JHVEPhoto/iStock Editorial through Getty Pictures

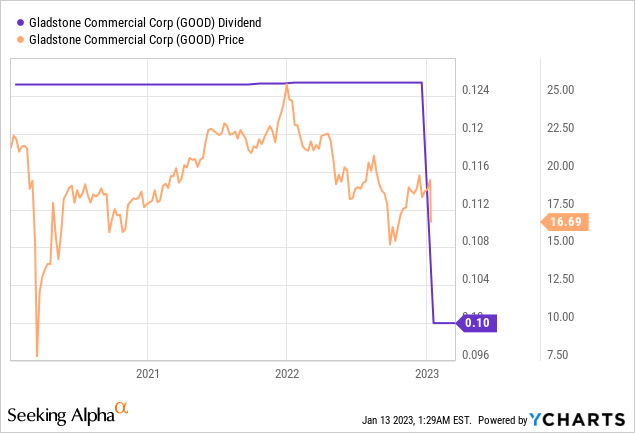

Gladstone Business (NASDAQ:GOOD) welcomed its shareholders into the brand new yr with a dividend reduce. The REIT just lately declared a month-to-month per share money dividend payout of $0.10, a 20.3% lower from the prior payout, which types an annualized yield of seven.2% in opposition to the present share value. The $670 million McLean, Virginia-based REIT which began buying and selling near the flip of the millennium has fairly actually saved its dividend on an upward trajectory since 2003. The month-to-month payout was maintained in the course of the 2020 flash pandemic crash, was elevated in the course of the 2008 monetary disaster, and had been maintained at its prior payout of $0.13 per share since January 18, 2008. The no reduce since inception mantra was a defining a part of administration’s pitch of Gladstone Business, therefore, the sudden reduce to kick begin the brand new yr undoubtedly got here as a shock to some shareholders.

What occurred? Administration billed the transfer as a precautionary pivot forward of anticipated financial headwinds and broader volatility this yr. The financial forecasts for 2023 are certainly grim, with the US broadly anticipated to fall right into a recession in opposition to rates of interest which can be nonetheless being hiked to new highs and inflation nonetheless far forward of the Fed’s 2% goal.

Nonetheless, the dividend reduce represents a watershed second in Gladstone’s twenty-year historical past as a publicly traded REIT. That administration had carried out such a tough pivot in opposition to a defining function of their investability, a recurring theme of their earnings name, and a probable driver of the comparatively sturdy returns of the externally managed REIT represents some extent of no return, symbolically akin to Caeser’s crossing of the Rubicon river for my part.

A New Method Ahead

With the REIT’s funding advisor waiving incentive charges for the primary half of 2023, administration acknowledged that they anticipate this to mixture with the dividend reduce to enhance the general liquidity place of their stability sheet. The REIT held whole debt of $747.2 million as of the top of its final reported fiscal 2022 third quarter and positioned the REIT’s debt-to-capital ratio at 65.84%, practically 35% larger than its peer group’s median debt-to-capital ratio of 48.85%. This was additionally seemingly a consideration within the dividend reduce as with the Fed set to hike charges to between 5% and 5.25% this yr, the best fee in 17 years, its debt place would have come below some strain.

While quarterly curiosity bills have been rising and reached $9.1 million in the course of the third quarter, its highest stage in over ten incomes quarters, the majority of the REIT’s debt profile needs to be much less delicate to future rate of interest hikes. Round 49.5% of their debt is at a set fee, one other 49.5% is floating fee debt hedged by a mixture of rate of interest swaps and rate of interest caps, and the remaining 1% is at a floating fee. Additional, as of the top of the quarter, their efficient common SOFR was 2.98% with solely $66.1 million in mortgage maturities coming due in 2023. The REIT has additionally been leaning on secondary choices and raised $8.9 million within the third quarter internet of prices by its at-the-market providing program. That is nonetheless operating with the corporate holding the view to utilizing proceeds to opportunistically purchase again their preferreds.

The only-tenant REIT which owns roughly 17.2 million sq. toes of business and workplace actual property throughout 137 properties within the US final reported occupancy of 96.9% and $1.61 in adjusted FFO per share. Tenants which embody Citrix Programs got here with a median remaining lease time period of seven.1 years.

The Sequence E Preferreds In opposition to Commons Volatility

Gladstone Business 6.625% Sequence E Cumulative Redeemable Most popular Inventory (NASDAQ:GOODN) supply one other option to acquire publicity to the REIT’s portfolio. The worth proposition of Sequence E preferreds facilities on the $1.66 annual coupon paid in month-to-month instalments. This presently works out to be a 7.3% yield with the preferreds presently buying and selling at $22.75 per share.

Not solely is that this on par with the dividend on the commons, however the preferreds are additionally buying and selling round $2.25 decrease than their redemption worth. This close to 10% low cost to its par worth opens up the additional scope of capital appreciation because the commons get rerated on the again of the dividend reduce.

QuantumOnline

Gladstone Business just lately introduced its intention to purchase again at the least $20 million price of the Sequence E preferreds, round one-third of the overall quantity issued. It is a bittersweet occasion. On one hand, it helps shut the low cost to par and advantages the present homeowners of the preferreds with the scope of additional repurchases on the open market at a reduction to par lowering the opportunity of materials draw back.

To be clear, the preferreds as much less more likely to considerably deviate from their redemption value in opposition to financial disruption if the REIT has signaled an intention to purchase them again on the open market forward of its October 4, 2024 maturity date. Bears would nonetheless level to this transfer being created by a potential lack of funding alternatives above their price of capital. I am impartial on Gladstone Business after the reduce. The preferreds needs to be thought-about by extra risk-averse revenue traders.

{kind=link}