zorazhuang

Vitality Switch (NYSE:ET) and Magellan Midstream (NYSE:MMP) are two excessive yield investment-grade midstream MLPs. Though MMP has a greater observe report and a decrease leverage ratio, ET is bigger, extra diversified, and supplies a considerably larger distributable money circulate yield.

On this article, we examine them facet by facet after reporting This fall outcomes and provide our tackle which is a greater purchase in the meanwhile.

Vitality Switch Vs. Magellan Midstream: This fall Outcomes

In 2022, Magellan Midstream Companions elevated its cargo of refined merchandise and crude oil, and it expects this pattern to proceed in 2023. Regardless of this, its This fall web earnings declined to $187M or $0.91/share from $244M or $1.14/share in the identical quarter of the earlier 12 months because of a non-cash impairment cost of $58M associated to the Double Eagle pipeline three way partnership.

Nevertheless, its This fall distributable money circulate improved to $345M from $297M within the prior-year quarter, and free money circulate elevated to $324M from $291M in the identical interval of the earlier 12 months. Moreover, the cargo of refined merchandise elevated to 144.5M barrels from 142M barrels within the year-earlier quarter, and crude oil cargo by way of its wholly-owned property surged to 65.2M barrels from 44.3M within the earlier 12 months.

For the fiscal 12 months 2023, MMP expects to generate DCF of $1.18B, which is 1.38x the quantity wanted to pay money distributions, and free money circulate of $1.07B, or $216M after distributions. The partnership foresees a rise in crude oil transportation quantity on its wholly-owned pipelines in comparison with 2022 ranges, primarily as a result of full-year impression of upper shipments on the Houston distribution system from a current pipeline connection. Magellan additionally assumes that the demand for refined merchandise will stay steady, and refined merchandise shipments are anticipated to rise by roughly 1% in comparison with the report annual quantity transported in 2022. Lastly, refined merchandise tariffs are anticipated to extend by an all-in common of roughly 8% on July 1.

MMP’s administration emphasised prioritizing incremental buybacks over accelerating distribution progress through the earnings name. Though they plan to keep up their 21-year progress streak, administration indicated that rising distributions in step with money circulate progress just isn’t a precedence for them. Administration believes that repurchasing models is a greater use of capital as a result of present undervaluation of models, lack of market pricing credit score for the present excessive yield, and anticipated capital appreciation to be loved from buybacks.

The partnership additionally emphasised that it expects to proceed having fun with robust natural progress in 2023. Whereas it has lowered its capital expenditures in recent times and solely spends $100-$150 million on “enlargement capital” per 12 months, MMP nonetheless expects to develop its distributable money circulate by practically $70 million in 2023. This displays robust natural progress in its current property, which is a distinction to midstream friends that spend aggressively on “progress” initiatives however find yourself seeing little DCF per unit progress. As well as, the partnership plans to extend its refined merchandise charges by an all-in common of roughly 8% on July 1st, which displays the power and aggressive positioning of its property.

ET, in the meantime, achieved a brand new report in quantity throughout all core segments in 2022. In This fall, the online earnings attributable to companions elevated to $1.16B from $926M in the identical quarter of the earlier 12 months. This was accompanied by a rise in adjusted EBITDA to $3.44B from $2.81B, primarily because of larger volumes throughout all core segments in comparison with the earlier 12 months and the acquisition of Allow Midstream. Furthermore, the distributable money circulate for a similar interval was $1.91B, up from $1.6B within the earlier 12 months.

The partnership reported a number of different achievements in This fall, corresponding to a 7% year-over-year enhance in pure fuel liquids fractionation volumes, setting a brand new report. Moreover, the single-day fractionation throughput at Mont Belvieu exceeded 1M barrels for the primary time within the partnership’s historical past. NGL transportation volumes rose to a report 2M bbl/day, up by 5% from the identical interval the earlier 12 months. Moreover, midstream throughput volumes jumped by 32%, setting one other new report. Lastly, This fall NGL exports from the Nederland terminal reached a brand new excessive.

For FY 2023, administration offered steerage for adjusted EBITDA of $12.9B-$13.3B and expects progress capital expenditures of $1.6B-$1.8B and upkeep capital spending of $725M-$775M.

Throughout its post-earnings convention name, ET talked about that it’s taking longer than anticipated to make a remaining funding determination on its Lake Charles LNG challenge because of excessive competitors. Moreover, the partnership acknowledged that it has secured 25%-30% of the required funding to determine on its introduced Warrior pipeline in Texas.

ET administration made clear on the earnings name that it plans to prioritize debt discount and investing in enticing progress initiatives as its prime capital allocation priorities in 2023. This means that there could also be no additional distribution hikes in 2023 however administration signaled that it could very effectively enhance its distribution on an annual foundation sooner or later. Moreover, ET is contemplating issuing a C-Corp forex, which might enable the corporate to supply the very best of each worlds to traders by retaining tax benefits for long-term unitholders and making ET models extra accessible to different traders who’re in any other case averse to proudly owning Okay-1 issuing securities.

Vitality Switch Vs. Magellan Midstream: Enterprise Mannequin

With a extremely diversified portfolio of property, ET is a significant participant within the midstream sector, providing entry to all main U.S. provide basins by means of its interstate and storage enterprise. The partnership’s enterprise worth is over six occasions bigger than that of MMP, which is additional diversified by means of its pure fuel, NGLs, crude, refined merchandise, storage, fractionator, terminal, processing, and treating property. Moreover, ET’s adjusted EBITDA is essentially fee-based, with solely a small share being delicate to commodity costs, offering important money circulate stability. ET’s administration has lowered the corporate’s debt and elevated free money circulate after distributions by lowering capital expenditures and bringing on-line its progress challenge pipeline, giving it an easier and decrease danger enterprise profile shifting ahead.

Whereas boasting a considerably smaller portfolio than ET, MMP makes up for lack of measurement with profitability and consistency. With its well-managed refined merchandise midstream property, MMP has generated spectacular common annualized returns on invested capital of 16% over 15 years. MMP’s money circulate is essentially insulated from commodity value fluctuations, with 85% of its money circulate coming from fee-based contracts, offering stability by means of varied market cycles and power trade circumstances.

General, each of those corporations have wonderful enterprise fashions, however ET holds a bonus because of its bigger measurement and scale, which ought to present extra long-term funding alternatives for progress in addition to decrease publicity danger. Alternatively, MMP’s property are very prime quality and are producing comparatively capital-light robust natural progress. In consequence, MMP is ready to develop its DCF whereas pouring a lot of its retained money circulate into unit repurchases moderately than having to pursue a higher-risk aggressive progress funding agenda.

Vitality Switch Vs. Magellan Midstream: Steadiness Sheet

With investment-grade scores from each Moody’s and S&P, ET is eyeing a potential improve to BBB within the close to future. Its credit standing has a constructive outlook, and the corporate is dedicated to continued deleveraging, having already lowered its debt aggressively over the previous few years. Presently, ET’s leverage ratio is inside its long-term goal, and administration plans to additional cut back debt sooner or later.

MMP maintains a conservative method to capital allocation and steadiness sheet administration with modest leverage and liquidity, and has been promoting non-core property to cut back debt and purchase again widespread models. Its advantageous debt maturity schedule reveals none of its long-term debt matures previous to 2025, with 83% of complete web long-term debt maturing in 2030 or later and the bulk not maturing till 2042 or later, locking in low rates of interest for a few years to return and avoiding detrimental impacts from rising rates of interest.

Each companies look to be in robust monetary form with little danger of monetary misery for the foreseeable future.

Vitality Switch Vs. Magellan Midstream: Distribution Outlook

Trying forward, the present distribution ranges of each corporations seem safe and backed by strong steadiness sheets. Moreover, the administration of each corporations have expressed a want to extend their quarterly distributions on a yearly foundation sooner or later.

Analysts challenge ET will develop its distribution per unit at a 3.3% CAGR by means of 2027, whereas MMP is anticipated to solely make token will increase over that span (0.8% projected CAGR by means of 2027) because it continues to prioritize unit repurchases and steadiness sheet power.

That mentioned, it’s price noting that MMP is anticipated to develop its DCF per unit at a powerful 6.3% CAGR by means of 2027 due to its robust mixture of natural progress by way of tariff hikes in its competitively positioned property and aggressive unit repurchases. In the meantime, ET is simply anticipated to develop its DCF per unit at a 1.5% CAGR over that span.

Vitality Switch Vs. Magellan Midstream: Valuation

Each companies additionally look very attractively priced in comparison with their very own histories. Here’s a side-by-side comparability of them:

ET MMP EV/EBITDA 7.81x 10.66x EV/EBITDA (5-Yr Avg) 8.73x 11.68x P/2023 DCF 4.87x 9.07x Distribution Yield 9.4% 7.8% Click on to enlarge

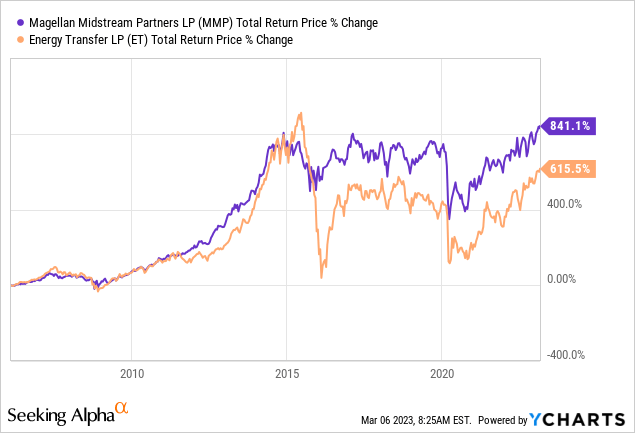

General, ET seems to be vastly cheaper, with a considerably decrease EV/EBITDA and P/DCF multiples together with a meaningfully larger distribution yield. Moreover, it’s anticipated to generate superior distribution per unit progress within the coming years. Alternatively, MMP does have a convincingly superior observe report and is anticipated to generate stronger DCF per unit progress within the coming years.

Investor Takeaway

At Excessive Yield Investor, we have now chosen to personal ET as an alternative of MMP given its superior yield and considerably cheaper valuation. That mentioned, it’s arduous to go improper with both funding at this level as each provide very protected and enticing earnings yields. MMP brings with it a really enticing mixture of progress potential and yield alongside a confirmed administration workforce and enterprise mannequin.

Earlier than buying the models of both enterprise, it is necessary to understand that each situation K1 tax kinds.

{kind=link}