I am love pictures and artwork. That is me.

We have owned CrossAmerica Companions LP (NYSE:CAPL) on and off for years. Like many different energy-related shares, CAPL’s fortunes have waxed and waned during the last decade. At one level, again in Q3 ’17, administration had raised the quarterly distribution 13 straight instances, however then lower it in Q2 2018, to $.525, the place it has remained, together with the newest payout, which went ex-dividend in early February.

Profile

CAPL is a wholesale distributor of motor fuels, comfort retailer operator and proprietor and lessee of actual property used within the retail distribution of motor fuels. CrossAmerica Companions distributes branded and unbranded petroleum for motor automobiles in the US to roughly 1,750 websites situated in 34 states; and owned or leased roughly 1,150 websites. (CAPL web site)

CAPL web site

In 2019, funding entities managed by Founder and present Chairman, Joe Topper, bought 100% of the curiosity in CrossAmerica’s Normal Associate.

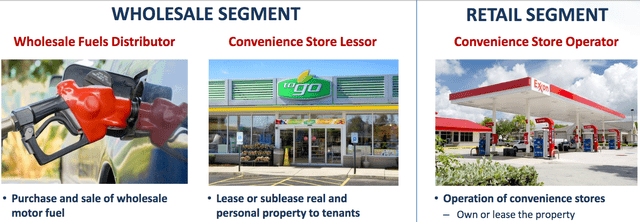

CAPL has 2 foremost segments:

Its Wholesale section has 2 areas of focus – it distributes branded and unbranded motor gasoline to ~1,750 websites situated in 34 states. It supplies gasoline to a number of several types of buyer websites, together with impartial sellers, lessee sellers, CAPL company-operated shops (Retail Section), and fee brokers.

The Wholesale section additionally leases or sub-leases websites used within the retail distribution of motor fuels. These are normally triple-net leases, and are typically for 3-10 12 months phrases. There are ~900 websites producing rental revenue. CAPL owns 60% of those properties.

The Retail section owns or leases comfort retailer operations, C-stores, with ~253 retail websites. CAPL retains all earnings from motor gasoline and comfort retailer operations at these websites.

CAPL web site

Earnings

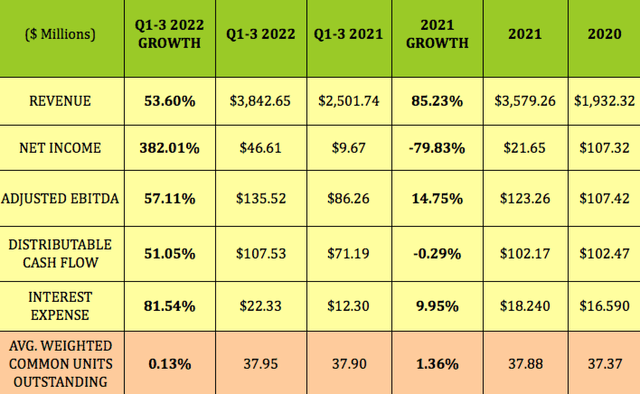

CAPL had a really robust Q3 ’22, throughout which it had 3-digit progress in Working Earnings, Adjusted EBITDA, and DCF. Its Distribution Protection ratio jumped 67%, to 2.55X, vs. 1.53X in Q3 ’21:

CAPL web site

After the pandemic challenges of 2020, CAPL’s income bounced again in 2021, rising 85%, because the US reopened. EBITDA was up almost 15%, whereas Distributable Earnings, DCF, was flat.

Q1-3 2022 had very robust progress, with Income up 53%, Internet Earnings up 382%, EBITDA up 57%, and DCF rose 51%. Like we have seen with most different firms, Curiosity Expense rose considerably, from $12.3M to $22.33M.

CAPL had a $1.2B, (54%) enhance in its wholesale section revenues primarily attributable to a 52% enhance within the common each day spot worth of WTI crude oil to $98.96/barrel for Q1-3 ’22, vs. $65.05/barrel in Q1-3 ’21.

There was an $800M, (84%) enhance in its retail section revenues in Q1-3 ’22, primarily attributable to a 43% enhance within the common retail gasoline worth.

Hidden Dividend Shares Plus

Dividends

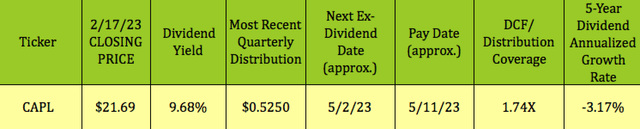

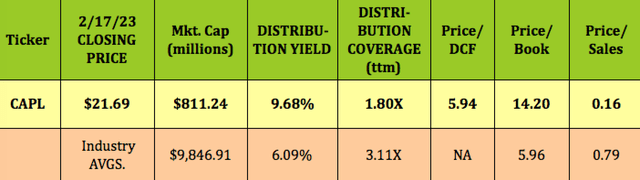

At its 2/17/23 $21.69 closing worth, CAPL yields 9.68%. As famous above, administration has stored the quarterly payout at $.525, after slicing it in Q2 2018, therefore the -3.18% 5-year dividend progress ratio.

Hidden Dividend Shares Plus

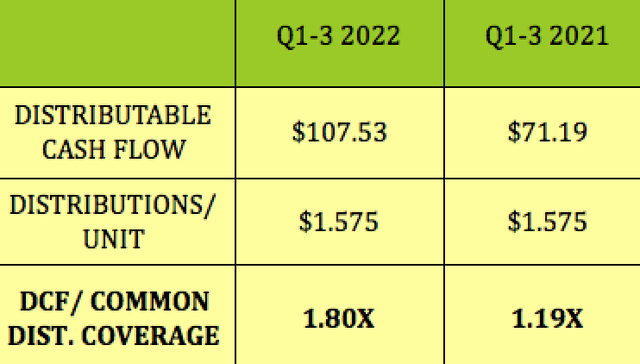

With the large bounce in DCF, and the regular distributions in Q1-3 ’22, CAPL’s Distribution protection issue surged to 1.8X, vs. 1.19X in Q1-3 ’21:

Hidden Dividend Shares Plus

Taxes

CAPL points a Okay-1 tax kind to unit holders.

Profitability & Leverage

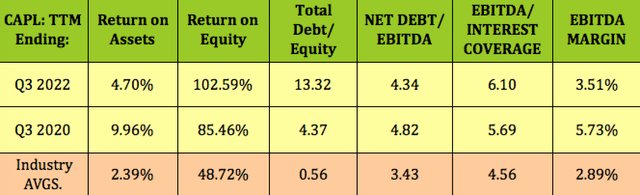

ROA and ROE flip-flopped in Q3 ’22 vs. Q3 ’20, however remained above common. Internet Debt/EBITDA improved to 4.34X, very near administration’s 4.0X to 4.25X Goal Leverage Ratio.

The Fairness base was ~$57M as of 9/30/22, vs. $120M at 9/30/22, therefore the large enhance in Debt/Fairness. EBITDA/Curiosity protection improved to six.1X, larger than common, whereas EBITDA margin decreased to three.5%>

Hidden Dividend Shares Plus

Debt & Liquidity

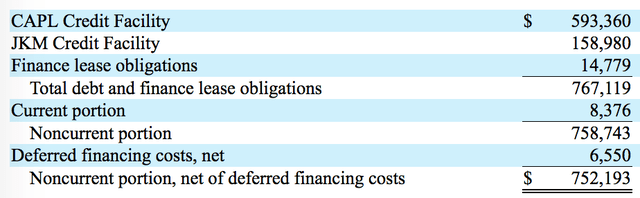

CAPL has a $750M credit score facility, which matures in April 2024, and a $ JKM credit score facility, which matures July 2026. The JKM facility was issued March 2022 to associates of Topper Group and Reilly entities.

Taking the rate of interest swap contracts under consideration, the efficient rate of interest on the CAPL Credit score Facility at September 30, 2022 was 3.9%. The efficient rate of interest on the JKM Credit score Facility at September 30, 2022 was 5.2%.

Whole liquidity as of 9/30/22 was $189.59M, with $163.6M obtainable within the CAPL facility, and $14.2M obtainable within the JKM facility, and $11.79M in Money. Administration diminished CAPL’s whole debt and finance lease obligations by ~$63M in Q1-3 ’22.

CAPL web site

CAPL obtained $24.4M in internet proceeds from the issuance of personal most popular membership pursuits through the 9 months ended September 30, 2022.

Efficiency

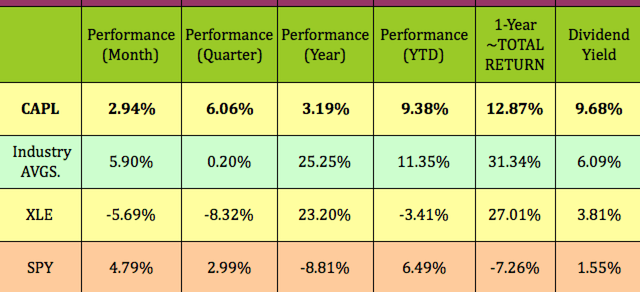

CAPL’s 1-12 months ~whole return outpaced the S&P 500, however lagged its business and the broad Power sector, which had an impressive 12 months. Up to now in 2023, CAPL has outperformed the market and the broad Power sector.

Hidden Dividend Shares Plus

Valuations

Whereas CAPL’s yield, Worth/DCF, and P/Gross sales are all engaging, its P/E-book suffers from the small fairness quantity, i.e. guide worth.

Hidden Dividend Shares Plus

Parting Ideas

At its 2/17/23 $21.69 closing worth, CAPL is ~7% under its 52-week excessive, and 18.4% above its 52-week low. It’s possible you’ll need to look ahead to a worth pullback earlier than nibbling on some models.

All tables furnished by Hidden Dividend Shares Plus, except in any other case famous.

{kind=link}