humanmade

“Your thoughts is sort of a parachute: If it is not open, it would not work.” -Buzz Aldrin

The Macro View

The basics stay weak. Manufacturing is horrible. Housing is in a deep hunch. Proof of a client who’s working out of steam continues to mount. With job development doubling output, productiveness is falling. The very best yield-curve recession indicator, the 3-month/10-year Treasury unfold, is as inverted as it has been since 1981! Nonetheless, as famous final weekend oftentimes the technicals will begin to enhance properly earlier than the financial image brightens. Whether or not it’s optimistic or unfavorable, the market is in search of that “change”.

With financial knowledge at lows, suffice it to say it might appear that there’s just one approach to go on the sequence of unhealthy information, and that’s up. That leaves me with a notion of what was talked about throughout the week. The inventory market is trying forward, and if we’re already in a recession it is monitoring the “change” that would happen. Monitoring a stabilizing sequence of knowledge experiences could be thought-about a win within the close to time period. Nonetheless, the burning query is how lengthy will it take earlier than we see significant and extra importantly sustained positives being reported for the economic system. What has modified within the final month is the “China reopening commerce”, which is sparking a rally within the Eurozone that’s the greatest begin to a yr since 1987.

Many issues technically have improved, however (in the end) the large image has not modified yet- the dominant pattern remains to be down for now. General, the web result’s a market which will turn out to be extra range-bound over the approaching months, doubtlessly between ~3700-4300. We’re only a yr faraway from probably the most extraordinary financial and financial stimulus in our lifetimes-more than $9 trillion that was adopted by probably the most aggressive Fed tightening in historical past -There is no playbook for this. It is why there are quite a lot of questions however little in the best way of solutions. Let’s examine if we will make sense of the state of affairs primarily based on what we all know right this moment.

Credit score Spreads lean towards a extra optimistic near-term market.

Excessive-yield CDS spreads basically replicate the price to insure towards firm defaults- and have been a superb indicator of fairness market traits over the previous yr. After trending solidly upward within the first half of 2022 (as inflation considerations intensified), CDS spreads have trended typically sideways since mid-2022.

Consequently, this has correlated with an S&P 500 pattern that has additionally turn out to be extra sideways over the previous six months. A optimistic divergence may be seen on this view- whereas CDS spreads have narrowed again to August lows, the S&P 500 remains to be properly beneath its August highs of 4300. This implies additional upside and will increase the chance that the S&P 500 retests ~4300 in some unspecified time in the future.

A possible drawback looms with this This fall Earnings Season: It’s only just the start of This fall earnings season, however thus far outcomes are coming in beneath historic averages. 63% of S&P 500 firms are beating estimates by 4% (vs 15-year averages of 70% and 5.4%, respectively). Steerage can also be being lower with 2023 earnings estimates transferring broadly decrease. For instance, the banks are setting apart additional reserves for an anticipated rise in mortgage delinquencies.

With the typical S&P 500 inventory now properly off its lows, weak outcomes this earnings season could also be extra of a headwind. This fall earnings season is ramping up and the outcomes will go a good distance in figuring out near-term worth motion. A base case expectation for a 2023 earnings estimate of $215 (beneath the present bottom-up analyst estimate of $227) might be extra in keeping with actuality. Little doubt PEs reached an elevated degree within the zero rate of interest backdrop, so we’re coming down from these lofty ranges. However once I drill into the numbers, I discover that on an annual foundation, the P/E has fallen 42% since 2021, marking the biggest two-year contraction in almost 50 years.

There’s yet one more “issue” that may preserve the market steady. Once I check out the typical P/E a number of relationship again to 1960 regarding numerous ‘ranges’ for inflation, it presents an attention-grabbing image. If the consensus view is that inflation has peaked and is coming down that helps a number of enlargement. In fact, it is solely ONE issue that goes within the PE equation, however once we enter a interval the place the positives are embellished the “different” components are pushed to the background.

Close to Time period Conclusion

Historical past means that moderating inflationary pressures, and a much less aggressive Fed displays any ‘unhealthy information’ on charges has been priced into the a number of. Secondly, traders already “know” there shall be successful to earnings this yr, and relying on the severity of the decline, some, if not all of that has ALSO been factored in.

Worth is the ultimate arbiter, and within the quick time period worth is a operate of investor sentiment. We frequently expertise durations the place the negatives are positioned on the again shelf and the positives are embellished. We’re experiencing a type of time frames now. I take my cues from the inexperienced shoots that the technicals are sprouting. From there I can conclude the intermediate time period is trying extra optimistic as we start to shut out Q1 and enter Q2. Let’s not take that as an all-out BULLISH reversal, the place I’m going out and purchase something and all the things. There’ll nonetheless be loads of irritating and questionable moments, and I will not change my view that “selectivity” on this backdrop shall be a key to success. Bear in mind, this evaluation relies on the enhancing technical image. It can disintegrate IF assist ranges that we have now outlined as KEY pivots are violated. That isn’t uncommon once we are coping with a inventory market that’s NOT in a “Full Velocity Forward” BULL market backdrop that we noticed earlier than 2022.

Selectivity is Key

If this evaluation seems to unfold as I anticipate, it’ll imply that merchants can begin to take a look at a number of the high quality shares which might be displaying “reversal” patterns. This stays a bifurcated market with the indices following completely different paths, so it isn’t a Inventory market the place all is aligned. We have seen that for some time and it all the time leads us again to a key to my strategy- Selectivity.

The best way I view the MACRO image now has a slight twist to it. I can envision a “get together” to have fun the Fed leaving the scene and rates of interest that may STOP going UP. How lengthy this get together lasts is unknown. As all the time it is determined by a complete bunch of variables most of that are unknown to us now.

In some unspecified time in the future, the truth of a sluggish/no development economic system units in. In fact, that isn’t set in stone simply but. However the concrete truck is on the scene able to pour. The troublesome funding setting remains to be right here and I believe that the headline-driven backdrop goes to proceed within the months forward. Altering plans because the scene unfolds is a testomony to working with an Open Thoughts.

The World Scene

A Bloomberg survey of economists revealed an anticipated 5.1% development in China’s GDP in 2023 because the nation reopens after COVID lockdowns. The extent to which the Chinese language economic system is normalizing shall be seen over the following a number of weeks, amid the Lunar New 12 months journey season. The vacation will happen on January 22, and the related journey season encompasses as much as 40 days.

Generally known as the world’s largest annual human migration, a whole lot of thousands and thousands of individuals will journey, typically from city areas to go to their family members within the countryside. China’s transport ministry expects greater than two billion passenger journeys, doubling from the lockdown-impacted degree of 2021. All this journey, in fact, is prone to exacerbate the post-lockdown COVID wave, doubtlessly main to provide chain disruptions as factories and different companies face employee shortages.

So whereas that could possibly be a near-term unfavorable, if these forecasts are wherever near being appropriate, it confirms the view that China will start to dominate the financial stage. I’ve talked about this earlier than. They’ve what each the US and the EU want to take care of their “inexperienced” behavior. That habit retains China in management whether or not some need to acknowledge that or not.

The Week On Wall Avenue

Sellers dominated the Monday session as the worth motion remained weak all day. Each Index and all eleven sectors posted losses. Turnaround Tuesday arrived and the entire indices and sectors ripped larger. It was a much-needed turnaround for the Bulls with the S&P clawing again (+1.5%) the entire earlier day’s losses.

FOMC day unfolded and after some indecision, the rally ensued, culminating with the S&P closing at a brand new restoration excessive. Nonetheless, it was fairly evident cash was rotating out of what was the outperformer, the DJIA, and into different areas of the market. The NASDAQ added 2% and the small caps (IWM) posted a 1.4% acquire. Each of these features add extra affirmation to the breakouts that had been famous within the charts. The DJIA ended the day with a 6-point acquire whereas the entire different indices had been larger by 1-2%. The reversal of the 2022 Worth commerce continued into Thursday’s motion as properly.

Aside from the DJIA, the key indices continued the rally that’s concentrating on development and the beaten-down areas of the market. When the mud settled on Thursday all Indices besides the DJIA had been “extraordinarily” overbought. After the shut, Apple, Amazon, Alphabet, and Starbucks, all reported earnings that missed estimates.

Friday’s session was combined, and if that’s all BEARS may muster with that information backdrop, it reveals how near-term sentiment has modified.

The FED

No surprises right here. The Federal Reserve’s assertion;

“The Committee seeks to attain most employment and inflation on the charge of two % over the longer run. In assist of those targets, the Committee determined to lift the goal vary for the federal funds charge 25 foundation factors to 4-1/2 to 4-3/4 %. The Committee anticipates that ongoing will increase within the goal vary shall be acceptable in an effort to attain a stance of financial coverage that’s sufficiently restrictive to return inflation to 2 % over time.

In figuring out the extent of future will increase within the goal vary, the Committee will consider the cumulative tightening of financial coverage, the lags with which financial coverage impacts financial exercise and inflation, and financial and monetary developments. As well as, the Committee will proceed decreasing its holdings of Treasury securities and company debt and company mortgage-backed securities, as described in its beforehand introduced plans. The Committee is strongly dedicated to returning inflation to its 2 % goal.”

Since they talked about “2% inflation” 3 times in two paragraphs, we will assume they’re intent on staying on a path to attain that purpose.

The Financial system

Employment And Inflation

The January nonfarm payroll report left nearly each economist scratching their head. Whole nonfarm payroll employment rose by 517,000 in January, and the unemployment charge modified little at 3.4 %. I will not try to determine why this report was so sturdy. I do know the “employment element” that’s being reported in ISM and different surveys isn’t aligned with sturdy job development. That provides extra confusion to the financial image.

If we need to make the case that the economic system is powerful primarily based on this jobs report, it raises a number of questions. Will development be sluggish sufficient to deliver down the inflation charge? Will considerably larger rates of interest be required to make that occur?

Then once more, maybe wage development is not feeding into the inflation concern and if it was, it had a minimal impact. Inflation is subsiding whereas wage development stays sturdy. That means inflation is all about what has been mentioned right here for months. Extra spending and power insurance policies.

Confused? You need to be. The ‘knowledge’ is sending combined alerts, and the knowledgeable are as confused as you might be.

Manufacturing

No change within the subpar manufacturing knowledge that’s being reported.

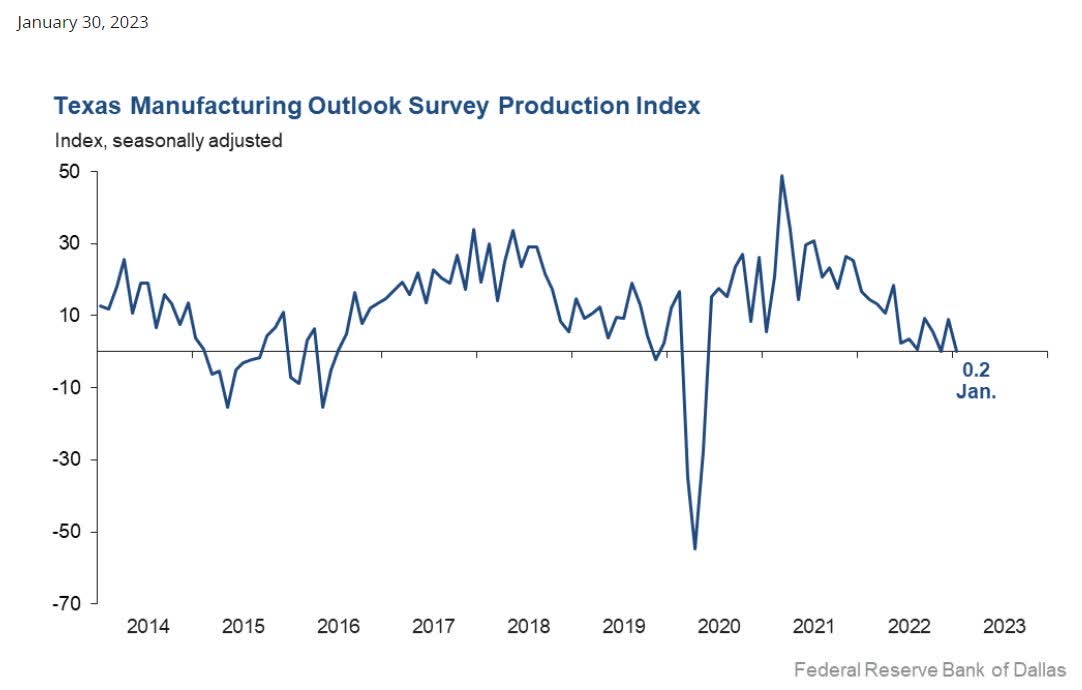

The Dallas Fed Manufacturing Index confirmed development in Texas manufacturing unit exercise slowed in January. The manufacturing index, a key measure of state manufacturing circumstances, fell from 9.1 to 0.2, with the near-zero studying suggestive of a flat output.

Dallas Fed Manufacturing (dallasfed.org)

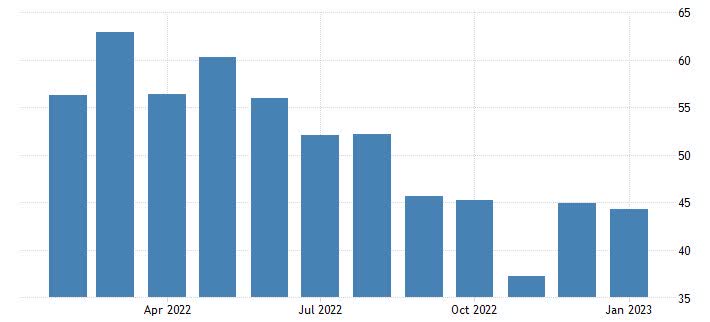

Chicago PMI dropped to 44.3 in January from 45.1in December leaving a fifth consecutive sub-50 contractionary studying. Many of the numerous element classes are actually in contraction territory. Analysts anticipate the ISM-adjusted common of the key sentiment surveys to fall to a 3-year low of 48 in January.

Chicago PMI (tradingeconomics.com)

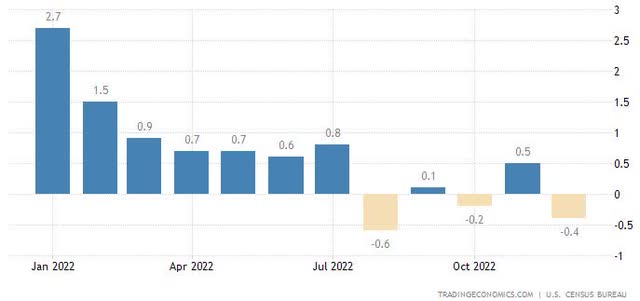

Development spending beat estimates through big upward revisions, although analysts noticed a 0.4% December drop. Development spending posted a 0.9% development charge in This fall, after charges of three.4% in Q3, 10.3% in Q2, and 22.3% in Q1.

Const. Spending (www.tradingeconomics.com/)

That pushed analysts to decrease the Q1 GDP estimate to -0.8% from -1.0%.

The ISM manufacturing index declined 1 level to 47.4 in January after dipping 0.6 ticks to 48.4 in December following annual revisions. That is the fifth straight drop and is the bottom since Could 2020. It has been in contraction for 3 consecutive months.

ISM Manufacturing (ycharts.com)

ISM knowledge has been in regular decline for properly over a yr now.

Client

The U.S. client confidence index dropped to 107.1 in January from what was an 8-month excessive of 109.0. The Convention Board survey has revealed a surprisingly resilient path relative to the opposite confidence gauges since peaks in mid-2021. At the moment’s client confidence drop joins a Michigan sentiment rise to a 9-month excessive of 64.9 from 59.7, which leaves that measure nonetheless properly beneath the early pandemic backside of 71.8 in April of 2020.

The IBD/TIPP index fell to 42.3 from 42.9, versus an 11-year low of 38.1 in August. Analysts have seen a confidence updraft since mid-2022, although the entire measures have deteriorated sharply from mid-2021 peaks, and Michigan sentiment is fluctuating round remarkably weak ranges whereas the Convention Board measure has remained comparatively elevated.

The underside line; client surveys replicate the financial circumstances, poor.

The World Financial system

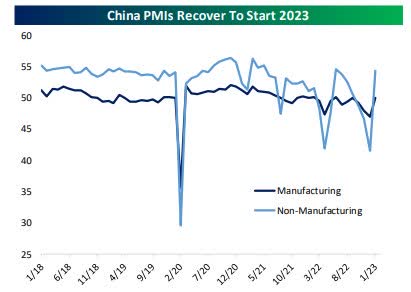

Chinese language PMI knowledge surged to start out 2023 as manufacturing returned to enlargement in-line with estimates versus an enormous surge in companies that topped economist views considerably. As proven beneath, outcomes are close to one of the best ranges of the previous 18 months and provide hope that the disruptions of COVID are beginning to path off.

Chinese language PMI (bespokepremium.com)

Additionally of be aware, the sub-PMI index that tracks the metal trade noticed the best stock studying since early 2020. Spot metal costs onshore hit the best yuan costs since early July final night time after flying 2% larger to start out the week.

This optimistic goes a good distance in solidifying the notion that the worldwide economic system can now stabilize.

World Manufacturing PMIs stabilize however for probably the most half, stay in contraction

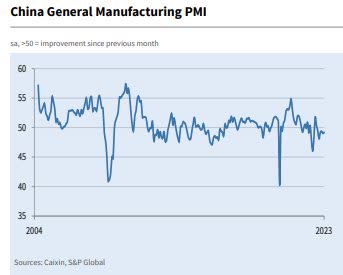

China

The headline Caixin China Manufacturing Buying Managers’ Index – rose from 49.0 on the finish of 2022 to 49.2 in January, to sign a decline within the well being of China’s manufacturing sector for the sixth month in a row. That stated, the speed of decay eased from December and was solely marginal.

Caixin China PMI (pmi.spglobal.com)

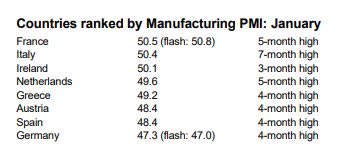

Eurozone

Manufacturing PMI at 48.8 (Dec: 47.8). 5-month excessive.

Manufacturing Output Index at 48.9 (Dec: 47.8). 7-month excessive.

Eurozone PMIs (spglobal.com)

Whereas there may be enchancment be aware that the majority of knowledge stays in contraction. (sub 50)

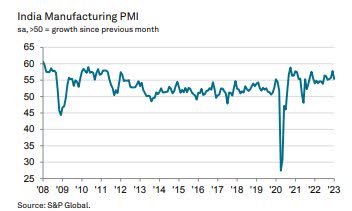

India

January knowledge confirmed an extra enchancment within the well being of the Indian manufacturing trade. Posting 55.4 in January, the seasonally adjusted India Manufacturing Buying Managers’ Index highlighted a nineteenth successive month-to-month enchancment in working circumstances.

India PMI (pmi.spglobal.com)

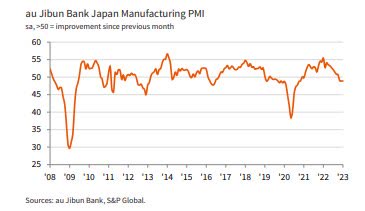

Japan

At 48.9 in January, the headline au Jibun Financial institution Japan Manufacturing Buying Managers’ Index remained beneath the impartial 50.0 threshold for the third month working. Nonetheless, the index was unchanged since December and thereby prompt an general stabilization of producing sector enterprise circumstances.

Japan PMI (pmi.spglobal.com)

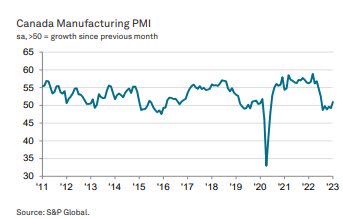

Canada

Canada’s manufacturing economic system registered a return to modest development throughout January. Canada Manufacturing Buying Managers’ Index recorded 51.0 in January, up from 49.2 on the finish of 2022. The most recent knowledge marked the primary time that the index has recorded above the 50.0 no-change mark that separates development from contraction since final July

Canada PMI (pmi.spglobal.com)

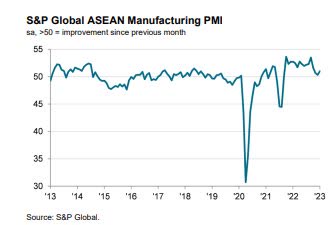

ASEAN manufacturing corporations reported an enchancment in working circumstances firstly of 2023. The headline PMI picked up from 50.3 in December to a three-month excessive of 51.0.

ASEAN PMI (pmi.spglobal.com)

4 of the seven ASEAN nations monitored by the survey registered development throughout their manufacturing sector in January, up from three in December.

World Providers PMI knowledge from a spread of worldwide economies was broadly improved and better than expectations, with China performing equally to the spike within the official sector PMI knowledge reported earlier within the week and the Eurozone’s uptrend persevering with for an additional month.

World Providers PMI (bespokepremium.com)

Composite output PMIs, which measure manufacturing and nothing else (in contrast to manufacturing and companies headline indices) had been combined. Smaller economies proceed to sluggish whereas the opposite two of the world’s largest three financial blocs are each seeing a particular inflection larger over the previous few months as COVID-Zero and the power shock each put on off.

Meals For Thought

All ESG, on a regular basis. ESG investing is the brand new mantra driving a theme that has seemingly taken over the minds of many funding corporations. ESG investing highlights environmental, social, and governance rules and is meant to attenuate dangers tied to these three components.

As a result of environmental, social, and governmental methods exclude many securities and a few sectors of the market, ESG-focused merchandise could not have the ability to reap the benefits of the identical alternatives or market traits as merchandise that don’t use such methods. Moreover, the factors used to pick out firms for funding could end in investing in securities, industries, or sectors that underperform the market as a complete.

The pushback on this “funding scheme” is simply starting to take root. West Virginia is without doubt one of the newest to tackle the ESG mania. Texas, Florida, West Virginia, North Dakota, Oklahoma, Minnesota, Idaho, South Carolina, Louisiana, Idaho, Wyoming, Arizona, Kentucky, Utah, Indiana, Missouri, Ohio, and South Dakota are actually adopting ESG bans.

Moreover the ethical or ideological conflicts that one might need with “ESG” investing, many state pension funds are beginning to take a look at outcomes. If a portfolio did not embody the power sector final yr it was destroyed. As well as, companies pressured into this regulatory nightmare are additionally questioning their stance. That is because of investor backlash which is now questioning company fiduciary accountability to shareholders. By its strict selective nature, ESG strikes fiduciary accountability to the background. It’s this precept that for my part makes it in direct battle with capitalism and uninvestable.

200 years in the past the world was dominated by poverty. One thing known as “Capitalism” got here alongside and all of that modified. Capitalism has taken extra individuals out of poverty than another system in historical past. But it appears many proceed to derive “schemes” to derail the system. From the place I sit ESG is a type of schemes. Every can determine for themselves how they need to proceed, however as a matter of non-public selection, I’ve determined I am not taken with any of the ESG-related funding automobiles. Choosing winners and losers by defining particular ‘standards’ is not what I’m taken with. Like anybody else that appears at a monetary assertion, I’m involved about how a lot cash a company is now being pressured to toss at this “concern” to be compliant. Telling an trade they can not put money into a sector as a result of it would not “match” sure standards isn’t in keeping with a capitalist society. In spite of everything, I’m a shareholder in a capitalist society, and each company has a fiduciary accountability to its shareholders.

The underside line is; Shareholders are all the time on the high of the meals chain in the case of company governance. There are lots of different rules and mandates coping with greenhouse gases, social points, and so on. with out dragging the monetary system into the fray. I am unable to communicate for anybody else, however I for one don’t desire the Federal Reserve having to cope with “local weather” points when they’re preventing 40-year highs in inflation.

The fact is the extra companies must spend on research about their greenhouse gasoline emissions, social compliances, and so on., the extra their services or products are going to value everybody else. To not point out many companies had been already good residents properly earlier than ESG mandates got here alongside. They had been in a position to allocate assets to handle points at their very own tempo. ESG calls for will have an effect on each company’s backside line. Subsequently, once we add all of it up, the “value-added quotient” is negligible. It is merely one other “handcuff” on Company America and a risk to capitalism.

The Day by day Chart of the S&P 500 (NYSEARCA:SPY)

Sentiment stays within the glass half-full mode and the BEARS are scrambling. A full-fledged breakout and the one query is how far can this mini uptrend go?

S&P 500 (FreeStockCharts.com)

The August highs would be the subsequent resistance zone, however the BULLS have a confluence of assist within the 3950-4000 vary. So the battle strains have been drawn.

It is your transfer. Glass half full? or Glass half empty?

Funding Backdrop

With the 10-year Treasury yield holding regular down close to 3.5% and the greenback index additionally behaving (by not rallying), traders have continued to push into shares to start out the yr. January has been a whole reversal of the motion we noticed in 2022. The Nasdaq, Client Discretionary, Communication Providers, and Know-how have been 2023’s largest winners, and these had been final yr’s largest losers. On the similar time, defensive sectors like Client Staples and Utilities have been lagging.

It is attention-grabbing that on the similar time, the yield curve and nearly all of financial indicators are telling us a recession is sort of a assure, the inventory market is buying and selling from a stance of financial energy with cyclicals outperforming and defensives underperforming.

Final week we noticed the US outperform most different nation ETFs, however worldwide markets stay properly forward of the US year-to-date. The all-world ex-US ETF (CWI) is up 9.3% YTD versus a acquire of 6% for SPY.

That brings us to the RESULTS for the MONTH.

January is within the books and it was a robust month, with the key indices posting features throughout the board. The theme for this previous month has been the final shall now be first. The laggards in ’22 have led this rally. On the index degree, the NASDAQ led the best way with a ten+% acquire, adopted by the Russell small caps (9+%). The S&P 500 rallied 6+%, and what had been the chief final yr, the DJIA posted a subdued 2.8% acquire for the month.

I will be aware that these January features have been pushed even larger within the preliminary buying and selling days of February.

On the sector degree, it was the previously beaten-down semiconductors opening the yr with a 16% rally in January. Client Discretionary was one other sector that was crushed in ’22, it reversed sharply, and gained 15%. Vitality (XLE) was flat with a modest 2.7% rally, whereas the newly designated Savvy Scorching Spot for ’22 within the power sector, the Oil Providers group (IEZ) outperformed with an 8.3% rally.

Small-cap development (+11%) beat out small-cap worth (9.8%). On the commodity scene, Gold rallied 5.7%, Silver was flat dropping ~1%, and one other Savvy favourite, Uranium, rang the register with a 15% rally.

It has been a robust across-the-board rally that has left the complete inventory market in a particularly overbought situation. I’ve been content material with my positioning so I wasn’t chasing something this week.

Small Caps

The Russell small caps (IWM) was the primary index to vault over its 200-day MA and has now closed above that degree for 16 consecutive days. That proof solidifies the view that the breakout is real and will result in larger costs within the close to time period.

The IWM has now put in a detailed above $189, an space that I cited as resistance, because it capped the earlier 4 rallies. Right here is one other instance of an index that might want to get previous a former excessive (August/$201) to interrupt the sequence of decrease HIGHS. That is step one in turning across the BEAR market in small caps. As of the shut on Friday that has not been completed.

Sectors

Client Discretionary

This was the overachiever in January. The Discretionary ETF (XLY) misplaced 37% in ’22 and has clawed again ~20% of that loss because the starting of the yr. Some names look attention-grabbing right here, however others are buying and selling on “hope”. This can be a sector the place “selectivity” shall be crucial in ’23.

Cybersecurity

There are many analysts and analysis corporations that proceed to pound the desk on the sector. Little doubt of their argument that cybersecurity will command funding as expertise advances. Nonetheless, I simply cannot wrap my arms across the group on account of valuations.

Lastly, each particular person inventory and cybersecurity ETF stays in a deep BEAR market. I will sit again and wait till I see the group break UP and out into BULL traits. I’ll miss the preliminary a part of any rebound however I will additionally eradicate the danger of this group imploding if shares with HIGH valuations are jettisoned once more. PATIENCE is the secret.

Vitality

The Vitality ETF (XLE) is again at a degree that has been a tricky space to crack. The ETF has as soon as once more hit its head on the $94 degree. With the rally in crude oil pausing this week, it despatched the power sector decrease. It’s the third time it has been rebuffed at this resistance degree since final June. As soon as once more, the BULLS shall be seeking to see how deep any pullback turns into, and if assist can maintain.

Since I take into account my power positioning – Lengthy Time period, I am prepared to experience the short-term waves that exist within the context of a bigger PRIMARY BULL market pattern.

Pure Gasoline

Final summer season, pure gasoline futures within the US had been buying and selling on the highest degree in over a decade, and there appeared to be no ceiling for costs as Europe approached winter. This week, nat gasoline is firmly beneath $3 and the bottom degree in a yr and a half. Over the past 100 buying and selling days, costs have plunged by a report 69%. My Long run positioning within the Nat gasoline ETF (UNG) is including extra gray hairs.

Financials

We have famous how shut the Monetary ETF (XLF) has come to breaking out, and every time it has failed. This week was certainly “completely different”. The ETF broke out to a brand new restoration excessive and for the primary time in fairly some time has damaged again right into a BULLISH pattern. The onus is on the BULLS to substantiate this current transfer, by pushing costs larger.

Industrials – Sub Sector – Protection

The Industrial ETF (XLI) (+2,6%) underperformed the S&P (+6%) in January. The sub-sector of “protection” (ITA) has lagged even additional with a acquire of 1.6% in January. At one level throughout the month, the protection sector bought off dropping 3% whereas the general market was rallying.

There are all the time quite a lot of causes for worth motion, however the main trigger for the poor efficiency in (ITA) thus far is linked to considerations about protection spending cuts. We have seen “political” rhetoric trigger short-term disruption in different sectors earlier than. Healthcare is the poster youngster for such knee-jerk reactions to “commentary”. Normally, it seems to current a chance for anybody that may look previous the quick time period. The identical applies right here. The “rhetoric” is extra “spin” than truth. It could appear that decreased assist for Ukraine within the new Congress is fiction. Home chairmen are lobbying for extra weapons to be despatched to Ukraine.

Since I missed the BULL market in most of the defense-related shares, I used to be of the mindset to try to add publicity throughout any dip within the main pattern. After listening to completely different protection firm earnings calls, I got here away with the identical message from every. Aiding Ukraine in its protection towards Russia has depleted the provision of armaments right here within the US. Within the case of Lockheed Martin (LMT), they estimate it’ll take years to deliver provide ranges again to ranges which might be thought-about “routine provide”. Firm order backlogs are already excessive, and until the federal government is able to function in a state of vulnerability (uncertain), extra orders to deliver our defenses again to regular shall be coming in.

We will anticipate extra bumps within the highway and knee-jerk reactions, however so long as the first BULL pattern on this sub-sector is in place there shall be a chance. For these that don’t need to tackle any particular person inventory danger, the Aerospace and Protection ETF (ITA) is on the cusp of one other breakout.

Healthcare

The Healthcare ETF was a laggard in January, however I am not able to lose curiosity within the group. For one, the sector stays in a long-term BULL pattern. Secondly, most of the healthcare shares will do comparatively properly in a weaker economic system. They’re being bought now as it is a easy reversion to the imply commerce. That presents a chance for “choose” healthcare names.

Biotech

Final week I spoke in regards to the Biotech (XBI) breakout and the newest worth motion brings us a much-anticipated follow-through that’s gaining extra traction. The index shall be coming right into a heavy resistance space within the $94-$96 vary. That’s the convergence of the April and August ’22 highs is aligned with the longer-term 20-MONTH transferring common.

Will probably be a tricky “ask” for the XBI to get via all of that resistance on the primary attempt. I will be seeking to loosen up on the place that was added final June at $64. This has been an immensely worthwhile commerce for Savvy traders and the majority of it occurred throughout a BEAR market.

Gold

Gold continues to look optimistic, and there may be loads of time to BUY. I’ve felt {that a} pullback was due and I nonetheless consider that to be the case. I’m not actually in a rush to chase it larger right here as a result of there may be potential for Gold to create a bigger transfer down the highway, and there shall be loads of alternatives for revenue if that happens.

The MACRO view of Gold seems to be arrange in a big cup-and-handle sort sample on its long-term chart. (GLD) broke down early final yr when Gold, fashioned a double high above $2050 and dropped down beneath $1650.

However maybe Gold is simply taking longer to type the “deal with” portion of the cup-and-handle. If that’s the case and Gold proceeds to satisfy the sample, then we should always anticipate Gold to go a lot larger within the years forward. So, I nonetheless consider the smarter play is for some type of retracement within the close to time period, however I believe we have to preserve Gold on our radars given the potential it holds.

Within the quick time period, I proceed to play the short-term transfer through the Gold Miners ETF (GDX). That may be a good “saucer” sample as you’ll ever see in a inventory chart.

Gold Miner ETF (FreeStockCharts.com)

The chart of (GDX) is one among many who I share each week with the entire members of my SAVVY market. So long as that uptrend line is not damaged, it pays to remain on board in case you have positions. With GDX pulling again to $30, there may be potential for a transfer to the $36-$40 vary. That in fact shall be depending on how Gold performs.

Silver

We’re seeing one other “problem” for holders of the Silver ETF (SLV) this week. The ETF broke beneath a key short-term assist degree. It is had a tough time getting via the $22 degree, and the BULLS shall be seeking to defend the $20 breakout degree.

Uranium

The Bull Case for this Treasured Metallic Has Not Modified

I’ve mentioned Uranium a number of occasions over the previous couple of years, but it surely’s been some time since I discussed it right here. That is as a result of little or no has occurred over the previous a number of months aside from loads of rangebound whipping round. But, the bull case for Uranium because the gas for the “clear” power with one of the best likelihood of truly working as a baseload Vitality supply is unbroken.

It was a giant subject of dialogue on the current World Financial Discussion board in Davos. All I heard late final yr about Uranium was the “BEARS” saying it was forming a Head and Shoulders high, however that seems to be breaking down, and infrequently when a potential sample fails to type it does the precise reverse as a substitute (in that case meaning larger).

I’ve had a place in Uranium since early final yr. Traders can use any one of many common ETFs like (URA) or (URNM). One other approach to take part is Sprott Inc. (SII), an organization that manages/maintains holdings and investments in valuable metals.

The Shorter-term view of URNM has additionally taken on a optimistic slant which has now pushed the ETF again right into a main BULL pattern.

Know-how

As famous earlier the NASDAQ composite led the best way throughout January, and that transfer could have been step one to slowly rebuild its closely broken technical sample. Earlier than this rally, the index didn’t see a detailed above its 200-day transferring common in over a yr and has now vaulted about that preliminary resistance. There’s further work to be finished earlier than we will declare the BAER market over within the NASDAQ, however step one has been taken.

Semiconductors Sub-Sector

Another excuse I really feel the market has justified being extra constructive these days is that the Semiconductor Index, which frequently leads the broad market, has been outperforming the S&P 500 and has damaged its downtrend strains on each its worth chart and its relative energy chart vs the S&P. This offers me extra confidence that maybe the current energy has some legs behind it to increase up additional.

The group (SOXX) was UP 17% in January. Much like the NASDAQ there are extra resistance obstacles forward so we should always anticipate pullbacks. Nonetheless, the SOXX chart has taken on a extra optimistic look that should not be dismissed simply but.

Cryptocurrency

Following large features earlier within the month, the rally in cryptos has begun to stall out. Throughout the biggest cryptos, worth motion has been combined with some property like Bitcoin rising whereas others like Ethereum have fallen prior to now week. Nonetheless, they continue to be overbought and buying and selling properly over one commonplace deviation above their 50-Day transferring averages.

Whole crypto market every day volumes have been subdued because the fall of FTX, bottoming round $33 billion on a rolling 50-day foundation mid-month; the bottom ranges since 2019. With January nearly over, we verify in on seasonality. Since 2015, February has ranked because the second strongest month of the yr for Bitcoin with a mean acquire of 13.87% and optimistic efficiency 87.5% of the time. Ethereum equally has regularly moved larger throughout the month albeit the typical acquire is much less spectacular relative to different months.

Cryptocurrency (bespokepremium.com)

Ultimate Ideas

I proceed to belief my technique whereas watching the inner indicators. That helps me keep in sync with the market it doesn’t matter what occurs. Regardless of my continued considerations in regards to the greater image, the near-term motion tells me to be extra constructive on the inventory market. The S&P is following the “bull path” that I outlined for members of my service over two weeks in the past. So long as costs continued to behave in a way in keeping with that path, shares can go larger.

If that modifications and I turn out to be extra cautious once more, it isn’t going to be due to any explicit information occasion however as a result of the steadiness of proof suggests warning. There’s an inverse correlation between efficiency and the way a lot information an investor takes in. An excessive amount of data will turn out to be overwhelming and result in evaluation paralysis. And because the information circulate by no means ends, there’ll all the time be one thing new to must consider if you’re making choices primarily based on headlines and speaking heads. As a substitute, I make use of a course of and that course of doesn’t change primarily based on what “would possibly” occur sooner or later due to some unsure information occasion. I’ve typically stated that it isn’t worthwhile to play the “what if recreation”.

Traders needs to be making choices primarily based on a number of components (costs, technical indicators, valuation, financial indicators, sentiment, intestine really feel, and so on.) however taking part in a guessing recreation about what the market would possibly do if this or that occurs within the information isn’t one among them. For one factor, the market I all the time one step forward of traders. It’s consistently discounting and pricing in all doable contingencies.

Analyzing worth motion over time is the method of analyzing how the market’s views are altering about no matter you occur to be charting. Once I observe “worth”, I’m in a method, following the information. If you’re, as a substitute, making choices immediately on what could occur sooner or later and the way the market could reply to it, you might be simply playing. You are taking part in a “guessing” recreation.

Bear in mind, there may be all the time one thing that would deliver down the markets. If you’re ready for all of the dangers to go away, you’ll by no means personal shares once more. And should you’re making an attempt to make choices primarily based on each doubtlessly market-moving information occasion, you’re going to have a tough time as a result of that by no means ends. The market isn’t a guessing recreation, despite the fact that many individuals deal with it as such.

THANKS to the entire readers that contribute to this discussion board to make these articles a greater expertise for everybody.

Better of Luck to Everybody!

{kind=link}