Klaus Vedfelt/DigitalVision by way of Getty Photographs

Funding Overview

IL-17 – A Drug Goal To Rival IL-23 / Skyrizi?

Yesterday the Pharma large AbbVie (ABBV) reported its FY22 earnings and supplied steering for 2023, which included a forecast for gross sales of autoimmune remedy Skyrizi of $7.4bn – up $2.2bn year-on-year. Administration additionally revealed that Skyrizi already has a >28% share of the US biologic psoriasis market.

Skyrizi – and a second autoimmune remedy Rinvoq – is AbbVie’s reply to the patent expiry of its all-time best-selling drug Humira, which was indicated for a spread of autoimmune circumstances.

Skyrizi works by focusing on the p19 subunit of IL-23, which is a cytokine (a sort of cell signalling protein) identified to play a key position in driving inflammatory illnesses together with Psoriasis, Psoriatic Arthritis, and Hydradentis Suppurativa.

The cytokine IL-23 types an axis with one other cytokine, often called IL-17, which, in line with a latest summary paper revealed on the Nationwide Library of Drugs web site:

performs a central position within the immunopathogenesis of psoriasis and associated comorbidities by performing to stimulate keratinocyte hyperproliferation and feed-forwarding circuits of perpetual T cell-mediated irritation. IL-17 performs an vital position within the downstream portion of the psoriatic inflammatory cascade.

This helps to clarify why a number of firms – for instance Immunic (IMUX), DICE Therapeutics (DICE), and MoonLake Immunotherapies (NASDAQ:MLTX) – the topic of this publish – are creating IL-17 focusing on medication for autoimmune / inflammatory circumstances.

MoonLake’s SLK – A Blockbuster Resolution?

MoonLake’s sole growth candidate Sonelokimab has some distinctive options that make the drug an fascinating proposition inside an autoimmune / inflammatory subject that’s admittedly crowded with blockbuster (>$1bn each year) promoting medication, comparable to Skyrizi, Rinvoq, Johnson & Johnson’s (JNJ) Stelara, Sanofi (SNY) / Regeneron’s (REGN) Dupixent, Amgen’s (AMGN) Enbrel, Biogen’s (BIIB), Tysabri, Bristol Myers Squibb’s (BMY) Zeposia and Orencia, and Novartis’ (NVS) Cosentyx.

MoonLake refers to Sonelokimab (“SLK”) as a “novel tri-specific Nanobody”, and an inhibitor of IL-17A and IL-17F. MoonLake licenses SLK from German Pharma Merck KGaA [XETR:MRK] (OTCPK:MKGAF) (OTCPK:MKKGY) – no relation to Merck & Co (MRK) within the US.

The drug has already been examined in a Part 2b study- by its former proprietor Merck, in partnership with United Kingdom primarily based Avillion LLP – in >300 sufferers with average to extreme Psoriasis, the place it appeared to check favourably with the “present commonplace of care” – Novartis’ Cosentyx (Secukinamab), which generated revenues of >$3.7bn within the first 9m of 2022.

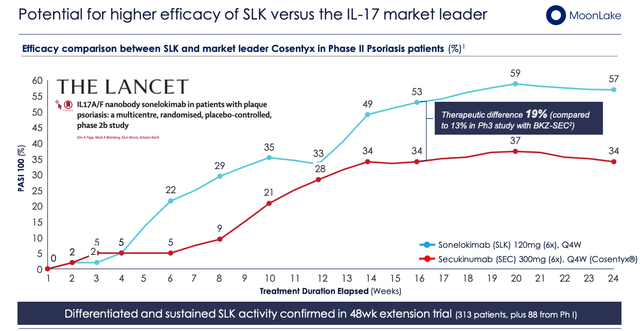

SLK versus “market chief” Cosentyx (MoonLake investor presentation)

As we are able to see above, 57% of sufferers achieved complete pores and skin clearance at week 24 with a security profile “much like the lively management” (Supply: firm Q322 10-Q submission) and the info was revealed within the peer-reviewed and revered journal The Lancet.

SLK is named a “tri-specific” as a result of it may bind to IL-17A and IL-17F, that are often called “dimers”, and likewise to human albumin. In line with MoonLake, and verified by different scientific sources, IL-17A and IL-17F can work together to drive irritation by activation of IL-17RA and RC receptor complexes, creating completely different chains which mix to type complexes that MoonLake believes conventional IL-17 focusing on therapies – comparable to Cosentyx, and IL-17 focusing on candidates developed by Eli Lilly (LLY) and DICE Therapeutics – are unable to deal with.

A further benefit is that MoonLake’s “nanobody” is just one quarter the dimensions of a conventional “antibody”, which means it may doubtlessly goal irritation at a deeper stage, or, as MoonLake itself places it:

Irritation is deep with albumin-rich oedemas and tissue harm siting in deeper, little vascularized tissues, ideally suited for a Nanobody

Illness Goal Choice & Research

MoonLake believes that SLK might be profitable throughout a number of autoimmune circumstances however the firm has chosen Hidradentis Suppurative (“HS”) and Psoriatic Arthritis (“PsA”) as its preliminary targets since IL-17F is considered the “most ample” pro-inflammatory cytokine in these illnesses.

MoonLake notes that the Belgian Pharma UCB (EURONEXT:UCB) has developed the IL-17 inhibitor Bimekizumab – marketed and bought as Bimzelx in Europe to sufferers with average to extreme plaque psoriasis, and pending an approval determination from the FDA in the identical indication within the US – has achieved higher response charges than Humira and Cosentyx in HS.

In PsA, each Bimekuzimab and Izokibep – developed by the Swedish Pharma Affibody and being co-developed with Los Angeles primarily based Acelyrin – have produced examine information suggesting improved inhibition and penetration in comparison with Humira and Cosentyx.

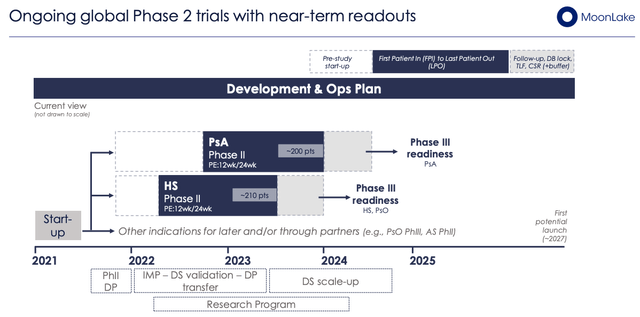

MoonLake has 2 Part 2 research ongoing in PsA (200 sufferers, 60 websites) and HS (210 sufferers, 60 websites), as proven under, which must learn out information this yr, offering an vital near-term catalyst.

MoonLake’s Part 2 research in HS, PsA (Investor Presentation)

MoonLake’s focus is on placebo managed research with an lively reference arm – the reference being Humira – and is hopeful that it may transfer into pivotal research as quickly as virtually potential – supplied the Part 2 information helps it, after all.

Firm Overview & Market Alternative

MoonLake was capable of obtain its Nasdaq itemizing by way of a enterprise mixture / merger with Helix Acquisition Corp, a Particular Objective Acquisition Firm (“SPAC”) headquartered in Boston Massachusetts, and primarily based within the Cayman Islands, and sponsored by healthcare funding firm Cormorant Asset Administration.

The truth that MLTX inventory obtained its itemizing by way of a SPAC will likely be a purple flag for a lot of traders. When itemizing themselves, SPACs haven’t any business operations of their very own – their shares have a par worth of $10, and so they’re granted two years to finish an acquisition or merger, in any other case they need to return funds to traders.

SPACs present a lightweight robust regulatory path to a Nasdaq itemizing, however time constraints could imply the SPAC is unable to discover a appropriate enterprise to merge with, or turn out to be determined and merge with an organization that won’t benefit a list.

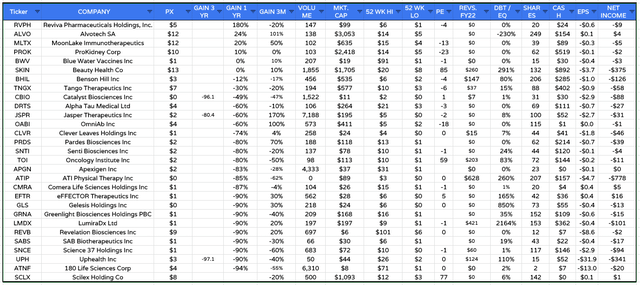

Biotech SPAC listings evaluation (Google Finance / TradingView)

Based mostly on a pattern set of 29 biotech firms (proven above) which have achieved a Nasdaq itemizing by way of a SPAC merger, the common share value efficiency of the merged firms over the previous 12 months is -51%. Solely 4 of those 29 firms commerce larger than their preliminary itemizing value – though MoonLake is one among these.

MoonLake relies in Zug, Switzerland and its founders are Kristian Reich, a scientist who has revealed ~300 papers on mucosal and pores and skin immunology, and Arnaud Ploos Van Amstel, who previously labored at Novartis and helped to launch Cosetyx, in line with an interview given to PharmaPhorum. A 3rd “thriller founder” referred to in that article appears to be Jorge Santos Da Silva who’s now CEO. Van Amstel seems to have now left the corporate.

MoonLake was capable of entry ~$230m money due to the merger with Helix, and in its Q322 incomes press launch, the corporate reported a near-term money place of $88.5m, and a loss earlier than earnings tax of $48m.

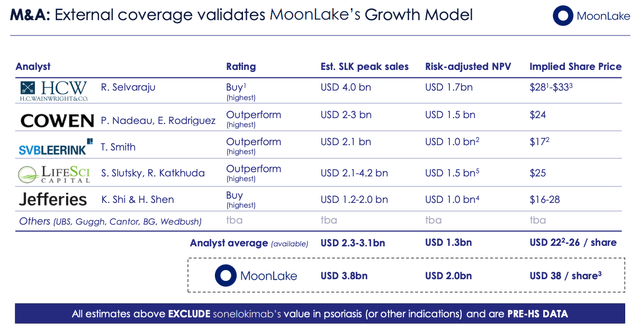

MoonLake investor protection slide (Investor Presentation)

As we are able to see above, MoonLake appears to have attracted the eye of biotech analysts who’ve set what appear to be real looking value targets for a corporation with a promising Part 2 with a validated mechanism of motion that has best-in-class potential property focusing on giant markets.

At this stage, though the height gross sales estimates can be correct if SLK was authorized with a best-in-class profile, they might as properly be disregarded because the do not account for the chance of scientific examine disappointment. Suffice it to say, if SLK strikes right into a Part 3 after acing its Part research, the corporate’s valuation and share value will doubtless soar past $1bn and the share value will acquire by >50%.

Some Dangers To Think about

In my opinion MoonLake represents an funding alternative with a excessive stage of danger. MoonLake has been capable of checklist on the Nasdaq by way of a SPAC deal which suggests it has not been topic to the identical stage of due diligence as an organization that has listed the standard manner, by way of an preliminary public providing.

MoonLake burned by a whole lot of money in 2022 and if it continues to take action it might run out of funding someday in 2024. A slide within the investor presentation proposes 2 paths ahead, one by which the corporate raises additional funds to assist Part 3 trials and commercialisation, and the opposite the place it companions with a “chief in Irritation and Immunology”.

Administration makes it clear it prefers the latter choice however will an I&I chief step up earlier than MoonLake is compelled to take a position once more?

MoonLake has substantial single property danger – if SLK does disappoint within the clinic, there is no such thing as a fall again choice and the enterprise may face being wound up. Though there’s some compelling proof to assist the efficacy and security profile of IL-17 focusing on property, the proof that SLK is best-of-breed is inconclusive to say the least. There isn’t a scarcity of IL-17 candidates, and the failure of Eli Lilly’s candidate owing to liver toxicity could also be not be an anomaly.

Conclusion

A Very Apparent Market Alternative Comes With A Substantial Ingredient Of Danger

MoonLake is arguably working beneath the radar at current – though it has attracted the eye of analysts who’re giving out tender purchase alerts.

IL-17 is an thrilling house – though MoonLake will not be a frontrunner within the subject, with Izokibep in Part 3 research in HS, PsA and a pair of different indications and UCB having already secured approval for Bimekizumab in PsA in Europe, and resubmitted its Biologics Licence Software within the US.

It could come down as to if the benefits of SLK as a “tri-specific nanobody” are as vital as MoonLake administration believes. In equity, Merck retains an curiosity within the candidate – MoonLake will make milestone and funds to the German Pharma because it progress by the clinic and royalty funds if authorized. A growth companion with deep pockets can be invaluable, nonetheless.

The Part 2 examine outcomes strike me as a vital catalyst for MoonLake and so they must arrive this yr – for me the chance of investing in the present day within the hope they’re constructive is just a bit too excessive, however these traders who do make that wager must make a >50% return if outcomes are constructive – as they’ve been in former trials (though not robust sufficient for Merck to carry the drug in-house). With no security web within the occasion of disappointment, nonetheless, it will be clever to not make investments cash you can’t afford to lose.

{kind=link}