Drazen_/E+ through Getty Photos

Pfizer (NYSE:NYSE:PFE) is among the largest pharmaceutical corporations on this planet, specializing within the growth and manufacture of medicines for the therapy of a variety of illnesses, resembling cardiovascular illnesses, most cancers, and autoimmune illnesses, and a vaccine portfolio for the prevention of influenza, COVID-19 and different viruses.

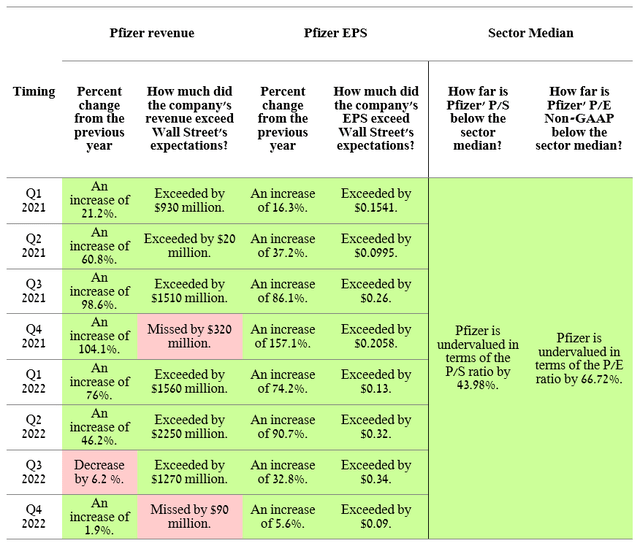

In This fall 2022, the corporate’s income was $24.29 billion, up 1.9% from the final three months of 2021, regardless of a major lower in individuals’s need to vaccinate towards COVID-19. General, Pfizer’s administration achieved the monetary outcomes introduced within the steerage printed within the third quarter, displaying an all-time file in income of $100.33 billion and greater than $31 billion in internet earnings. The corporate’s EBITDA margin of 43.9% for 2022 continues to develop yearly, outperforming trade mastodons resembling Merck (MRK), Novartis (NVS), and Roche Holding (OTCQX:RHHBY) (OTCQX:RHHBF).

Creator’s elaboration, based mostly on Investing.com

This text will current the components that make the corporate a lovely asset for dividend traders and the dangers that anybody contemplating Pfizer as a long-term funding ought to pay attention to.

Conducting an aggressive M&A coverage

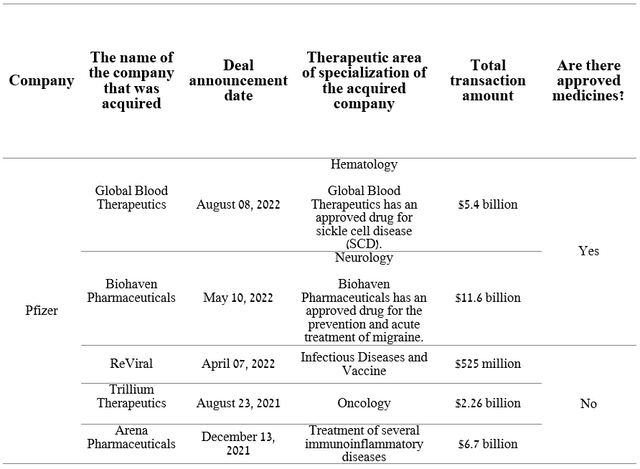

Because the starting of 2021, the corporate’s administration has pursued an aggressive M&A coverage, which has not been noticed for a few years. The explanation for that is the necessity to rejuvenate the drug portfolio earlier than a lot of them lose exclusivity within the coming years. As well as, the multi-billion greenback internet revenue generated from the sale of COVID-19 merchandise permits Pfizer’s Board of Administrators to purchase out corporations whose product candidates have important aggressive benefits when it comes to efficacy and security profile.

Supply: Creator’s elaboration, based mostly on quarterly securities reviews

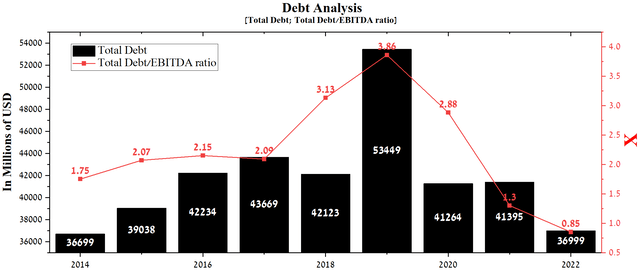

The full quantity spent on acquisitions of the 5 pharmaceutical corporations is $26.485 billion. Regardless of the spectacular quantity, the corporate’s whole debt continues to say no year-on-year and stood at $39,377 million on the finish of 2022. Furthermore, the full debt/EBITDA ratio fell beneath 1x and thus might point out the absence of great monetary dangers related to debt servicing. In consequence, in This fall 2022, Moody’s upgraded Pfizer’s long-term debt score from A2 to A1 and upgraded its long-term debt outlook to steady. Additionally, S&P International Rankings (SPGI) maintains the corporate’s long-term debt outlook as steady from This fall 2020. General, enhancing the credit standing reduces the corporate’s vulnerability to continued Fed tightening and boosts investor confidence in Pfizer as it could meet its debt obligations.

Supply: Creator’s elaboration, based mostly on In search of Alpha

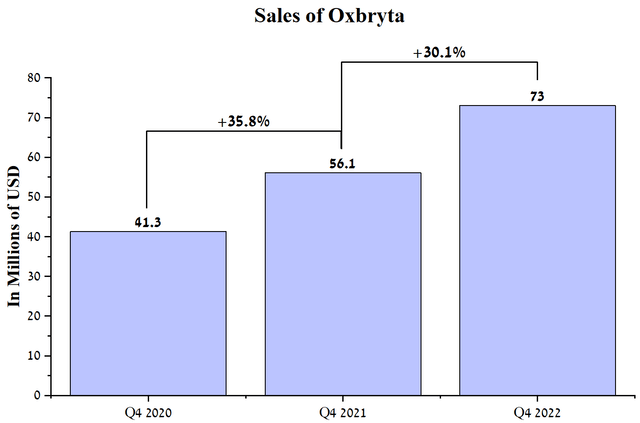

Returning to the dialogue of the offers made, we want to spotlight the $5.4 billion acquisition of International Blood Therapeutics, which has expanded Pfizer’s presence in sickle cell illness. The corporate estimates the mixed peak gross sales of acquired medicines and candidate merchandise may generate over $3 billion. For instance, International Blood Therapeutics has developed Oxbryta (voxelotor), which is permitted within the US, the European Union, and different international locations. The mechanism of motion of this drug relies on reversible binding to hemoglobin (HB) to extend the affinity of oxygen for this metalloprotein. On account of the motion of Oxbryta, the polymerization of Hemoglobin C is prevented, finally resulting in a discount within the crescent of pink blood cells liable for offering oxygen to human tissues and organs.

Supply: Creator’s elaboration, based mostly on quarterly securities reviews

Voxelotor gross sales continued to develop 12 months on 12 months and had been $73 million in This fall 2022. With Pfizer’s huge expertise in uncommon hematology and important monetary capability to allow aggressive advertising, we consider Oxbryta’s CAGR will probably be 25% from 2023 to 2027.

As well as, on October 3, 2022, Pfizer accomplished the $11.6 billion acquisition of Biohaven Pharmaceutical, which provides to one of many leaders within the pharmaceutical trade a portfolio of calcitonin gene-related peptides able to successfully combating migraines that have an effect on greater than a billion individuals yearly worldwide.

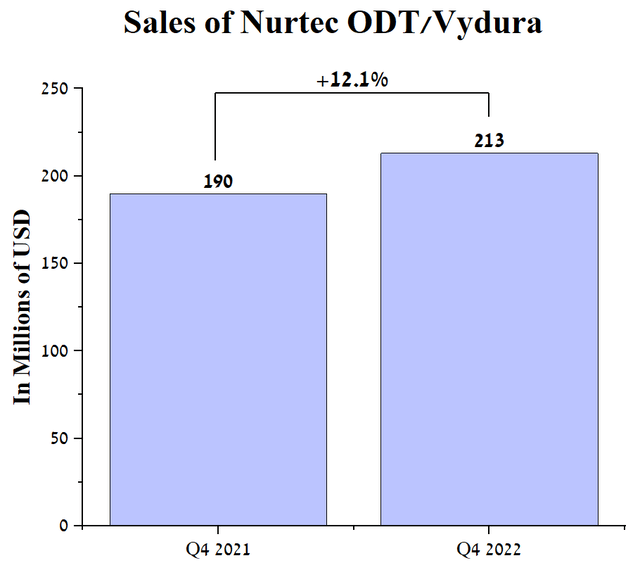

Along with a number of product candidates in scientific trials, Pfizer has acquired Nurtec ODT/Vydura, which is a drugs for the acute therapy of migraine and the preventive therapy of episodic migraine. Nurtec ODT/Vydura gross sales had been $213 million in This fall 2022, up 12.1% year-over-year.

Supply: Creator’s elaboration, based mostly on quarterly securities reviews

Contemplating the colossal migraine therapeutic market, the drug’s excessive efficacy, and the oral route, we estimate that Nurtec ODT/Vydura can have a CAGR of 15% by means of 2027.

Paxlovid is a pacesetter within the COVID-19 therapeutics market

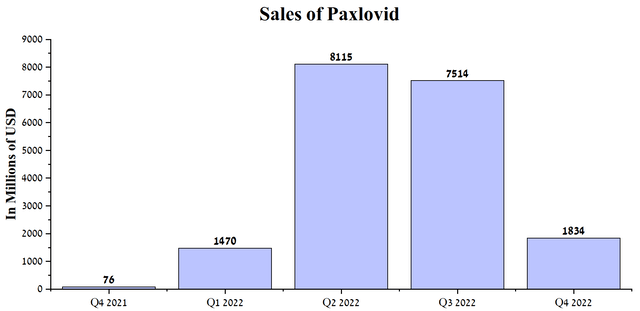

Paxlovid (nirmatrelvir/ritonavir), a drugs that not solely saves the lives of tons of of hundreds of COVID-19 sufferers worldwide however whose gross sales generated 18.9% of Pfizer’s whole income in 2022, performs a vital function within the growth of the corporate. In the mean time, the next monoclonal antibodies as AstraZeneca’s tixagevimab/cilgavimab, Eli Lilly’s bebtelovimab (LLY), GSK/Vir Biotechnology’s sotrovimab (GSK) (VIR), Eli Lilly’s bamlanivimab/etesevimab, REGEN-COV Regeneron’s (REGN) will not be efficient as a therapy and safety towards COVID-19 as a consequence of full or partial resistance to subvariants of Omicron, which finally led to the withdrawal of their emergency use authorizations in america.

In consequence, solely Pfizer’s drugs, Gilead Sciences’ Veklury (GILD), and Merck’s Lagevrio are extensively used as remedies for a illness whose outbreaks are occurring in numerous elements of the world because of the fast mutation of the virus. Paxlovid gross sales amounted to $1,834 million in This fall 2022, displaying a major enhance in comparison with the earlier 12 months. The lower in gross sales of this drugs within the final three months of 2022 in comparison with the earlier quarter was primarily because of the decline within the variety of circumstances of COVID-19 worldwide.

Supply: Creator’s elaboration, based mostly on quarterly securities reviews

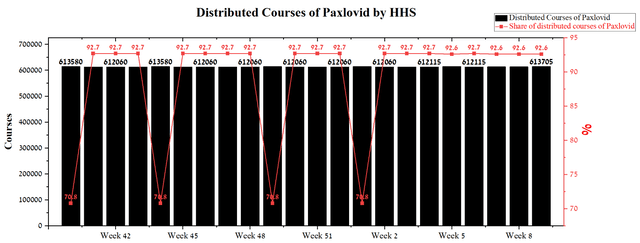

However, within the first two months of the primary quarter of 2023, the variety of circumstances of COVID-19 in america exceeded by 11% in comparison with the primary two months of the fourth quarter of 2022. Contemplating that Paxlovid continues to take care of excessive effectivity within the combat towards new virus variants and its comparatively low worth, these components favorably have an effect on the expansion within the share of nirmatrelvir/ritonavir programs that had been distributed in america by HHS. In latest months, the share of distributed Paxlovid has persistently exceeded 90% and solely often fell to 70.8% as a consequence of AstraZeneca’s tixagevimab/cilgavimab. With AstraZeneca’s drug withdrawn from the market in Q1 2023, we consider there is no such thing as a barrier to Pfizer’s drug persevering with to dominate the multi-billion greenback COVID-19 therapeutics market.

Supply: Creator’s elaboration, based mostly on HHS

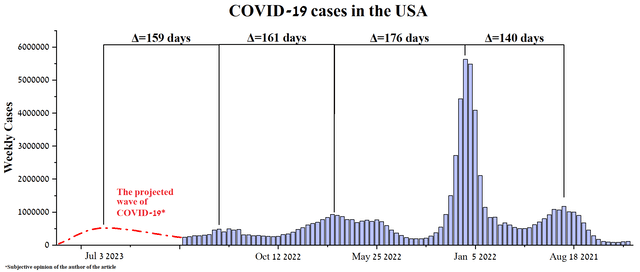

However, after the tip of the wave of coronavirus circumstances in December 2022, when 500,000 sufferers had been registered each week, the scenario is presently stabilizing. We analyzed the expansion and decline traits within the variety of circumstances of COVID-19 over the previous 12 months and a half. We famous that the interval between the peaks of coronavirus waves ranges from 140 days to 176 days, that’s, on common, each 159 days, a brand new wave of incidence begins in america. Consequently, in accordance with our mannequin, a pointy enhance within the variety of circumstances of COVID-19 will happen in June-July 2023, creating further demand for Paxlovid.

Supply: Creator’s elaboration, based mostly on CDC

Pfizer administration predicts that gross sales of this drug will quantity to $8 billion. Nonetheless, we consider that this conservative estimate and our gross sales mannequin for Paxlovid will probably be within the vary of $9.8 billion to $10.5 billion.

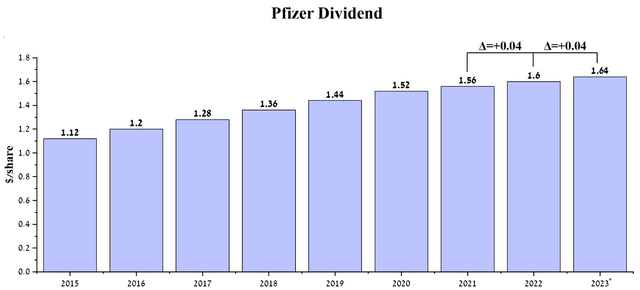

Excessive dividend yield and the share repurchase program

The implementation of an abnormally aggressive M&A and R&D coverage over the previous two years and elevated competitors amongst producers of anti-cancer therapies had a minimal impact on Pfizer’s margins. Consequently, this has contributed to a constant enhance within the firm’s dividend yield over the previous 12 years. On condition that for the first quarter of 2023, dividend funds amounted to $0.41 per share, we consider in sustaining this worth for the remaining three quarters of 2023, and consequently, for the present 12 months, Pfizer traders ought to obtain dividends of $1.64 per share, up 2.5% from a 12 months earlier. As well as, the dividend payout ratio is 24.32%. The comparatively low worth of this monetary indicator demonstrates the opportunity of persevering with the coverage of accelerating dividend funds within the coming years, which, given the present worth of the corporate’s shares of $40.5, is a good looking second for long-term traders.

Supply: Creator’s elaboration, based mostly on In search of Alpha

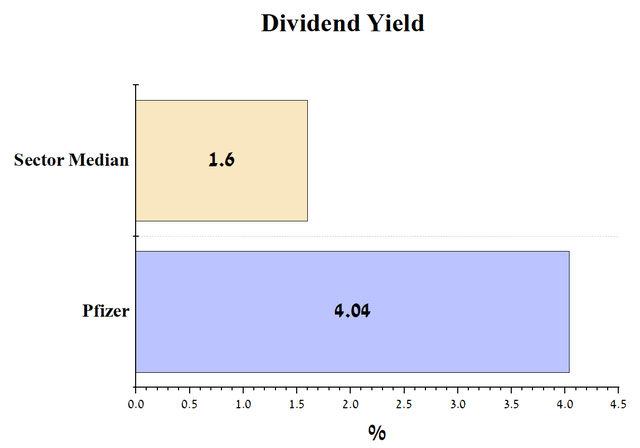

Pfizer’s present dividend yield of 4.04% shouldn’t be solely considerably greater than the biggest pharmaceutical corporations however outperforms different sector leaders resembling Procter & Gamble (PG) and Coca-Cola (KO).

Supply: Creator’s elaboration, based mostly on In search of Alpha

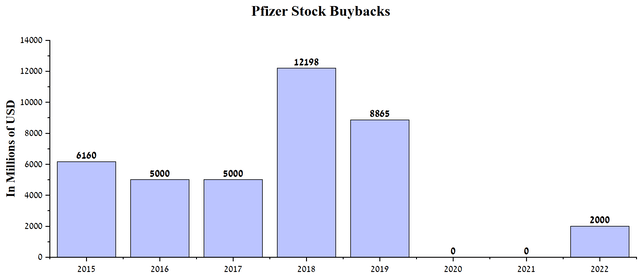

Along with dividends, Pfizer additionally has one of the efficient instruments to enhance the corporate’s funding attractiveness, and it’s the share repurchase program. Nonetheless, Albert Bourla, as CEO of the corporate, has not engaged in an lively share buyback coverage for the reason that onset of COVID-19. One doable cause for this might be the necessity to rejuvenate the portfolio of permitted medicine and to increase the corporate’s presence in therapeutic areas with excessive unmet medical must offset the decline in income from COVID-19 merchandise and people whose exclusivity will finish within the subsequent 5 years. In 2022, Pfizer purchased again two billion {dollars} of shares, breaking a two-year pattern of inactivity.

Supply: Creator’s elaboration, based mostly on quarterly securities reviews

As of December 31, 2022, the remaining quantity underneath Pfizer’s share buyback program was $3.3 billion. Nonetheless, in our estimation, the corporate’s administration is not going to use this cash till the share worth falls beneath $36 per share, which is a powerful help degree when it comes to technical evaluation.

Dangers

Lack of exclusivity of Pfizer merchandise

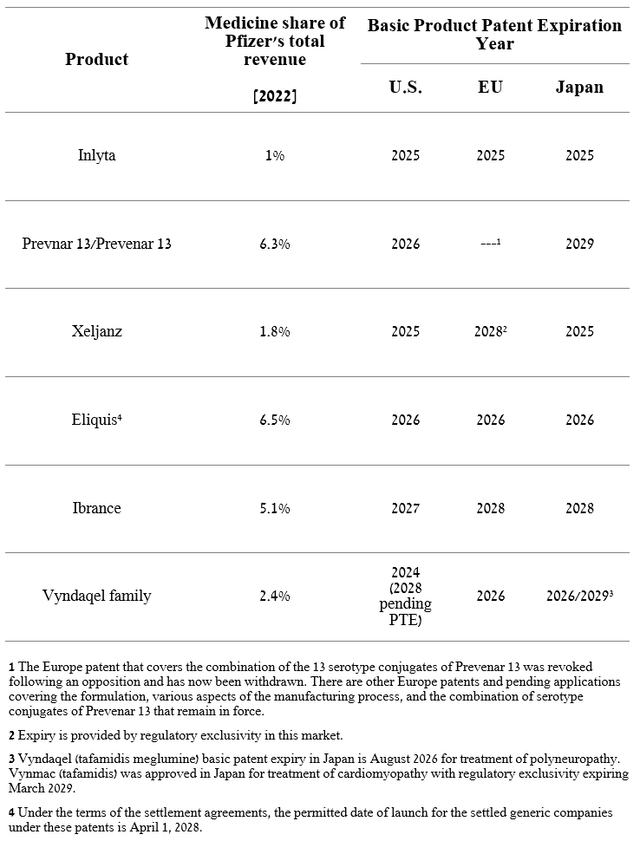

Earlier than discussing the influence of the tip of exclusivity for a number of of Pfizer’s important medicine, it needs to be famous that this refers back to the expiration of patents that shield the unique proper of a pharmaceutical firm to fabricate and subsequently commercialize a branded drug that it owns. In different phrases, when patents expire, pharmaceutical corporations can produce generic variations of the branded drug, resulting in extra competitors and decrease affected person prices as healthcare suppliers search to maneuver sufferers to cheaper generics. However on the similar time, the influence of the lack of exclusivity of a specific drug on the corporate’s monetary place will be totally different and depends upon the share of its gross sales in whole income, the extent of competitors from generic producers, and the presence of next-generation medicines within the firm’s portfolio that may change an out of date product. One in all Pfizer’s methods to mitigate the influence of the lack of exclusivity is to pursue an lively R&D coverage to diversify its product portfolio and enhance income within the firm’s favorable COVID-19 period. The desk beneath highlights the important thing six medicines, whose mixed gross sales account for 23.1% and whose generic variations are anticipated to be in the marketplace earlier than 2028.

Supply: Creator’s elaboration, based mostly on 10-Ok

In the mean time, there’s a lower in gross sales of COVID-19 merchandise and, consequently, stress on the corporate from numerous monetary establishments is rising since it’s not totally clear with what particular medicine Pfizer administration will be capable to offset the lack of exclusivity of such blockbusters as Ibrance, Prevnar 13 / Prevenar 13 and Eliquis, commercialized in partnership with Bristol-Myers Squibb (BMY).

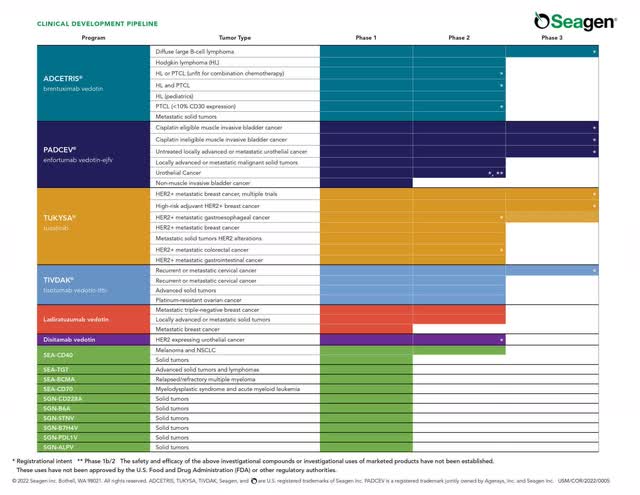

Acquisition of Seagen

In accordance with the Wall Avenue Journal, Pfizer’s administration is in talks to amass Seagen (SGEN) to increase the corporate’s portfolio with promising cancer-fighting medicines. A number of product candidates are in part 3 scientific trials, and consequently, if the first and secondary endpoints are reached, there’s a excessive chance that the FDA and EMA will approve their use, which might dramatically enhance the corporate’s income within the medium time period.

Supply: Seagen Pipeline

As of March 3, 2023, Seagen’s capitalization was $33.86 billion, and provided that the corporate refused to promote itself to Merck for $40 billion, within the present situations, there’s a excessive chance of two outcomes. The primary of those, which we estimate is unlikely, is the acquisition of Seagen’s complete portfolio of medicines for greater than $40 billion to influence the corporate’s administration and key traders to finish the deal. And the second, which is extra doubtless, is the exclusion of Padcev from the settlement to keep away from further investigations from the antitrust authorities and cut back the incidence of a battle with Merck, a associate of Seagen. In accordance with our estimates, if the deal to amass Seagne goes by means of as a part of the second consequence, then its quantity may attain $32-33 billion.

On condition that Seagen continues to be a loss-making firm, its acquisition may negatively have an effect on Pfizer’s EPS within the subsequent 5-6 quarters and cut back its monetary flexibility within the post-COVID-19 period. Furthermore, whole debt may additionally rise above $55 billion because of the have to finance this huge acquisition. In consequence, this may increasingly result in a refusal to extend dividend funds in 2024-2025, which can additionally lower the funding attractiveness of Pfizer on the a part of dividend traders. Consequently, we count on the corporate’s share worth to drop to $36 within the quick time period on this case.

Conclusion

Pfizer is the world’s main pharmaceutical company, based in 1849 and specializing within the manufacture and sale of medicines for the therapy of varied illnesses, together with cardiovascular, oncological, and autoimmune illnesses. The corporate additionally has a group of vaccines that shield towards the flu, COVID-19, and different viruses, which have been very important to reaching file income, working earnings, and different monetary indicators for 2022.

Since 2021, the corporate’s administration has been pursuing an aggressive M&A coverage that has not been seen in a few years, because of the sale of COVID-19 merchandise, which introduced tens of billions of internet earnings to Pfizer in latest quarters. The ensuing earnings are successfully transformed not solely into accelerating their developments but additionally by buying corporations whose medicines have important aggressive benefits over these presently thought of gold requirements in numerous therapeutic areas. As well as, rejuvenating the corporate’s product portfolio reduces the danger of a considerable drop in income because of the lack of exclusivity of a number of blockbusters within the subsequent six years.

Regardless of the excessive dividend yield and margins of the enterprise, and an intensive pipeline of product candidates, long-term traders have to consider the dangers not solely described on this article however the tense scenario round Ukraine and the continued enhance within the Fed rate of interest, which may result in a short-term lower within the firm’s share worth to $36. Nonetheless, regardless of them, we consider Pfizer is considerably undervalued among the many pharmaceutical corporations within the S&P 500 (NYSEARCA:SPY) and might be a superb candidate for dividend traders.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}