Nils Jacobi/iStock through Getty Photos

Pet humanization is a potent secular development. Through the pandemic, this assertion, which I personally firmly consider in, allowed some traders to hypothesize that pet care equities, with direct or oblique publicity and no matter their sector classification and valuation, are defensive in nature, and that they’d be rising at outsized charges advert infinitum, which is a bit specious, to say the least. This error value them dearly.

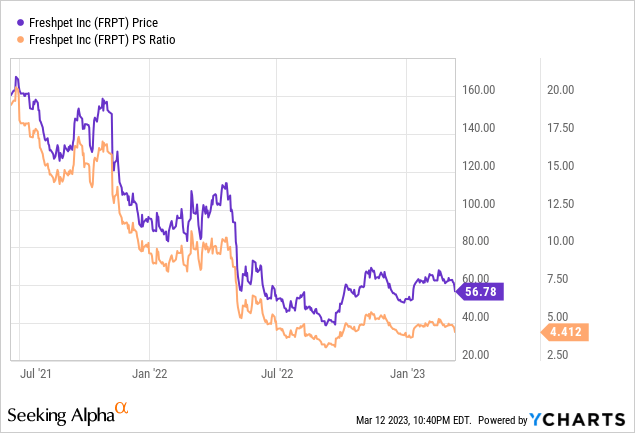

In my 2021 article on the ProShares Pet Care ETF (BATS:PAWZ), I touched upon valuation dangers that surrounded this funding automobile again then. With the pandemic supercharging just a few developments like distant work that, in flip, resulted in rising pet possession, multiples of shares associated to the theme soared, with Freshpet (FRPT) maybe being one of the best instance of a pet meals title that traded with a progress tech-ish valuation, with ~22x Value/Gross sales in Might 2021, a ratio fully disconnected from the fact that since then has shrunk to ~4x as realists prevailed amid inflation and different headwinds.

And as PAWZ was too richly priced again then, I opted for a conservative Maintain score.

And now? Quite a lot of froth has been eliminated, so multiples may need normalized, with pet humanization nonetheless being a development I’ve onerous time believing will disappear any time quickly. Have PAWZ turn out to be a Purchase then? Not precisely. There are a variety of shifting components right here. Let me elaborate on that.

PAWZ portfolio: significant shifts, valuation stays worrisome

The cornerstone of PAWZ’s funding technique is the FactSet Pet Care Index. As talked about on the fund’s web site, the concept is to amalgamate shares “that probably stand to learn from curiosity in, and assets spent on, pet possession.” Importantly, each U.S. and worldwide shares can compete for a spot in it, which provides just a few FX-related dangers to the fund’s technique (within the present iteration, I see the dangers stemming largely from the pound sterling publicity). For extra particulars on the methodology, which is reasonably nuanced, I strongly advocate studying the prospectus which is accessible on the fund’s web site.

Since my June 2021 protection, the PAWZ portfolio has seen thorough recalibration, owing to each additions/deletions and capital appreciation/depreciation of the holdings. Extra particularly, as its market worth has cratered, Freshpet is not amongst its high 5 holdings, with a 4.4% weight vs. virtually 10% beforehand. I additionally seen that 4 shares had been eliminated, together with Tractor Provide Firm (TSCO) and Boqii (BQ). Covetrus, a heavyweight animal well being trade participant working globally, is absent because it was acquired by Clayton, Dubilier & Rice and TPG in 2022. By the identical token, owing to a takeover, the ETF now has no publicity to beforehand Frankfurt-quoted Zooplus. In the meantime, I discovered eight additions (8.5% weight), with probably the most notable being Pet Valu (PET:CA) (OTCPK:PTVLF), a Canadian pet merchandise retailer.

Through the July 2021 – February 2023 interval, PAWZ delivered a detrimental 24.3% compound annual progress price as inflation and FX headwinds conflated to ship share costs of its holdings cratering. It’s not to be ignored that this horrible price is principally the consequence of its 40% decline in 2022. And although the tech-heavy iShares Core S&P 500 ETF (IVV) was additionally down throughout that interval, its detrimental 3.2% CAGR doesn’t look that harrowing.

Portfolio IVV PAWZ Preliminary Steadiness $10,000 $10,000 Last Steadiness $9,471 $6,284 CAGR -3.21% -24.33% Stdev 20.55% 25.69% Finest 12 months 11.73% 7.54% Worst 12 months -18.16% -40.07% Max. Drawdown -23.93% -47.10% Sharpe Ratio -0.14 -1.01 Sortino Ratio -0.19 -1.19 Market Correlation 1 0.9 Click on to enlarge

Created by the writer utilizing information from Portfolio Visualizer

So even with the spectacular 61.7% complete return in 2020, PAWZ, which was incepted in November 2018, is now manner behind IVV (the interval beneath is December 2018 – February 2023).

Portfolio IVV PAWZ Preliminary Steadiness $10,000 $10,000 Last Steadiness $15,459 $13,056 CAGR 10.79% 6.48% Stdev 19.70% 22.79% Finest 12 months 31.25% 61.69% Worst 12 months -18.16% -40.07% Max. Drawdown -23.93% -47.10% Sharpe Ratio 0.55 0.33 Sortino Ratio 0.83 0.5 Market Correlation 1 0.88 Click on to enlarge

Created by the writer utilizing information from Portfolio Visualizer

Clearly, it appears most excesses have been eliminated, with the portfolio now wanting completely different from its pre-bear market model. So is PAWZ an adequately valued play to contemplate now? Hardly. There are just a few points to debate right here.

As ordinary, let me begin with the Quant information. Please take discover that for non-U.S. corporations, I used American Depositary Receipts as a substitute of the abnormal share tickers in my evaluation. One of many examples is Nestlé (OTCPK:NSRGY), a Swiss client staples mammoth; PAWZ holds Zurich-quoted NESN shares, whereas I used NSRGY in my adjusted dataset.

First, over 71% of the holdings has a In search of Alpha Quant score. In that group, 5 gamers have a B- Valuation grade and higher, collectively accounting for ~11.1% of the online property, a reasonably small quantity. A pleasant instance right here is Patterson Firms (PDCO), a dental and animal merchandise distributor with an A grade, which may be defined by its reasonably sluggish progress profile. Once I analyzed the fund the earlier time, ~19% was undervalued.

Subsequent, ~56% (11 shares) are clearly imperfectly priced, with the market anticipating an excessive amount of from them, which is mirrored of their D+ grade and worse. In my view, that is intolerably massive for the present setting as progress premium remains to be a priority owing to uncertainty surrounding the rate of interest query. One instance of a dangerously valued inventory is Zoetis (ZTS), a worldwide chief within the animal well being trade and the fund’s high holding with 11.1% weight.

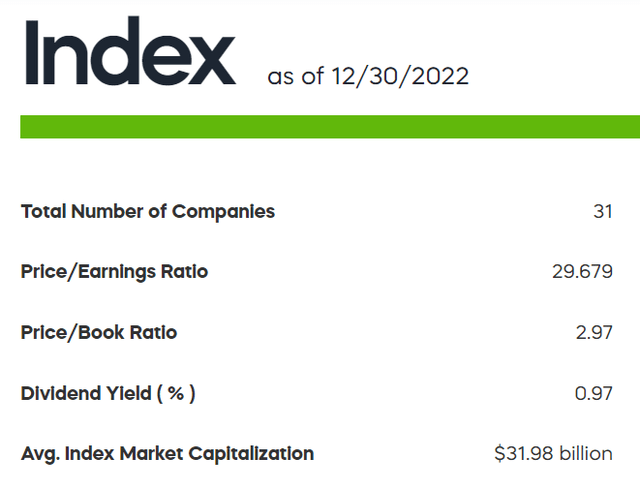

After all, we are able to use conventional multiples taken individually as a substitute of composites. So with the weighted-average market cap of round $46.5 billion, PAWZ has an earnings yield of lower than 2%, as per my calculations. It also needs to be famous that the fund’s web site reveals an index P/E of ~29.7x as of 30 December 2022, which interprets right into a ~3.3% earnings yield.

PAWZ web site; the screenshot taken March 12, Jap Time

Subsequent, Value/Gross sales, which, in line with my computations, stands at ~4x, I consider traders would concur that the margin of security is non-existent right here. That is particularly attention-grabbing because the WA ahead income progress price is barely ~9.4%.

Lastly, we must always not neglect about high quality. One of many points is that about 29% of the businesses within the portfolio are loss-making, whereas greater than 14% are outspending web working money circulation. The ~28.7% distinction between Return on Fairness and Return on Property (solely ~6.6%) factors to the truth that most holdings actively used debt, so ROE is unreliable. The silver lining is that ~51% have a B- Quant Profitability grade and higher.

General, I don’t consider PAWZ’s valuation match its progress and high quality traits.

Investor Takeaway

With pet humanization being a potent, hardly reversible development, traders may contemplate allocating capital to portfolios centered on pet care publicity to reap advantages longer-term.

With that being mentioned, I’m of the opinion that if one is trying to profit from that development, it’s value being exceedingly choosy, continuing with excessive warning, most likely skipping tech-ish performs for extra defensive names like Nestlé, additionally being attentive to valuation and different dangers concerned.

That’s to say, PAWZ isn’t the most suitable choice to contemplate shopping for into at present. A stable deal of froth has been eliminated, little doubt, particularly in relation to FRPT, however the dangers haven’t fully evaporated, and the fund’s earnings yield beneath 2%, as per my calculations, is an ideal illustration. In sum, this ETF is a go.

{kind=link}