Editor’s word: In search of Alpha is proud to welcome Francesco Infusino as a brand new contributor. It is easy to grow to be a In search of Alpha contributor and earn cash on your greatest funding concepts. Lively contributors additionally get free entry to SA Premium. Click on right here to seek out out extra »

mbbirdy

With Malibu Boats (NASDAQ:MBUU) experiencing a historic wave of progress off of the COVID-19 pandemic and the retirement wave, I imagine that the corporate’s true success and future alternatives have been undermined. With their sturdy presence within the boating market mixed with their diversified product segments securing a secure and affluent future, I’d fee the MBUU inventory a Sturdy Purchase, as the corporate has proven implausible progress with strong fundamentals to help a a lot larger value producing far above-average upsides, as defined later on this article.

Enterprise Overview

Malibu Boats is a luxurious boat producer based in 1982 and produces in 3 services situated in Tennessee, California, and New South Wales, Australia. The corporate capabilities via the Malibu, Saltwater Fishing, and Cobalt segments underneath the Malibu, Axis, Pursuit, Maverick, Cobia, Pathfinder, Hewes, and Cobalt manufacturers creating the last word on-the-water life-style. With a market capitalization of $1.171 billion, ROIC of twenty-two.32%, a 52-week excessive of $72.47, and a low of $46.30, a value of $57.55 attracts my curiosity as a result of weak value efficiency after the corporate had implausible progress numbers in revenues and web revenue, as displayed beneath.

Malibu Boats 1Y Efficiency (In search of Alpha) Malibu Boats Development in A number of Key Metrics (Buying and selling View)

This historic progress from earlier quarters was exemplified by the Q1 2023 earnings which have returned strong outcomes and steering, with web gross sales rising 19.2% to a report $302.2 million, and unit quantity rising to 10.5% to a report 2,237 items. Though Malibu has acknowledged that gross sales progress will barely lower as a consequence of pandemic booms, I imagine the corporate has sturdy progress potential for the long run because it has achieved a 25% improve in gross sales for Cobalt boats on the Fort Lauderdale present, which is a good indicator for future quarters, and has spectacular backlogs on Pursuit Boats extending into the second half of fiscal yr 2024.

I imagine that Malibu Boats has implausible potential as a consequence of 3 predominant driving elements – strategic acquisitions that may propel the corporate’s progress in a number of product segments; vertical integration efforts which is able to generate sturdy revenue margins within the far future and keep away from potential provide chain points; and huge loyal seller community that may assist generate sturdy pricing energy within the business.

Thesis Driver #1: Current Strategic Acquisitions will Enable for Sturdy Future Development

Malibu Boats

Cobalt Boats

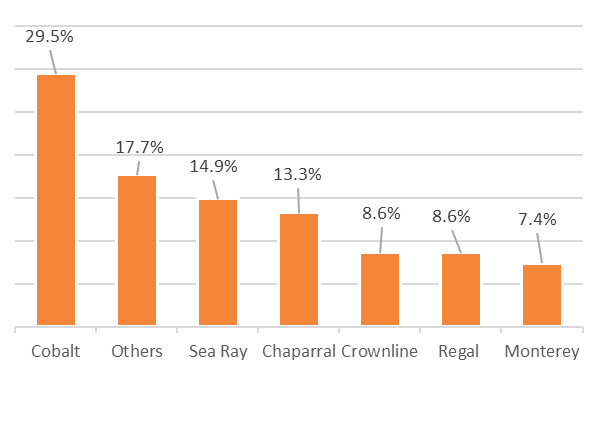

With their first acquisition of Cobalt Boats in 2017 for $130 million, Malibu was in a position to clear a direct competitor leading to larger pricing energy and margins as a consequence of decreased competitors in the long run. The acquisition additionally offered one other phase of progress for the corporate, with it seeing a implausible 25% progress in revenues from the fiscal yr 2021-2022. Not solely did the acquisition foster a brand new progress stream, however it additionally has given Malibu the #1 market share in america for the sterndrive phase of the leisure powerboat business for fashions ranging between 24′-29′, rising from 14.2% to 29.5% since 2010.

Cobalt Boats Lead in 24′-29′ Sterndrive Section (Created by creator utilizing Malibu Boats annual report)

Pursuit Boats

The second strategic acquisition that Malibu made was Pursuit Boats for $100 million in 2018. This buy generated the initiative for Malibu to dive right into a extra luxurious phase of the boating business. With the powerboat business seeing a median annual progress of virtually 20%, there’s a sturdy future forward for this phase of the corporate into new territory the place additional revenues and earnings might be generated.

Maverick Boating Group

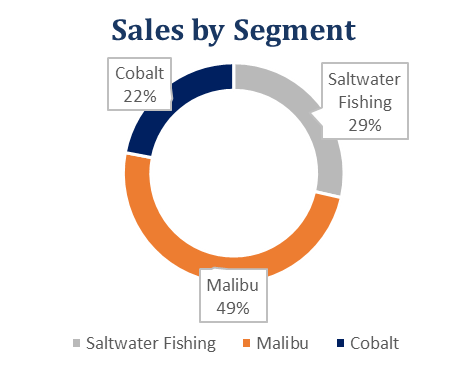

The third massive buy that Malibu made was of Maverick Boating Group in early 2021 for $150 million. With this latest acquisition, Malibu was in a position to take the management place within the bay boat phase giving them a robust market presence with sturdy pricing energy from the start. Moreover, this improve into the saltwater phase has allowed for progress from 18.9% of whole revenues in 2020 to 29% in 2022.

Malibu Boats Income Breakdown (Created by creator utilizing Malibu Boats annual report)

Thesis Driver #2: Vertical Integration Together with Progressive Options will Result in Success

My second progress driver for Malibu Boats is their efficient use of vertical integration, and new improvements and the way they’ll foster progress in profitability. Not too long ago, Malibu Boats has developed the flexibility to create a number of elements and lodging for his or her boats. This effectivity within the creation of their merchandise has allowed for larger margins per boat bought. Within the present state of provide chain shortages and corporations struggling to catch as much as demand, Malibu creating these elements domestically permits them to enhance upon their effectivity and outpace rivals, particularly in an business the place the season of use is brief and time is of nice significance. An instance of this initiative is the introduction of Malibu Electronics, LLC, which is a lately established, wholly-owned, direct subsidiary of Boats LLC. Malibu Electronics was signed into an asset buy settlement on February 1, 2022, in an effort to buy sure property from Amtech, LLC. Buying its predominant supplier {of electrical} harnesses for boats made by Malibu and Axis will permit for additional integration into their predominant income supply and reduce prices of manufacturing having a constructive influence on long-term margins.

Thesis Driver #3: In depth International Vendor Community Generates a Aggressive Benefit

The final of my thesis factors for Malibu Boats is that the corporate holds shut connections with over 300 sellers in North America and one other 100 in Europe, Asia, South Africa, and the Center East. With every settlement with massive sellers from 1-3 years and over half of the sellers have been with Malibu for 10 years or extra, Malibu may have the flexibility to have management over a big group of sellers, thereby lowering the competitors with different firms. With Malibu in a position to prepare conditional rebates, regular seasonal reductions, and flooring plan financing preparations with sellers which smaller rivals on this fragmented market can not, it provides way more bargaining energy over rivals, as the corporate talked about of their 2022 annual report, that they’ll “proceed increasing” their community resulting in extra shopper entry sooner or later. Lastly, the big seller community that Malibu holds helps my thesis of the inventory being a low-risk, progress funding as a result of lack of latest entrants. That is as a result of massive clientele new corporations should develop earlier than turning into a sizeable drive, giving Malibu ample time to find threats far earlier than they grow to be main rivals.

Analyst Consensus

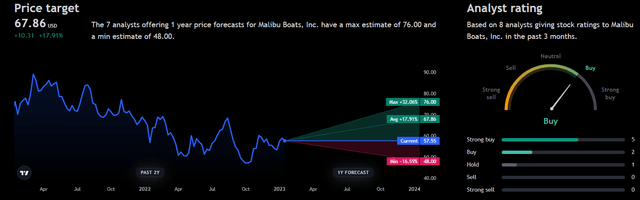

My ranking of Malibu boats is strongly supported by analysts predictions with over half of them ranking the inventory as a Sturdy Purchase. This constructive look on the inventory is additional strengthened by the common estimate of its 1Y efficiency appreciating to $67.86/share, which suggests a 17.91% upside.

Malibu Boats Analyst Consensus (Buying and selling View)

Valuation

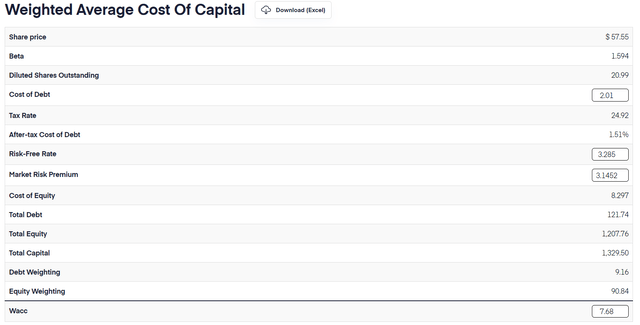

Earlier than performing my DCF evaluation, I generated a WACC for Malibu Boats utilizing a market threat premium of three.1452. This gave me a WACC of seven.68%, which is beneath the business common of seven.98%.

Malibu Boats WACC Calculation (Created by creator utilizing Monetary Modelling Prep)

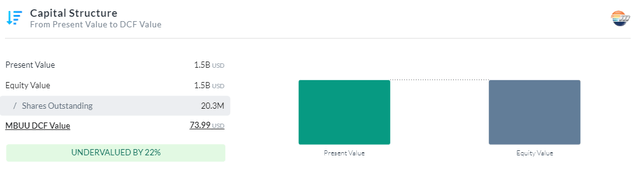

Going by my unlevered DCF calculations, at its base case, Malibu Boats is undervalued by 22% with a good worth being ~$73.99, through the use of a reduction fee of 10% over a 5-year interval. With a WACC of seven.68%, I added 2.32% to my low cost fee as a consequence of market headwinds corresponding to excessive rates of interest and a looming recession. For my income assumptions, I maintained a sluggish progress within the forecast for 2023 and 2024 as a result of potential recession as a consequence of fee hikes and inflation doubtlessly impacting shopper buying energy. I then integrated analyst predictions for income within the following years as it’s within the far future and the expansion is supported by my 3 drivers listed above. I then assumed that Web CapEx will proceed to develop as a result of Malibu Boats has acknowledged that acquisitions and elevated vertical integration are of nice curiosity to them, resulting in elevated expenditures.

Malibu Boats DCF Mannequin (Created by creator utilizing Alpha Unfold) Malibu Boats Capital Construction (Created by creator utilizing Alpha Unfold)

Dangers

Unfavorable Financial Situations: With high-interest charges and extra hikes all through this yr mixed with powerful inflation, we might even see a recession in 2023. This financial downturn will harm Malibu Boats considerably as a result of they’re within the shopper discretionary business, which means many individuals won’t purchase boats in powerful instances or might even dump their boats, resulting in much less priceless clients sooner or later to repurchase from Malibu. This threat can also be supported by widespread figures corresponding to JPMorgan Chase (JPM) CEO Jamie Dimon, warning {that a} “very, very severe” mixture of headwinds was prone to tip each the U.S. and world economic system into recession by the center of subsequent yr.

Massive Acquisitions could not Maximize Potential Advantages: Because of the recency of Malibu’s strategic acquisitions, we don’t absolutely know if the corporate will have the ability to absolutely combine these new segments with ease, as we’re basing success on as little as 2 years (the Maverick Boat Group acquisition, for instance). This assumption could also be altered within the close to future once we are in a position to achieve a extra secure monitor report for the entire segments.

Competitors: With fast innovation within the leisure boating business in regard to know-how, manufacturers could possibly steal Malibu’s market share leading to a lack of clients. That is largely as a consequence of new boat layouts taking maintain, new GPS and security programs, and lastly, the introduction of electrical/hybrid boats within the close to future. To this point, Malibu has been in a position to not solely adapt but in addition outpace the competitors with improvements such because the surf gate and energy wedge applied sciences. Though they’re doing properly to date, this might change at any second as a consequence of fierce competitors to seize new boating clients, which makes it a average threat for me.

Conclusion

In conclusion, I view Malibu Boats as a Sturdy Purchase as it’s a firm that holds an enormous seller community and focuses on vertical integration and acquisitions to enrich its natural progress via fixed improvements. With the inventory being undervalued, presenting a 23% potential upside, I imagine the MBUU inventory is a implausible purchase granted you’re snug with the dangers acknowledged above.

{kind=link}