mdworschak/iStock by way of Getty Photographs

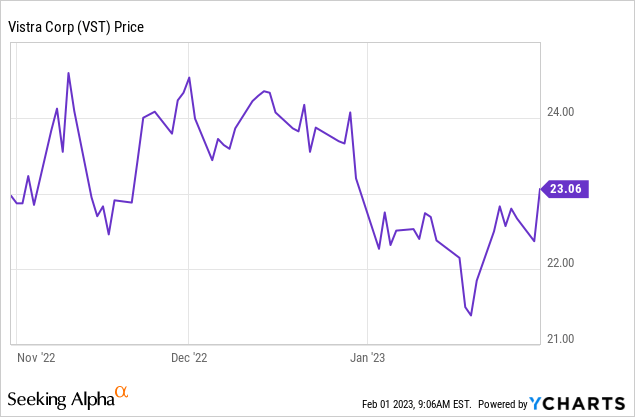

Vistra Corp. (NYSE:VST) is a Texas-based utility that operates 38,700 megawatts of energy technology belongings throughout the whole spectrum from coal to renewables. Like many friends, it’s pivoting in direction of renewable, attempting to maintain nuclear going and avoiding investing in coal technology. Within the final three months, the worth of this inventory hasn’t actually gone anyplace, which is stunning to me as a result of: 1) it’s fairly low-cost; and a couple of) it’s returning capital to shareholders aggressively.

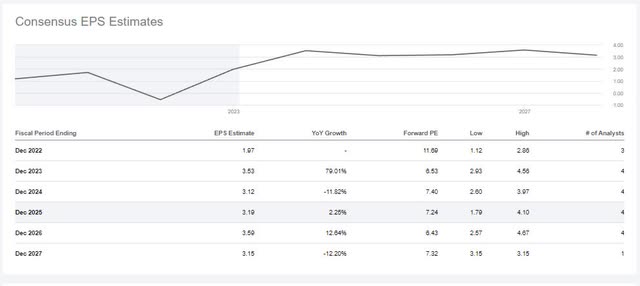

There aren’t that many analysts following the $9 billion market cap utility. Nonetheless, those that do have EPS above $3 per share in future years:

Vistra Corp analyst estimates (In search of Alpha)

That is fairly nice on a $23 utility inventory.

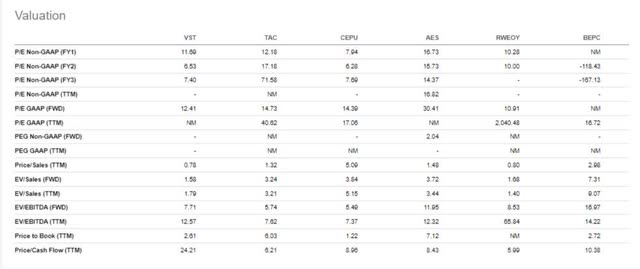

I additionally pulled up quite a lot of friends (assigned by In search of Alpha information, see under), and this reveals Vistra Corp. inventory is on the cheaper finish of the vary. I am not conversant in the rivals listed besides CEPU. In CEPU’s case, I imagine this can be very low-cost however these are Argentinian belongings. I do not see the valuation hole between Texas and Argentinian belongings disappearing anytime quickly.

Vistra Corp valuation (In search of Alpha)

Gasoline costs are vital enter prices, and these are notoriously unstable. Nonetheless, the corporate has hedged these prices for the upcoming years in keeping with the newest earnings name:

As you’ll count on, the business group has continued its execution of the great hedging program that we mentioned initially on the primary quarter earnings name, considerably derisking and locking in our future earnings potential for these out years. As of the top of the quarter, we have been roughly 70% hedged on common throughout all markets for 2023 by way of 2025, with 2023 being roughly 90% hedged.

What I actually like about this firm and its administration group is how aggressively Vistra Corp. is returning capital to shareholders. Over the past name administration identified they’d $1.2 billion of repurchases they have been going to make the most of earlier than yr finish 2023. Additionally they identified the $375 million that was earmarked to exit as dividends. Collectively this makes up a complete “shareholder yield” of 17.34% on the present share value.

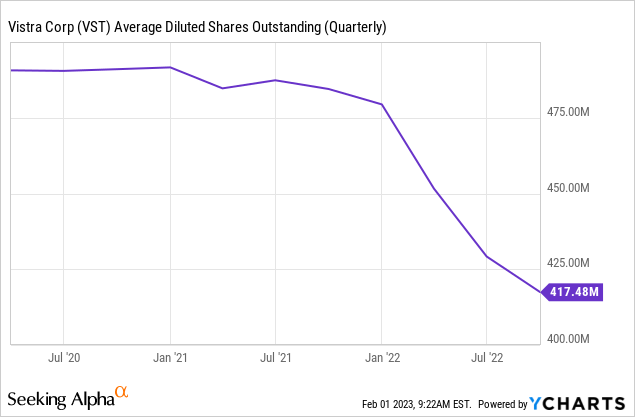

Aggressive buyback plans are all good and effectively, however corporations don’t all the time execute on these. I will not deny that however the firm does have a strong latest observe report of taking out substantial portions of shares:

The corporate can be lowering (and continues to take action) debt:

My large concern with vitality corporations, whether or not it’s Shell (SHEL) or utilities like this, is they may plow free money stream into subpar renewable technology belongings. Nonetheless, Vistra Corp. is as an alternative utilizing renewable investments to boost third get together capital. In my expertise, this capital is usually a bit cheaper as a result of there may be nice demand (resulting from ESG pressures) for inexperienced investments.

Vistra Corp Capital Allocation (Vistra Corp Presentation)

What I do not love about utilities is that they have a tendency to make use of a comparatively great amount of debt. It is sensible as a result of their income is pretty predictable, however it’s harmful if income disappears. In Vistra’s case, most maturities are past 2026. There are minimal maturities in 2023. The 2024 wall appears manageable, however the 2025 balloon maturities most likely must get termed out or paid down prematurely, or they will turn out to be problematic.

Vistra Corp debt maturities (Vistra Corp Q-10)

From the earnings name, I perceive administration is on prime of this:

Whereas returning money on to our shareholders stays a precedence, we are going to proceed to give attention to sustaining a powerful steadiness sheet. Importantly, we have now not deviated from our long-term internet leverage goal, excluding any non-recourse debt at Vistra Zero of lower than 3 times.

On our second quarter name, we famous that we anticipated to repay not less than $2.5 billion within the second half of the yr and we made important progress this quarter, repaying roughly $1.4 billion of debt. We count on to repay a further $1.1 billion of debt by yr finish.

The corporate is buying and selling at a pretty valuation (round ~7x ahead earnings), it’s lively in a protected line of enterprise that I am positive it will likely be round for fairly a while. The shareholder yield is in extra of ~14%. The dividend yield is not that particular at 3.3%, however it’s not one thing to disregard. Administration is strategically elevating capital the place it’s advantageous and returning capital in one other advantageous approach. I count on the corporate will report earnings in February, and I am particularly to listen to how they’re progressing with the buyback and the debt paydown.

As issues stand, with administration executing, I like Vistra Corp. in my portfolio. I feel Vistra Corp. is a really affordable shopping for alternative, whereas the market appears to be ignoring the robust shareholder yield by way of buybacks and modest dividends.

{kind=link}