Michael Vi

Yesterday, after the market shut, LendingClub Company (NYSE:LC) issued a press launch asserting its plan to streamline its operations. This features a discount of its workforce by 14%. The rationale for the announcement was offered under:

…a price discount and reorganization plan to align its operations to decreased market income following the Federal Reserve’s historic tempo of rate of interest will increase.

The corporate additionally launched preliminary outcomes for This autumn 2022 and scheduled the total earnings launch and convention name for the twenty fifth of January after the market shut.

There may be a lot to unpack and for traders to digest. I’ll endeavor to supply insights as to the influence and what this all means for traders.

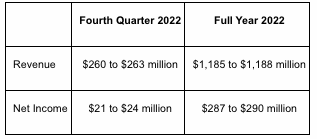

The This autumn Earnings

The preliminary outcomes are proven under:

LC Investor Relations

On the face of it, the 4th quarter income is within the center vary of steering ($255 to $265 million) offered within the Q3 earnings name, whereas the online earnings is within the excessive vary of steering ($15 to $25 million). Originations had been additionally on the lights aspect (at $2.5 billion solely) in comparison with $3.5 billion the earlier quarter.

Nevertheless, there have been additionally quite a few changes and one-off gadgets to contemplate together with:

– the acquisition of the $1.05 billion MUFG portfolio that closed on the 2nd of December 2022. As such, LC benefited from virtually one month of curiosity (my estimate is an incremental pre-tax earnings of ~8m), however there would have been some transaction prices concerned as properly. – restructuring price of $4.4 million in This autumn referring to the cost-cutting.

If I modify for these, it appears like LC’s earnings would have come on the decrease finish of income and web earnings steering. Provided that LC sometimes sandbags earnings steering, this means to me that LC is going through stronger-than-expected headwinds in terms of its market income.

To recap, as I highlighted in my earlier article, traders’ urge for food for unsecured lending is waning for 2 causes. Firstly, the quickly larger rates of interest are altering the economics and return traders are in a position to generate from the asset class, provided that funding prices change instantly because the Fed raises charges (for some traders) whereas the rise in yield of the loans reprices with a major lag.

The second motive is the worry of a looming Fed-induced recession. Buyers are naturally taking a extra cautious stance in terms of high-yield private shopper lending.

That is clearly impacting LC’s market revenues and origination ranges. And this headwind is prone to proceed and maybe even strengthen within the subsequent few quarters.

The Focus On Profitability

LC administration is targeted on rising its mortgage portfolio. That is the important thing strategic crucial and is driving robust working leverage for the enterprise.

This was defined in nice element in my newest article on LC.

Nevertheless, to develop its ebook, LC should generate natural capital, and, due to this fact, GAAP profitability is a key enabler.

Subsequently, I used to be not stunned that LC introduced a cost-cutting train given the headwinds within the market. LC should stay worthwhile to develop and generate natural capital in any other case, will probably be capital-constrained. This implies pulling all levers out there together with huge price cuts.

I anticipate LC to exit 2022 with ~$5 billion of unsecured private lending which ought to ship a steadily rising earnings stream at a excessive yield. Fortuitously, LC has already totally reserved for many of those loans underneath the CECL lifetime anticipated loss methodology. In 2023, I anticipate LC to proceed to lean into retaining extra loans on its stability sheet versus promoting these within the market. I additionally anticipate it to cut back its advertising spend additional and largely concentrate on servicing current LC members. Moreover, administration of credit score threat will come to the forefront, particularly if a recession ensues throughout 2023.

Closing Ideas

Mr. Market reacted properly to the press launch in after-hours buying and selling with the refill 4%. Let’s examine if Mr. Market hasn’t modified his thoughts throughout Friday’s buying and selling session.

The complete earnings launch on the twenty fifth of January will likely be necessary, particularly, the 2023 full-year steering which I anticipate to err on the conservative aspect given macro uncertainties.

LC, nonetheless, ought to profit from a gradual curiosity earnings stream from its massive portfolio to cushion the headwinds. I’d additionally keenly look out for its capital ratio (particularly the Tier 1 leverage ratio) to evaluate how a lot incremental mortgage capability it’s prone to have in 2023. The MUFC acquisition would make the most of ~$110 million of capital, however given the brief period of the portfolio (<1 12 months), that capital needs to be launched quickly all through 2023.

There are presently robust headwinds (charges, recession fears, traders’ urge for food) within the private lending house however the long-term narrative is totally intact. LC ought to stay worthwhile all through 2023 and because it continues to construct its unsecured lending portfolio, that profitability will improve materially within the coming years. {The marketplace} ought to start to get better when the Fed pauses and peak recession fears cross.

In a traditional economic system, with an unsecured portfolio of say ~$10 billion, LC ought to have the ability to generate pre-tax earnings of ~$1 billion. That is the chance forward. I stay very bullish about LendingClub Company.

{kind=link}