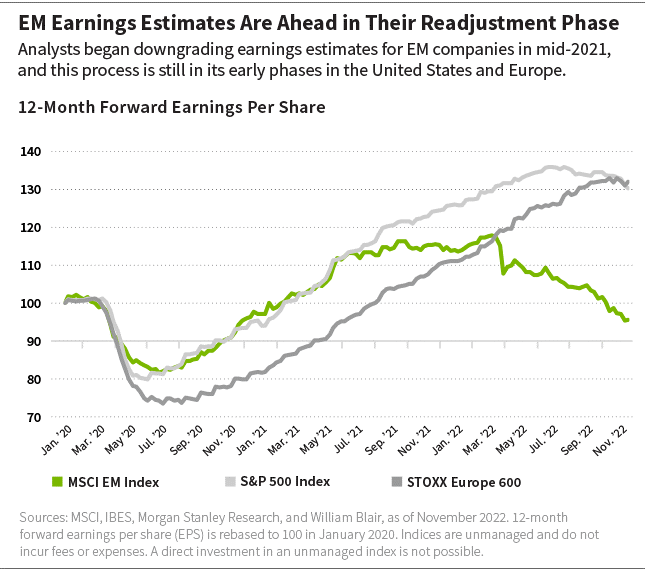

Equities have already derated in lots of EMs, suggesting that these nations at the moment are within the late phases of a bear market. They appear now higher positioned for a rebound, particularly provided that we anticipate interest-rates cuts and different stimulative measures to come back in 2023.

Many metrics recommend that the EM bear market is getting lengthy within the tooth. Traditionally, the common EM bear market has lasted 263 days and produced a 38.2% drawdown, in response to Morgan Stanley. The present EM bear market, which started in February 2021 when China tech shares peaked, is sort of 600 days previous, and the MSCI EM Index was down 40% heading into October 2022.

EM valuations have derated 39% versus a mean of 34% for EM bear markets, and EM earnings estimates have been downgraded sharply in 2022, in distinction to america and Europe, the place the damaging earnings revision course of has barely begun.

Given the mixture of value declines, the derating of valuation multiples, and earnings estimate cuts, we imagine that EM fairness markets have already readjusted and are higher positioned for restoration than developed markets. Some choose EM fairness markets have already been among the many prime performers globally in 2022 by way of November, amongst them Brazil (+17.64%), Mexico (+5.12%), and India (–2.62%), in response to Bloomberg.

Forex Change Charges

EM equities usually underperform when the U.S. greenback is powerful. We imagine that the U.S. greenback is probably going near peaking, which could possibly be a bullish sign for EM equities.

As an asset class, the relative efficiency of rising markets tends to be negatively correlated with a powerful U.S. greenback. Because the greenback rises, EM equities are inclined to underperform as a result of their currencies come underneath stress, and these nations should increase rates of interest to guard the alternate charge. As soon as the greenback peaks, that stress abates—financial coverage can loosen, and

fairness markets usually rerate larger. We anticipate the U.S. greenback to peak, which might possible flip a headwind right into a tailwind for EM equities in 2023.

Model Rotation

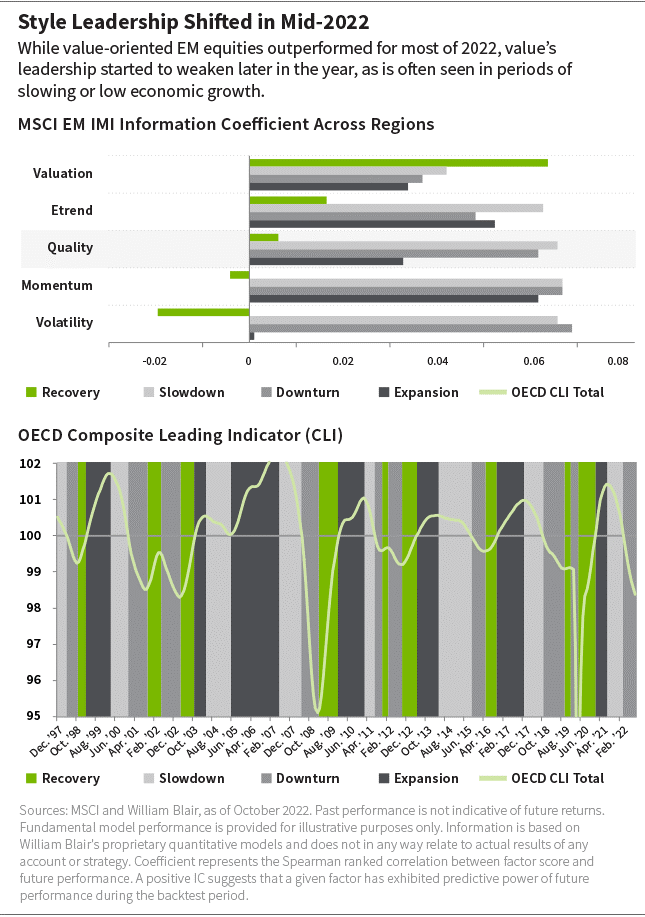

There was a current shift in management amongst EM type components, with the outperformance of value-oriented equities beginning to abate considerably.

EM worth shares outperformed within the first half of 2022, as is typical when rates of interest rise. Since then, the worldwide financial regime has switched from “slowdown” to “downturn,” as outlined by the Organisation for Financial Co-operation and Improvement (OECD) composite main indicator, and different fairness components have taken management—specifically high quality, earnings development, and momentum.

In an financial downturn, higher-growth EM shares which have derated and have sturdy and steady earnings might outperform, in our opinion. Sturdy earnings are normally rewarded in a downturn as a result of most firms’ earnings progress tends to weaken and/or decline because the financial downturn progresses. Increased-quality firms usually do higher underneath monetary tightening as a result of they’ve both (A) simpler entry to credit score or (B) stronger steadiness sheets and are usually self funded. Low-volatility shares are at a premium as a result of they’re extra defensive and fewer uncovered to cyclicality.

EMs of Curiosity

China

The expansion outlook stays muted and cloudy whereas zero-COVID insurance policies persist. However the completion of the current Nationwide Congress might present readability and lift the potential of extra stimulative financial and monetary insurance policies in addition to a roadmap out of zero-COVID insurance policies.

Chinese language equities have been among the many worst performers in 2022, and valuations are at a 15-year low. The federal government’s zero-COVID coverage is way guilty, creating uncertainty and pessimism and inflicting shopper confidence to break down. The federal government has offered some stimulus however not sufficient to offset the influence of zero-COVID.

Different considerations embrace the federal government’s concentrating on of expertise firms and its reticence to deal with the property market points, coupled with uncertainty as to the financial influence of the nation’s Widespread Prosperity doctrine, which is meant to advertise equality.

Now that the twentieth Nationwide Congress of the Chinese language Communist Social gathering wrapped up in late October 2022, celebration management could have a freer hand to deal with financial progress, setting the stage for China to loosen up zero-COVID insurance policies and enhance financial stimulus. As this happens, we imagine the Chinese language fairness market could possibly be set to outperform.

Because of this, we raised our weighting in China in late 2022. We’re nonetheless underweight China however much less so than we have been beforehand. Valuations seem engaging, and we’re cautiously constructive on potential coverage adjustments forward and early indicators of a roadmap out of zero-COVID, extra definitive assist for the property market, and the economic system usually.

India

The nation enjoys very favorable fundamentals, together with sturdy financial progress, a pro-business authorities, and a big and rising center class of greater than 300 million folks. However we acknowledge that a few of these are factored into the Indian fairness market’s valuation premium.

Regardless of its valuation premium versus different EMs, we’re obese India. In our view, its positives embrace favorable demographics, a well-educated inhabitants, sturdy financial progress, a pro-business authorities, and an English authorized system and a comparatively excessive diploma of visibility into how financial and monetary insurance policies are executed.

We imagine rising per-capita earnings and a rising center class are persistent structural tailwinds for Indian fairness markets. When per-capita earnings crosses the $2,000 mark, creating nations usually see an explosion of demand for shopper items and providers, from family home equipment to mortgage loans. India is at that inflection level—over 40% of the inhabitants is already there, and that is anticipated to rise to 60% by 2025, in response to Spark Capital.

Inflows from home retail traders additionally act to underpin Indian fairness markets. Systematic funding plans (SIPs) that robotically spend money on mutual funds have change into wildly in style. The share of equities in family financial savings is at an all-time excessive of round 5%, having been as little as 2.5% just a few years in the past—however it nonetheless has an extended technique to develop earlier than approaching the degrees of extra developed nations.

In India, we’re constructive on financials and housing-related shares. Within the monetary sector, penetration ranges of monetary merchandise are extraordinarily low and set to rise together with the rising center class. As well as, high-quality private-sector banks during which we make investments have the potential to take an enormous quantity of market share from public-sector banks that also management almost 70% of the Indian monetary sector. In housing, affordability is at a 10-year excessive, and the market is booming, which we imagine are constructive tailwinds for our Indian monetary and property-development firms.

Different EMs to Watch

Brazil: Brazil raised rates of interest sharply in 2021 to counter excessive inflation. These strikes drastically harm fairness markets in 2021 however put Brazil a lot additional forward within the financial cycle than most nations. Brazil has been a top-performing fairness market this 12 months (as of November

2022). We anticipate Brazil to be one of many first nations globally to start a rate-cutting cycle, maybe early in 2023. As soon as this occurs, we anticipate traders to take a constructive view of ahead progress, company fundamentals to enhance, and valuations to rise.

Indonesia: Indonesia has a sexy mixture of sturdy gross home product (GDP) progress, average inflation, and gently rising rates of interest mixed with a powerful demographic profile and an rising center class. We imagine this supplies an extended runway for secular progress. Indonesia can be a beneficiary of commodity-price will increase and a reform-minded authorities. In our view, company fundamentals are predominantly good and valuations seem cheap, and the economic system continues to be on a powerful progress trajectory. We’re obese Indonesia, significantly financials.

Saudi Arabia: Saudi Arabia now represents greater than 4% of the MSCI EM Index. It has in some methods crammed the hole that Russia left when it was faraway from the index after invading Ukraine. Saudi Arabia’s market is energetic with quite a few preliminary public choices (IPOs) and a plethora of firms benefiting from sturdy oil costs and the transformation of the nation’s economic system. The economic system is evolving quickly; girls are more and more within the workforce, extra social occasions are allowed, and tourism is inspired.

Wealthy and Rising Alternative Set for High quality Development Buyers

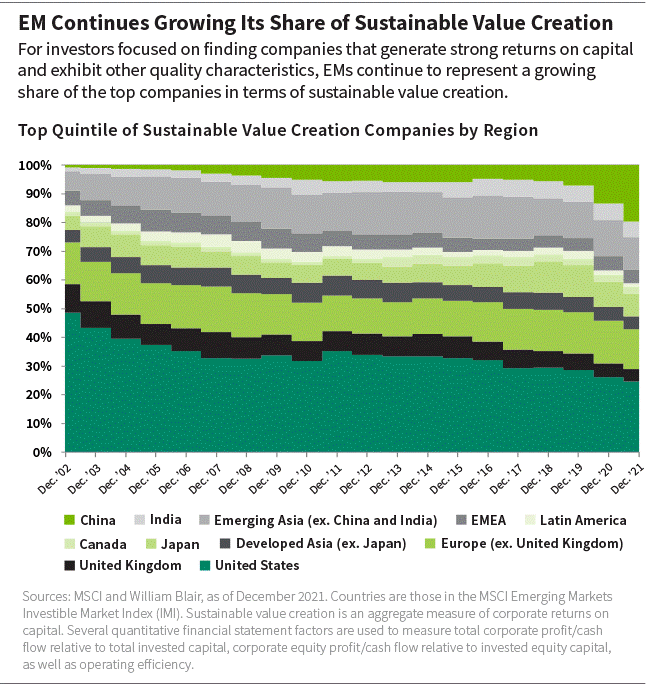

EM firms punch effectively above their weight globally with regard to sustainable worth creation, as measured by return on capital employed. As of December 2021, EMs represented barely greater than 10% of the MSCI ACWI IMI by market cap however accounted for about 40% of the worldwide prime quintile of high quality progress firms as outlined by sustainable worth creation, up from about 15% in 2002. In contrast, america represented about 60% of the index however lower than roughly 30% of the highest worth quintile.

Many of those high quality progress firms are in China and India, which have rising per-capita earnings, a elementary driver of sustainable worth creation. Alternatives to search out high quality in these nations are plentiful. For instance, about 40% of China A-share firms—greater than 1,200 firms in whole—exhibit larger high quality, primarily based on return on fairness (ROE), than the common of the broader EM universe. In India, 20% of firms have larger ROE than the EM common, which represents round 400 firms.

Sectors to Watch

We determine two particular sector alternatives going into 2023 and past:

Know-how: We imagine the semiconductor business is within the midst of a cyclical slowdown, however the long-term, secular progress story stays very engaging. Whereas we’ve got tactically decreased our expertise {hardware} publicity, we are going to look to extend positions as alternatives come up in 2023.

Healthcare: Healthcare expenditure in creating nations ties into the expansion dynamic of an rising center class. Healthcare spending in EM nations is effectively under developed nation averages, each per capita and as a share of GDP. We imagine that is one other secular progress path that may monitor earnings progress, and we’re positioning ourselves accordingly.

Inexperienced Economic system

We imagine the world’s transition to a low-carbon economic system gives sturdy progress alternatives for years to come back. Reducing value curves, growing innovation, and coverage/societal assist are among the components boosting adoption and progress.

Many EM firms are effectively positioned for this transition; some are even world leaders within the house, particularly in photo voltaic and electrical car (EV) batteries.

We imagine progress momentum and investments might speed up within the coming years because the world seeks to succeed in net-zero targets. We’ve got elevated publicity to renewable power and power storage and their provide chains throughout our portfolios.

Remaining Take

The EM bear market is lengthy within the tooth by way of time, value, and multiples. Earnings expectations have already been reduce, and plenty of EMs are effectively forward of developed markets in financial tightening. EMs could possibly be a brilliant spot in a cloudy image for equities globally in 2023.

The MSCI ACWI IMI captures large-, mid-, and small-cap illustration throughout 23 developed markets. The MSCI EM Index captures large- and mid-cap illustration throughout 27 EMs. The MSCI EM IMI captures large-, mid- and small-cap illustration throughout 27 EMs. The S&P 500 Index tracks the efficiency of 500 massive firms listed on inventory exchanges in america. The STOXX Europe 600, additionally known as STOXX 600, tracks the efficiency of European shares. Index efficiency is offered for illustrative functions solely. Indices are unmanaged and don’t incur charges or bills. A direct funding in an unmanaged index shouldn’t be potential.

Authentic Put up

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.

{kind=link}