Kodak’s story is acquainted as one of many company world’s nice ironies: Kodak went bankrupt in 2012 as a result of rise of digital images after pioneering the expertise years earlier than opponents. In keeping with legend, Kodak worker Steven Sasson invented the self-contained digital digicam in 1975, just for administration to inform him “That’s cute — however don’t inform anybody about it.” But the story of Kodak’s failure is about a lot a couple of shortsighted expertise determination. It’s extra about Kodak’s not understanding that worth evolution would require its enterprise mannequin to evolve accordingly.

To make use of phrases from my current report, Development Requires New Recipes, Not New Components, Kodak failed at each worth seize (rising by extending present markets) and worth creation (rising by increasing to adjoining markets). In flip, this meant Kodak failed at worth conversion (transitioning from seize to creation as circumstances and alternatives demanded and being productive between natural and inorganic progress).

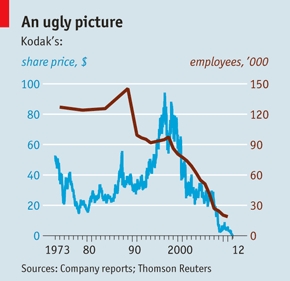

When it comes to worth seize, Kodak failed to increase its core market of images, the place losses began slowly then accelerated quickly. In 1976, Kodak had 90% market share within the US movie market. Within the Eighties, Kodak misplaced floor to its Japanese competitor Fujifilm, which aggressively slashed costs, had a advertising coup by sponsoring the Los Angeles Olympics, and opened a US-based film-production plant. Between 1980 and 2000, Fujifilm tripled its US market share to twenty%. Though Kodak had an preliminary lead within the digital images market, poor pricing fashions and extra opponents comparable to Canon and Nikon introduced Kodak from 27% US market share in 1999 to fifteen% in 2003 and seven% in 2010. Kodak shed its client images enterprise within the chapter two years later.

(Supply: The Wall Avenue Journal, “Kodak Is Dropping Share In U.S. Market to Fuji”)

When it comes to worth creation, Kodak did not broaden to adjoining markets. Within the 2000s, Fujifilm responded to declining images revenues by producing Astalift, a line of skin-care merchandise that used the identical antioxidant expertise it had developed for its photographic movie. In the meantime, Kodak spun off its subsidiary Eastman Chemical right into a separate enterprise in 1994. As we speak, Eastman Chemical has 10 instances the annual income of Kodak. Kodak’s one vital diversification play, the acquisition of Sterling Drug for $5.1 billion in 1988, ended six years later with the piecemeal sale of Sterling’s enterprise models.

(Supply: The Economist, “The final Kodak second?”)

In flip, Kodak did not convert worth between seize and creation as circumstances and alternatives demanded. In different phrases, think about a world the place Kodak had opportunely moved from movie to digital images, utilizing its expertise to widen its market aperture to its well being and industrial imaging companies — and, on the similar time, used its photographic and basic chemical compounds experience to develop prescription drugs and wonder merchandise.

That world didn’t come to go, however maybe some glimpse of it’s nonetheless to return. Perhaps we’re in for a brand new “Kodak second.” In July of 2022, Kodak introduced an funding in Wildcat Discovery Applied sciences to assist develop batteries for electrical autos. In keeping with its press launch, Kodak will “present coating and engineering companies in collaboration with Wildcat to develop and scale movie coating applied sciences that are crucial for the security and reliability of the following era of EV battery expertise. … [This] represents [Kodak’s] continued enlargement of our Superior Supplies & Chemical compounds group as we capitalize on our experience in coating expertise, developed over a long time of movie manufacturing … ”

Higher late than by no means.

This analysis falls below Forrester’s tech insights and econometric analysis (TIER).

{kind=link}