DNY59

After the bell on Monday, we acquired fiscal fourth quarter outcomes from Zoom Video Communications, Inc. (NASDAQ:ZM). As soon as one of many pandemic’s darlings, the corporate noticed its revenues surge and inventory soar as a major quantity of folks ended up working from house. Since then, nonetheless, the expansion growth has all however ended, and the corporate’s newest report continued to point out lots of the similar troublesome weakening traits.

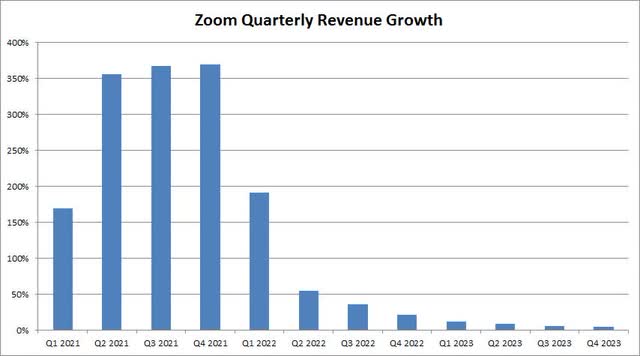

For the ultimate fiscal interval of the yr that led to January 2023, Zoom reported revenues of just about $1.12 billion. Whereas this got here in barely above the road’s common estimate of about $1.10 billion, we should do not forget that expectations had been closely lowered. Only a yr in the past, analysts had been anticipating $1.26 billion for fiscal This autumn. The reported quantity was additionally slightly below what the Road was searching for when steering was offered again on the Q3 report. The 4% income progress reported was the smallest determine for the reason that pandemic, because the chart beneath exhibits.

Zoom Income Progress (Firm Earnings Reviews)

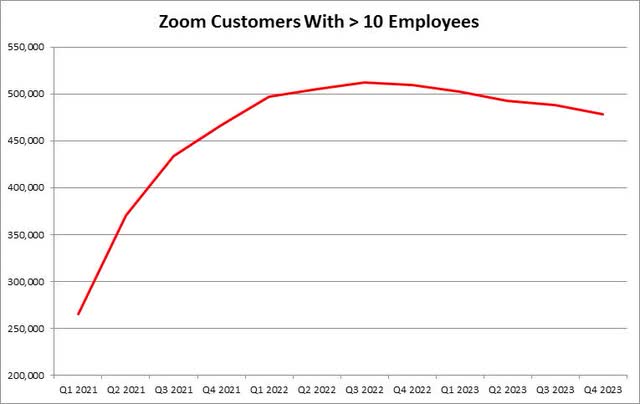

The expansion drawback right here may be very evident. Although the corporate was working off a lot greater base numbers a yr in the past, that hasn’t been the case in lots of latest intervals. The primary subject right here is with reference to prospects with larger than 10 staff. The web greenback growth price right here is right down to 109%, down 20 proportion factors from the place it was a yr earlier and three factors sequentially. This income group made up greater than two-thirds of the corporate’s enterprise at 70% in This autumn, and that proportion is at present growing by the quarter.

Sadly, the variety of prospects that Zoom has with greater than 10 staff is definitely in decline proper now, as you may see within the chart beneath. In fiscal This autumn, Zoom noticed the full variety of these prospects decline by 9,500, the second largest quarterly decline of the fiscal yr. For the fiscal yr, the full loss was 31,300 prospects, which is down about 6%, and losses listed here are beginning to add up. This can be a two-year low for the variety of these prospects.

Prospects With > 10 Staff (Firm Earnings Reviews)

Zoom administration within the press launch talked concerning the variety of prospects offering larger than $100,000 in final twelve month revenues growing by 27%. Whereas that’s true, that proportion progress is the bottom for the reason that begin of the pandemic. The corporate added 746 of those prospects prior to now yr, additionally a brand new multi-year low, and down from 1,081 added a yr earlier. Likewise, the corporate’s remaining efficiency obligations of $3.43 billion, or lower than 30% progress, noticed its lowest yr over yr enhance in each numerical and proportion phrases in fairly a while.

Even within the enterprise section, the numbers usually are not wanting that nice at present. Each the sequential and yearly added buyer numbers had been their weakest in a number of years, with the 22,000 enhance prior to now yr being lower than half of the almost 50,000 that had been added within the earlier fiscal yr. The year-over-year progress price has gone from 35% to 12% in simply twelve months, with the web greenback growth price going from 130% to 115%.

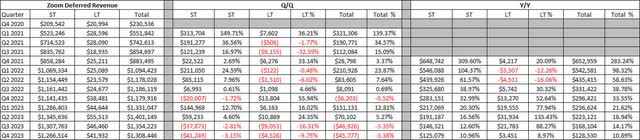

With these key company metrics displaying weakening traits, the numbers are additionally beginning to hit the steadiness sheet a bit. Within the desk beneath, you may see how deferred revenues, an indication of future enterprise, have now declined for the second straight quarter. The quantity of deferred income progress on a year-over-year foundation was lower than 11% on the finish of This autumn, down from greater than 33.5% simply twelve months earlier.

Deferred Income This autumn 2023 (Firm Earnings Reviews)

On account of all these progress points, steering was a bit disappointing. For fiscal Q1, administration is looking for quarterly income of between $1.080 billion and $1.085 billion and income in fixed foreign money is anticipated to be between $1.097 billion and $1.102 billion. Each of those numbers are beneath the road’s common estimate of $1.10 billion, and this means near zero progress over the prior yr interval.

Once more, analyst estimates have come down fairly a bit over the past yr, and income steering was nonetheless low. Non-GAAP EPS steering was a few dime higher than anticipated, however let’s not neglect that the corporate really misplaced over $100 million in This autumn on a GAAP foundation. The adjusted earnings quantity was primarily achieved by including again over $520 million in inventory primarily based compensation and associated payroll taxes. Vital dilution in prior years has lastly began to be offset by a share repurchase plan, however this firm is not producing the large GAAP earnings we noticed lately.

For the total yr, we noticed a really related development. Whole income is anticipated to be between $4.435 billion and $4.455 billion and income in fixed foreign money is anticipated to be between $4.458 billion and $4.478 billion. Sadly, the Road was searching for $4.63 billion, so this forecast is kind of a bit low, even when accounting for international alternate. Likewise, adjusted EPS are anticipated to be about 50 cents higher than anticipated, however income progress stays the issue right here. Non-GAAP working margins are anticipated to point out very minor enchancment yr over yr.

Within the after-hours session, Zoom shares had been up greater than 6%, buying and selling round $78. It seems that buyers are specializing in the This autumn beat of lowered expectations, together with the higher than anticipated non-GAAP EPS steering. Nevertheless, this firm has a significant income drawback right here, and the metrics are getting worse by the quarter. The typical worth goal on the road was $85 going into this report, however simply two years in the past analysts thought this title was price nearly $500, and look the place we at the moment are.

In the long run, the income progress drawback at Zoom is barely getting worse. This autumn outcomes confirmed the bottom proportion enhance for the reason that pandemic began, and plenty of key metrics are displaying weakening traits. It amazes me that main supporters like Cathie Wooden (who was speaking positively about Zoom on CNBC Monday morning) proceed to suppose this title is simply 3 fiscal years away from doing $30 billion in income per yr even in Ark Make investments’s bear case. Zoom is a key holding in each the ARK Innovation ETF (ARKK) and ARK Subsequent Technology ETF (ARKW). Zoom simply guided to lower than $4.5 billion in revenues for the present fiscal yr.

Whereas Zoom Video Communications, Inc. shares did rise within the after-hours session, we might see income declines sooner relatively than later if these present traits proceed. In consequence, I’d not purchase Zoom Video Communications, Inc. inventory after this report except you suppose we’re getting a significant Federal Reserve pivot quickly that may deliver the entire market up. If extra price hikes knock the general market again down within the near-term and Zoom’s prime line does not materially enhance, one might make the argument that new multi-year lows might be in retailer.

{kind=link}