Thanks on your assistant/iStock through Getty Photographs

Thesis

DNP Choose Earnings Fund (NYSE:DNP) is a closed-end administration funding firm that first supplied its frequent inventory in 1987. The fund’s major funding aims are present earnings and long-term progress of earnings. DNP seeks to attain its aims by investing primarily in a diversified portfolio of fairness and stuck earnings securities of firms within the public utilities trade.

DNP is a golden normal of the Utilities CEF buildings. Utilities are a defensive asset class, and so they have seen an enormous influx of capital as traders have began to cost in a recession. Huge inflows into an asset class not matched by an equal transfer up in elementary efficiency, find yourself inflating the numerator of the ‘P/E’ ratio:

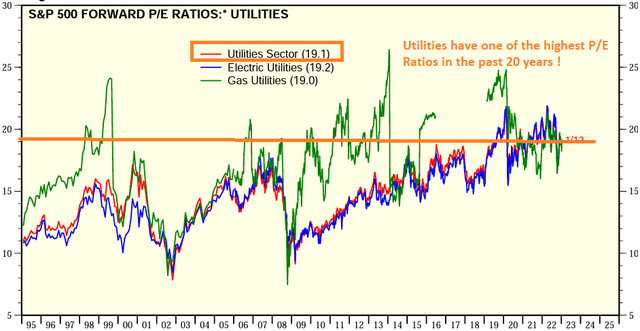

Utilities P/E Ratios (Yardeni Analysis)

As we will see from the graph above, courtesy of Yardeni, the Utilities sector shows one of many highest P/E ratio noticed prior to now 20 years. Why is that this the case? As a result of it’s a defensive sector:

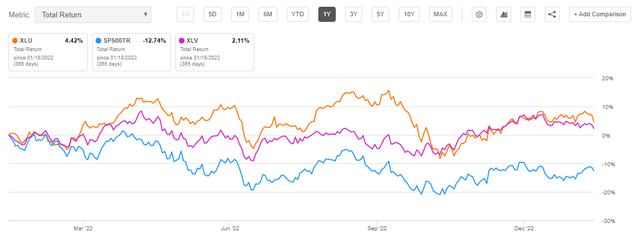

1-12 months Whole Return (Searching for Alpha)

We are able to see within the above whole return graph that the Utilities Choose Sector SPDR ETF (XLU) and the Well being Care Choose Sector SPDR Fund (XLV) had very shallow drawdowns in 2022 because the S&P 500 cratered. The explanation for this efficiency is the crowding-out commerce. In contrast to retail traders, many massive asset managers have outlined, most money buckets which normally are usually within the 5% to 10% vary. That signifies that a big fund can not maintain money greater than these ranges, which interprets into the fund managers transferring into defensive shares/sectors once they consider a recession is across the nook. As retail traders we’ve the posh of sitting 100% in money if we select to take action, whereas massive asset managers must in some way justify their charges, thus at all times stay invested within the equities markets to a sure extent.

We are able to see how DNP’s whole return carefully mirrors what we noticed in XLU:

DNP vs XLU (Searching for Alpha)

DNP is a structural transformation of Utilities fairness publicity into month-to-month dividends. The CEF construction although has its pitfalls as effectively, particularly the premium/low cost to NAV. When traders love a CEF an excessive amount of, they have a tendency to bid it up considerably, however not like an ETF which simply points extra shares, a CEF simply finally ends up having a big premium to NAV. So you could have a little bit of a double whammy right here – an enormous, unsustainable premium to NAV for DNP (which we talk about intimately within the beneath ‘Premium / Low cost to NAV’ part), and a historic excessive P/E ratio for the underlying asset class, particularly Utilities.

Premium / Low cost to NAV

DNP is a type of uncommon, golden normal CEFs which have at all times traded at premiums prior to now decade:

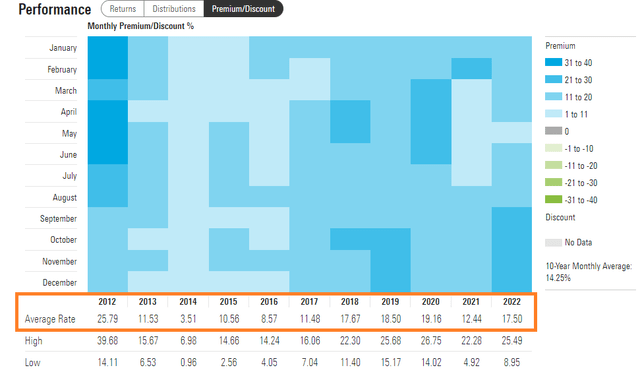

Premium/Low cost to NAV (Morningstar)

The above desk, courtesy of Morningstar, presents the month-to-month premiums/reductions for DNP prior to now decade. Blue is indicative of a premium to NAV, whereas inexperienced reveals months when the CEF was buying and selling at a reduction. We are able to solely see blue within the desk above, signifying a voracious investor urge for food for this identify.

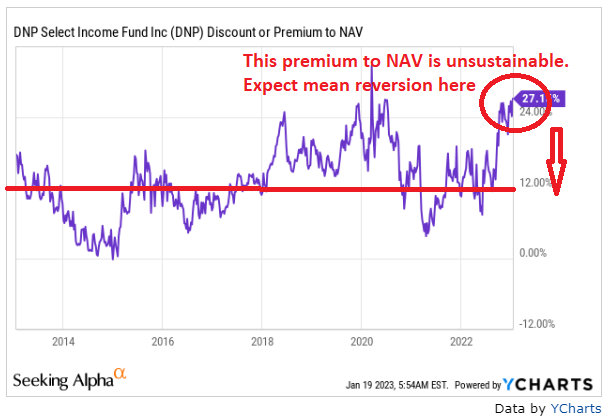

The orange field we’ve drawn above reveals the common premium exhibited by the fund, by calendar yr. Exterior 2012, we will see the CEF having a median premium of 15% to 17%. Furthermore, if we take a look at the following row, once more outdoors 2012, the fund by no means exhibited a premium increased than 26.75%, achieved in 2020. Which brings us to at present’s premium stage, which is presently 27.15%:

DNP Premium to NAV (YCharts)

At present’s premium stage is principally the second largest prior to now decade. Is it sustainable? No. Merely put, the CEF’s shares commerce at a premium of 27.15% to the precise NAV of the fund. If DNP have been to liquidate at present, traders would lose 27.15% proper now. Framing the premium from this angle ought to give a retail investor a greater understanding of the magnitude of this dislocation (for avoidance of doubt, there may be 0% probability of a fund liquidation; nonetheless, the crux of a CEF construction is the premise between NAV and share worth).

Conclusion

DNP is a 6.7% yielding CEF. The fund transforms Utilities equities returns into month-to-month dividends. The car is a golden normal within the CEF area, having a particularly sturdy historic efficiency and lengthy tenure. Buyers have acknowledged the long run worth within the CEF by bidding it up prior to now decade. Previously ten years the CEF has spent its time at a market worth above its internet asset worth. On common, when measured month-to-month, the premium to NAV has been round 15%. At present DNP is buying and selling at a particularly excessive historic stage of 27.15% above NAV. That is as a result of ongoing recession and the defensive market positioning in Utilities.

We love DNP and personal it, however have trimmed it considerably from our 401(ok) account and exited it from our private, actively traded account. We’re robust believers in imply reversion, and overbought circumstances are usually adopted by a reversion to historic averages. Now we have seen this time and time once more, most just lately with the FAANG cohort in 2020/2021 and with one other CEF we love, particularly ETV. We known as out the fund when its premium reached historic highs mid 2022 in our article right here, and certainly sufficient the premium contracted by greater than 12% within the subsequent months.

Now we have an identical scenario on our arms with DNP, however with a double whammy function – the CEF is overbought from a premium perspective, whereas the underlying asset class can also be overbought through historic excessive P/E ratios. General Utilities is a superb, defensive asset class with wonderful long run outcomes, however do anticipate a imply reversion right here. Because the recession will get priced in and equities begin bottoming out, market contributors are going to rotate out of defensive shares (Utilities and Healthcare) into extra aggressive names that are actually overwhelmed down. We’re lightening up on our DNP place now, seeking to re-enter the identify later within the yr at ranges -10% to -15% decrease than at present’s worth.

{kind=link}