Leland Bobbe/DigitalVision by way of Getty Photos

Shares of Gaming & Leisure Properties (NASDAQ:GLPI) massively outperformed the broader REIT index/ETF (VNQ) over the previous yr with a complete return of 27% versus -17% for VNQ. In a turbulent macro setting, Gaming & Leisure has benefitted from contractually assured money flows below its triple web lease construction.

Whereas I anticipate GLPI will proceed to obtain well timed funds from its on line casino operator tenants, GLPI trades on the excessive finish of its historic valuation vary. That is in distinction to different sub-sectors of the REIT market (akin to residences, places of work, and many others) that are buying and selling on the low finish of their historic valuation vary.

Resilient Money Circulation- Even in Downturns

GLPI has benefitted from the sturdiness of its contractually assured rental stream from regional casinos. GLPI has lengthy (15-40 yr leases) with sturdy on line casino operators together with PENN Leisure (PENN), Bally’s (BALY), Ceasars (CZR) and Boyd (BYD). At the moment all of those firms seem like in respectable monetary form. In fact casinos have a historical past of stepping into bother which is why GLPI makes use of grasp leases (described beneath).

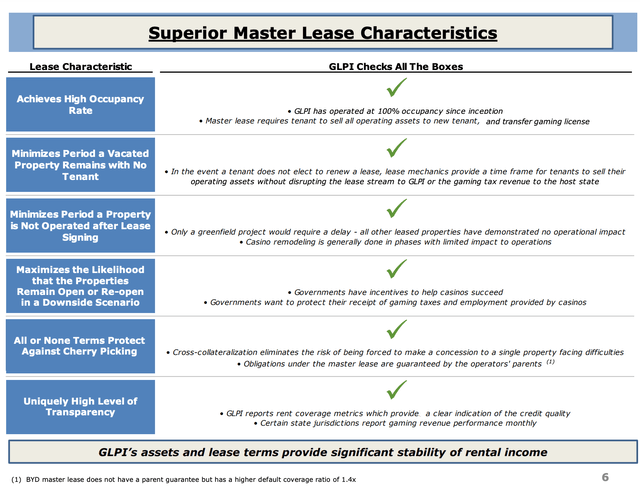

As proven beneath, GLPI’s leases are structured to make sure tenants make funds even when the tenant results in chapter. The grasp lease construction requires that tenants make good on lease funds on all properties. From the owner’s perspective, the aim of a grasp lease is successfully to forestall the tenant from getting the leases on underperforming properties rejected in chapter court docket.

Gaming & Leisure Grasp Leases (Investor Presentation)

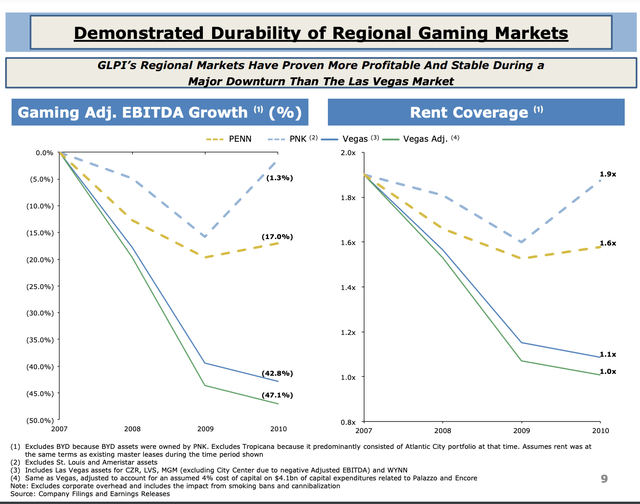

It is usually price noting that regional gaming properties (versus properties on the Vegas strip) have proven to be extra resilient throughout financial downturns. The rationale for that is that comparatively cheap native journeys have a tendency to stay in family budgets (whereas costlier vacation spot journeys like Vegas could get lower). As well as Vegas properties are extra depending on company trade-shows and junkets (team-building) occasions. Lastly, whereas new on line casino resorts (or re-developed on line casino resorts) pop up in Vegas (growing competitors), regional casinos are usually native monopolies.

Resilience in Previous Downturns (Investor Presentation)

Progress – Natural Vs. Exterior

The triple web lease construction makes estimating natural development pretty easy for GLPI. Most of GLPI’s leases are topic to mounted escalators between 1.5-2.0%. Whereas a few of GLPI’s leases are linked to CPI, all of those leases have slender caps and flooring which successfully repair lease development in a slender band of 0-2% yearly.

Exterior development comes from buying properties from on line casino operators. When GLPI is ready to add properties of comparable or higher high quality to its current portfolio (and with comparable or greater annual lease escalators) at greater cap charges than the implied cap price at which GLPI trades, it’s accretive to GLPI’s NAV (web asset worth) per share. Equally the acquisition of properties at decrease AFFO multiples (greater cap charges) than its personal a number of shall be accretive to AFFO per share.

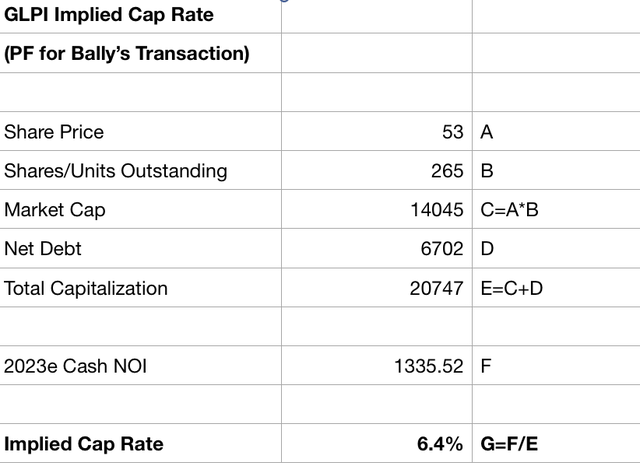

Over the previous couple years GLPI has acquired practically $2 billion price of properties at cap charges starting from 6.9-7.6%. Whereas as we speak GLPI trades at an implied cap price of 6.4% (proven beneath) and 14.5x AFFO/a number of, on the time GLPI made these acquisitions (and issued shares/items), GLPI traded at the next implied cap price (7+%) and decrease a number of of AFFO. As such, the worth accretion to shareholders from these transactions seems to have been pretty minimal.

Given how nicely, GLPI’s shares have carried out over the previous yr, the corporate now trades at only a 6.4% implied cap price. To the extent that GLPI is ready to purchase properties (once more of comparable/higher high quality with equal or higher lease escalation phrases) at 7%+ cap charges, it is going to be in a position to create worth for shareholders by exterior development.

One disadvantage right here is that its important competitor Vici Properties (VICI) can also be buying and selling at a premium valuation (and is in search of exterior development) which implies that GLPI is prone to face stiff competitors to buy belongings. That is in distinction to different actual property sub-sectors the place competitors has decreased as the price of capital has risen (share costs have fallen).

All-in, I anticipate tepid (3-4%) AFFO development for GLPI over the medium time period.

Valuation

At $53/share Gaming & Leisure seems absolutely valued at 14.7x 2023e FFO, a 5.3% dividend yield, and an implied cap price of 6.4% as proven beneath.

GLPI Implied Cap Charge (Firm Filings; Creator Estimates)

My cap price calculation takes under consideration the newest acquisition of properties from Bally’s (BALY) by together with the NOI (and including to debt – although we might even see GLPI fund extra of this deal by way of an fairness issuance).

The 6.4% implied cap price at which GLPI trades is on the low finish (excessive valuation) of the place the inventory has traded since coming public in late 2013 (vary of 6.3% to eight.2%). GLPI trades at a 15% or so premium to NAV (utilizing a 7% cap price which could possibly be thought-about optimistic). That is in sharp distinction to different sub-sectors like residences and places of work that are buying and selling at deep reductions to NAV and providing cap charges on the excessive finish of their historic vary (low valuation).

Conclusion

Gaming & Leisure has been a incredible performer over the previous yr. Whereas GLPI ought to produce constant working outcomes and dividends, shares commerce at a excessive valuation relative to historical past whereas reductions abound all through the REIT universe. As such, I see GLPI as being comparatively unattractive at $53 per share. I see a lot better worth within the closely discounted condo and workplace REITs I’ve not too long ago written about right here on In search of Alpha.

{kind=link}