rarrarorro/iStock by way of Getty Photos

Co-produced with Treading Softly.

It has been mentioned that the USA has been the one biggest incubator of wealth within the historical past of mankind. The USA’ financial output and development have been distinctive in a world and historic context.

A key driver of this has been what’s tied up within the American Dream – the assumption that any particular person can higher their scenario and circumstances via diligence and onerous work.

Whereas the federal government has slowly taken extra of a task and affect within the general market and financial system, an indicator of the USA has been the assumption and assist of an open market the place anybody can take part.

Greed is a robust motivator and drive. The need to higher one’s scenario is a robust driving drive, and when an financial construction is designed to assist assist and flourish this driving drive, the financial system will profit.

So in terms of my retirement, I do not wager in opposition to the USA – I wager on it. The inventory market has turn into an more and more accessible possibility for these with capital to spend money on the US financial system. That is the place I select to take a position the majority of my internet price.

Typically buyers consider the mega-cap firms that dominate the funding information cycle, like Tesla, Inc. (TSLA), Microsoft Company (MSFT), and even Starbucks Company (SBUX). But the majority of the financial system is supported by a lot smaller firms.

I prefer to spend money on firms and funds that actively allow financial exercise by supporting the center market of the financial system. This part of the financial system is the most important however most disregarded space out there. I do that by being a lender to a big selection of firms and people, and in return, I get curiosity and dividends paid again to me.

Let’s take a look at two methods you are able to do that with me.

Decide #1: BRSP – Yield 11.1%

BrightSpire Capital, Inc. (BRSP) is a industrial mortgage actual property funding belief (“REIT”) which invests primarily in floating-rate senior mortgages. With the Federal Reserve mountaineering charges extra often than a university pupil orders pizza, an investor would possibly assume that may be an excellent tailwind for BRSP’s earnings.

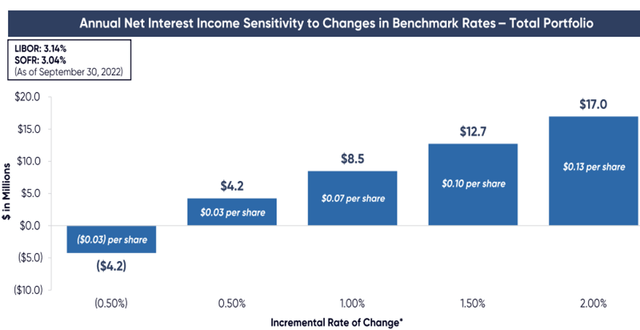

That thought can be proper, and here’s a have a look at BRSP’s rate of interest sensitivity:

BRSP Q3 2022 Complement

Notice that since September thirtieth, 1-month LIBOR is as much as 4.4%, so for the needs of this desk, charges are up roughly 1.2%. So rate of interest actions alone needs to be contributing a $0.08-$0.09 optimistic tailwind to BRSP’s annual earnings.

Regardless of that tailwind, BRSP has seen its share value decline. BRSP is at the moment buying and selling at almost a 50% low cost to ebook worth. It’s buying and selling at its lowest value since 2020, when it wasn’t paying a dividend in any respect.

In our opinion, this valuation is totally unjustified. Nonetheless, there are some authentic headwinds that some buyers may be fearful about. Let’s take a look at what may be regarding buyers:

Mortgage originations are slowing down: In Q3, BRSP originated solely $91 million. It is a sharp decline from $896 million within the first half. Administration urged origination will stay low in This autumn and possibly even the primary half of 2023. It is a headwind to earnings as a result of, as loans repay, the dimensions of the mortgage portfolio will decline. A smaller mortgage portfolio means much less curiosity is collected. All issues being equal, this can be a headwind to earnings.

Administration was upfront with the dangers they see within the Fed going too far and inflicting a recession. In consequence, BRSP is taking a extra conservative strategy than some friends. They’re selecting to construct up liquidity, as an alternative of creating loans in what would possibly prove an unfavorable setting. Within the earnings name, CEO Mike Mazzei mentioned:

Lastly, that can undoubtedly be nice lending alternatives that can come up from this market dislocation. However to be clear, over these previous few quarters and within the very speedy future, all issues equal, our bias is that liquidity will typically take precedent over new mortgage originations and inventory buybacks.

Offsetting the decline in originations is a decline in repayments. Within the earnings name, BRSP additionally famous a rise in mortgage modifications and extensions growing the length of the loans of their portfolio. BRSP collects further charges for making these modifications, and likewise will gather extra curiosity for longer.

The worth of all debt is declining: Business mREITs measure the worth of their loans by par worth minus CECL (present anticipated credit score loss). These loans are usually not publicly traded, and due to this fact are usually not “marked to market” just like the debt held by bond funds or different sorts of mREITs like company mREITs. This may make a cloth distinction in ebook worth.

Take into account Annaly Capital Administration, Inc. (NLY). It has $67.3 billion in par worth of company MBS that’s mirrored in ebook worth at its honest worth of $62.7 billion as a result of these belongings are mark-to-market and there’s a public market the place they’re at the moment buying and selling at a reduction to par.

NLY Q3 2022 Complement

If these belongings had been carried at par worth minus CECL – which is $0 since these MBS don’t have any credit score threat – that may enhance NLY’s ebook worth by $4.59 billion. NLY’s ebook worth would have reported $10.67/share increased in Q3 if company MBS was accounted for utilizing the identical methodology that industrial mREITs use for his or her mortgages.

So, once we talk about the premium/low cost to ebook worth for industrial mREITs, we should always needless to say the ebook worth solely displays credit score threat as calculated by CECL. It doesn’t mirror the market modifications within the value of debt normally, which in 2022 has been important. U.S. Treasuries, company MBS, leverage loans, and bonds of all stripes have seen costs decline in 2022. So, it is sensible that these loans are buying and selling at decrease costs when buyers are shopping for the businesses as a result of the marketplace for mREIT shares is the one open market the place these mortgages commerce.

After we have a look at a number of the largest, most established mREITs within the industrial sector like Blackstone Mortgage Belief (BXMT) or Starwood Property Belief (STWD), they’re buying and selling at 15-20% reductions to ebook worth. So that’s the quantity we might chalk up as an affordable low cost as a result of modifications in mortgage valuations.

Default issues: Final quarter, BRSP did acknowledge an impairment on two loans of $57 million ($0.44/share). Solely one of many loans defaulted, however each are to the identical borrower and BRSP thought it prudent to imagine each would default. The quantity written off displays the distinction between the dimensions of the loans and an appraisal of the liquidation worth of the property. With a big write-off final quarter, some buyers may be involved in regards to the credit score high quality of BRSP’s portfolio.

We aren’t. Why? These loans originated in 2019, lengthy earlier than the present administration took over. They had been additionally rated “4” (underperforming) on BRSP’s ranking scale since 2020, so the danger of those explicit loans was recognized and telegraphed by administration. Credit score defaults occur, that could be a actuality of investing. At present, all of BRSP’s holdings which might be rated 4 originated previous to 2020 underneath prior administration. BRSP has managed to roll over most of its portfolio with a modest affect on its ebook worth. The loans originated over the previous two years mirror the way more conservative strategy of present administration in comparison with the prior regime. The remaining legacy holdings would possibly justify some low cost to ebook worth, however the present valuation is extreme.

Valuation: As famous above, we do see some explanation why BRSP needs to be buying and selling at a reduction to ebook worth. Slowing originations will probably be a headwind to earnings, although it needs to be offset by the advantage of rising charges. BRSP’s dividend may be very conservative at $0.20/quarter in comparison with $0.25/share in distributable earnings. This protection ensures the dividend needs to be safe even when the headwinds outweigh the tailwinds.

The worth of debt is declining, and this probably ought to contribute to a 15-20% low cost merely as a result of macro-environment the place different debt funding choices can be found for decrease costs.

Lastly, the write-offs final quarter served as a reminder to buyers that defaults occur. A number of the weaker legacy loans in BRSP’s portfolio might expertise an identical destiny.

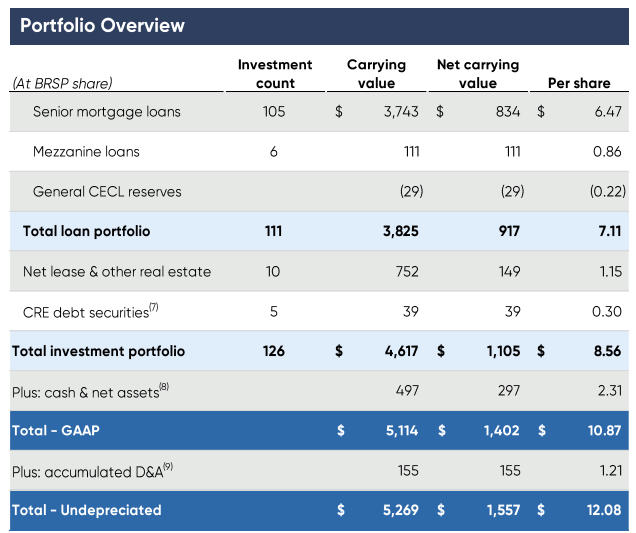

So BRSP ought to commerce at a reduction to ebook worth, however how a lot? Here’s a have a look at how BRSP’s ebook worth is at the moment calculated.

Q3 2022 Complement

$2.31 is money and internet belongings, and $2.36 is its internet lease properties and related depreciation (which suggests a 7% cap fee on the $64 million annualized NOI). That’s $4.67/share in NAV earlier than you even speak in regards to the mortgage portfolio. If we assume that BRSP’s loans ought to commerce at a couple of 20% low cost, that may suggest the mortgage portfolio is price roughly $5.64/share in at present’s setting. This suggests that BRSP’s “honest worth” needs to be roughly $10.31.

Immediately’s share value permits for an enormous margin of security for defaults. Moreover, BRSP’s present dividend is among the many finest coated within the sector, with 125% protection final quarter. It seems that the market continues to be pricing within the “Colony” penalty, penalizing the share value for the sins of prior administration. Nonetheless, administration has modified, and the model may be very completely different. The place Colony reached for yield and loaded up the portfolio with mezzanine and shaky development loans, BRSP’s administration has been relentlessly centered on high-quality senior mortgages.

When the market setting turned unfavorable, BRSP did not preserve accelerating. It took the conservative route, backing off and increase liquidity – making certain that it has a robust and liquid monetary place to cope with any headwinds.

BRSP is a really completely different firm from its predecessor. Administration is way more conservative and the portfolio is far increased high quality. The market hasn’t realized it but, and we’re comfortable to gather our 11% yield whereas we wait.

Decide #2: ECC – Yield 15.8%

Eagle Level Credit score Firm Inc. (ECC) is a closed-end fund (“CEF”) that invests within the specialised sector of CLOs or Collateralized Mortgage Obligations. Particularly, ECC has most of its funding within the “fairness” tranche.

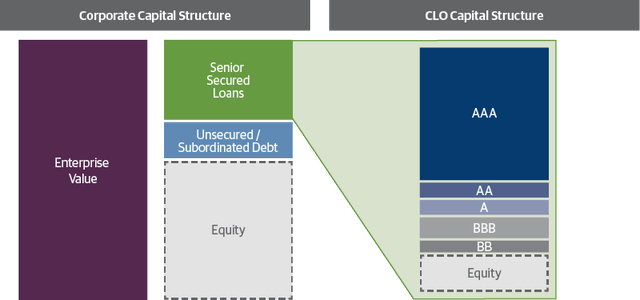

CLOs spend money on Senior Secured Loans. These are probably the most senior loans in an organization’s capital construction and have a secured first lien curiosity. This places the CLO on the very prime of the capital construction of the debtors.

What appears to confuse many is that the CLO has its personal capital construction. The CLO itself borrows cash, utilizing the loans as collateral. These borrowings are known as “debt tranches,” and the CLO agrees to pay out the proceeds to the debt tranches in precedence order. It seems one thing like this. Supply.

Guggenheim Investments

Notice there are two distinct capital constructions. On the left, you will have the borrower that sometimes has senior secured loans, possibly some unsecured bonds or subordinated debt, and fairness (most popular and customary).

On the suitable, you will have the CLO. The CLO invests within the highest stage of the capital construction of the company however has its personal capital construction which consists of a number of tranches from AAA to BB. Similar to another firm, the CLO is required to pay all of the debt it owes earlier than the fairness buyers gather their income. ECC primarily buys the fairness tranches of CLOs.

These are fairness positions in a portfolio of senior secured loans. Type of like if you spend money on a enterprise growth firm’s (“BDC’s”) frequent inventory, the BDC has a portfolio of loans that your fairness is shopping for, however the BDC itself has debt that must be repaid.

These fairness positions are usually not publicly traded. In consequence, they’re illiquid investments which might be finest held till maturity. CLOs have a predetermined lifespan, sometimes 7-10 years. After elevating capital, a CLO can have a “reinvestment interval” the place any principal repayments from the debtors are reinvested into new loans. Then on the finish of the CLO’s life, the CLO can have an “amortization interval” the place all principal repayments/prepayments are used to pay down the debt so as of seniority and as soon as all of the debt is repaid, the fairness buyers get the steadiness.

Notice that through the reinvestment interval, the CLO is being paid again with par {dollars}. If an organization decides to refinance or deleverage by paying off a mortgage, the CLO receives par after which reinvests in loans on the present market value. So when loans are buying and selling under par, it is rather advantageous for CLOs which might be of their reinvestment interval.

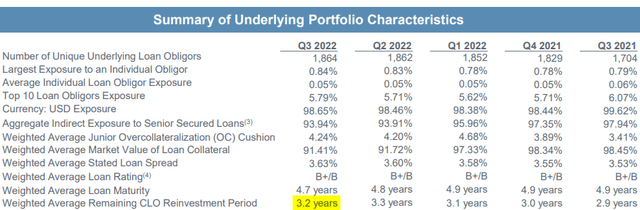

These are the sorts of CLOs that ECC has been centered on. ECC has deliberately elevated the common remaining CLO reinvestment interval in its portfolio to three.2 years. Supply.

ECC Q3 2022 Presentation

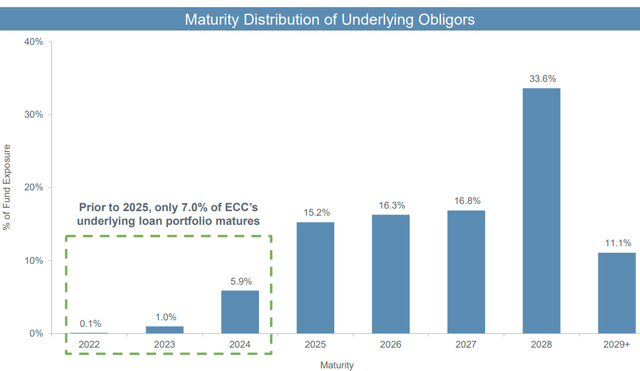

Moreover, the underlying loans that the CLOs maintain have only a few maturities within the subsequent two years.

ECC Q3 2022 Presentation

It is a profit as a result of defaults are usually most frequent when loans mature. With the financial system prone to weaken in 2023, ECC has little or no publicity to firms that will probably be pressured to refinance when there are twin headwinds of high-interest charges and a weakening financial system. If there’s a recession in 2023, it is best to not maintain a number of loans which might be maturing mid-recession.

It’s this sort of proactiveness from ECC’s administration that offers us the arrogance to proceed holding and gathering the large +15% yield.

Dreamstime

Conclusion

With BRSP and ECC, we cannot solely be actively engaged in the USA financial system, however we may also be key gamers in serving to or not it’s sturdy and wholesome.

A recession is coming, as a recession is at all times coming. It’s a query of “when,” not “if.” This doesn’t suggest you need to pull out of the market or financial system and look ahead to higher instances to return. It is a time when the level-headed can stay invested and unlock large rewards. ECC and BRSP have positioned themselves to learn from the present rate of interest setting and created portfolios structured to climate any recessionary storms to return.

I really like the USA of America. No nation is ideal. No nation has ever been with out error or fault. Likewise, no particular person is ideal or with out fault. Nonetheless, I’m betting my retirement on the flexibility of the USA financial system to proceed to supply wealth for its folks and permit those that try to higher themselves to realize these targets.

It is by no means simple to realize success, however it stays attainable. I prefer to assume that I will help allow that for others, all whereas receiving wonderful revenue for myself.

That is the great thing about the Revenue Methodology. That is the great thing about revenue investing.

{kind=link}