primeimages/iStock through Getty Photographs

One arrow

Two arrows

Crimson arrow

Blue arrow

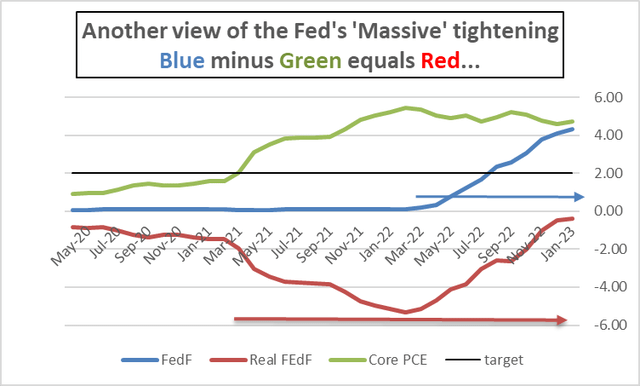

Nominal or actual fed funds? Select properly! (Haver Analytics and FAO Economics)

The chart above comprises the important data to clarify why so many individuals have been anticipating a recession earlier than they need to. That, in flip, explains why the recession is delayed. The recession isn’t delayed as a lot because it was merely anticipated to reach earlier than it might get right here. And that is not shocking as a result of there are such a lot of complicated issues happening within the economic system, together with Fed communication. However as soon as we’re afforded the chance to look again via the rearview mirror, historical past exhibits the event of the pertinent elements that merely make the method appear a lot clearer.

The chart above is about so simple as they arrive. It plots the year-over-year core PCE inflation price, it plots the federal funds price stage, and it plots the true fed funds price stage (which is the federal funds price with the inflation price subtracted from it). The Fed’s 2% goal is delineated by a skinny black line. And I’ve positioned two arrows on the chart. The pink arrow depicts the time when the true fed funds price started getting way more significantly adverse. The blue arrow begins because the Fed begins to tighten coverage and progresses via this nominal tightening course of.

One factor that needs to be instantly evident is that the blue arrow and the pink arrow overlap on the timeline…oops. Every of the occasions they chronicle happens throughout among the identical time durations. This is without doubt one of the essential causes for there being confusion about Fed coverage, what it’s, and when it should take impact.

When will recession come?

The Blue Arrow: For these attempting to pin down the timing of the recession, for probably the most half, there’s been deal with the blue time sequence. The blue time sequence in the course of the interval of the blue arrow that chronicles the Fed elevating rates of interest. Individuals look again at this. That’s now a couple of yr previous, and so they marvel after these extremely robust clustered and targeted will increase within the federal funds price how might the economic system nonetheless be so robust? Wanting on the downside this manner creates confusion.

The Crimson Arrow- However trying on the pink arrow fully redefines the problem. The pink sequence is the true fed funds price. The extent of the nominal federal funds price relative to inflation; that’s its internet worth in actual phrases. This has been the fundamental metric to guage financial coverage for fairly a protracted time frame, extra than simply the time that we present for information again to 1960 – for much longer than that. The pink line says that the time to start ready has not but begun- not begun…

Actual curiosity rates- Economists notice that if you happen to elevate rates of interest to say 10% but when inflation is working at 20% that is not going to be restrictive- however a ten% rate of interest sounds excessive. In actuality, if folks can borrow cash at 10% after which promote items whose costs go up by 20% they’re going to do that each one day lengthy. In fact, that is a extra dramatic instance than what now we have going right here, however that is primarily what now we have had going right here because the inflation price for over a yr continued to maneuver greater and better and has held above the rate of interest – a adverse actual fed funds price.

The true price on this cycle- The pink line measures that hole and that reached its biggest breadth in February at -5.34%. This chart focuses on this present cycle; it doesn’t return to 1960 but when it did you’d see that the 14 lowest month-to-month actual fed funds charges over that broad span lie on this cycle. The rationale that the economic system isn’t going into recession on the schedule that appears to be laid out by the blue arrow is as a result of the blue arrow is trumped by the pink arrow. And as you possibly can see, even with the blue arrow nonetheless transferring ahead and the nominal Fed funds price nonetheless rising the true fed funds price continues to be under zero; meaning it is nonetheless stimulative. The contractive course of has not but BEGUN not to mention reached a degree of biting. Financial coverage has not crossed the Rubicon from stimulus to restriction. For individuals who watch the pink line there may be nonetheless no cause to be counting the time till recession comes. That is an especially vital remark.

Caveat!- Actually, some readers are going suppose… ‘hey wait a minute…’ charges are greater and mortgage charges are loads greater and housing has been blasted. Okay… true sufficient. Housing was in a bubble and piggybacking on tremendous stimulative low financing charges that additionally spurred home costs. With the Fed funds price extra neutrally positioned, mortgages misplaced their low floor and housing affordability has dived consequently. You may take into account this a financial coverage impact (which it’s partly…) however it’s principally a return to extra sane, sober, and sustainable financing charges. The trade does really feel the shock. Auto loans have had among the identical points as some automakers had been providing zero-rate financing earlier than the Fed started transferring charges up.

Political strain…to do the WRONG thing- The Fed Chairman had simply gotten completed testifying earlier than the Home and Senate monetary/banking committees and earlier than every of those committees he obtained some very aggressive and hostile questioning from Democrat members of the committees about how aggressive the Fed price hikes have been. Elizabeth Warren, who really is aware of higher and understands economics, pointedly requested Mr. Powell how many individuals he supposed to place out of labor in his pursuit to scale back inflation. Consultant Pressley adopted that line of considering when the testimony moved from the Senate Banking Committee to the Home Monetary Companies committee. However as our charts present the Fed isn’t even on a path of restrictiveness but. Nonetheless, the political strain has welled up and is sort of intense. Not surprisingly political figures are wedded to nominal figures slightly than taking a look at metrics that modify for the consequences of inflation.

Bought lags?- I’ve been arguing that if financial coverage works with a lag then we’d count on there to be a lag when the Fed runs a really stimulative coverage in addition to when it runs a program of coverage tightening. Take a look at the blue arrow, take a look at the pink arrow. We’re nonetheless in a interval by which financial coverage is stimulative now we have not but began the clock on Fed coverage being restrictive – besides in sectors that had gotten out too far over their very own skis within the low-rate interval…The lags from the stimulative coverage are nonetheless in power.

Does Cash matter? In that case What’s-a-matter?

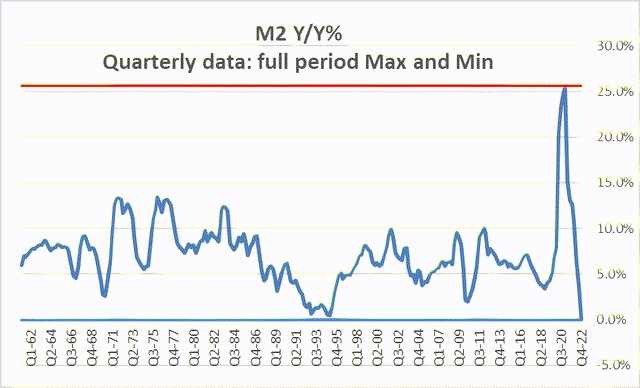

There’s one other matter we will take a look at that provides some perception on this: that’s the progress price of cash provide, M2. You see that on the chart under.

Financial conduct has grow to be excessive!! (Haver Analytics and FAO Economics)

This can be a quarterly chart that appears at year-over-year progress in M2. I’ve highlighted this chart by plotting the complete pattern most and minimal progress charges with the utmost represented by a pink line and the minimal represented by a blue line. As soon as once more, curiously, each the utmost and the minimal draw from our present cycle! Simply as we noticed earlier, the 14 lowest actual fed funds charges have occurred on this cycle. Now we uncover that the strongest M2 cash progress has occurred on this interval as effectively. And the strongest cash progress is separated by seven quarters from the weakest cash provide progress that we have had over this complete interval stretching again to the early Nineteen Sixties. How about that! So are we beneath the spell of extra growth or of document contraction?

So simply as we noticed with actual and nominal rates of interest we see with cash progress; cash progress has gone from an enormous growth to an enormous bust. The sharp slowdown of cash progress is cause sufficient to fret whether or not the economic system is headed for recession. On month-to-month information we’re trying on the first year-over-year decline within the cash inventory since a minimum of the Nineteen Sixties and definitely additional again than that. However what in regards to the influence of the growth?

We are able to discuss in regards to the lags in financial coverage in numerous methods; we will take a look at actual rates of interest and discuss in regards to the lags; we will take a look at cash progress and discuss in regards to the lags. It needs to be clear from our chart on cash progress that the lags from the growth are going to begin to overlap with the lags from the bust. And that is going to make it very troublesome to pin down how these lags are going to have an effect on the economic system and when they’ll trigger recession to happen.

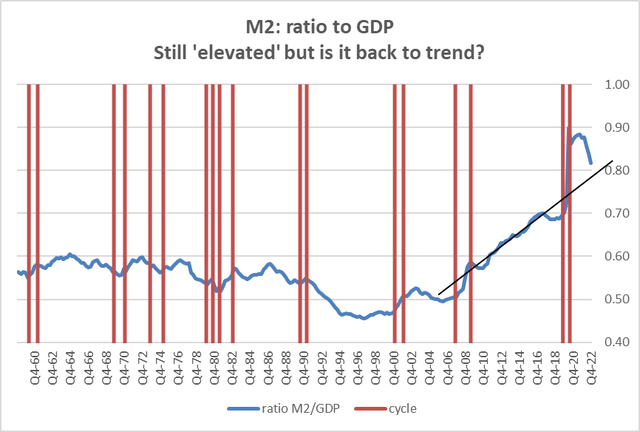

To grasp these forces a bit bit higher I’ve plotted the ratio of M2 to GDP on the chart under. What it exhibits is that there was a pointy run up within the progress of cash in comparison with the expansion of GDP. A few of you might acknowledge this as a flipped over chart of financial velocity; that is right. What I wish to discover with this chart is the query of the place is cash provide relative to GDP? Placing issues in progress price phrases, what we see is an extreme burst of cash progress after which a shocking decline within the progress price to abject quarterly flatness. The query is as soon as we observe that path the place are we with cash progress on stability? For instance the growth comes after a interval that was in any other case comparatively regular though we see on the chart that the ratio of cash to the GDP had really been rising for a while. However the interval of the bust in cash progress will not be fairly the identical as different durations when cash provide went via a bust as a result of we’re getting a bust after a growth which means that that is ‘simply’ the growth unwinding. So possibly slightly than being a bust it is an un-boom? (if you happen to’ll allow me to torture the English language a bit bit).

M2 relative to pattern (Haver Analytics and FAO Economics)

The chart means that the present bust in cash progress hasn’t fairly introduced us again all the way down to the previous rising pattern after we skilled the growth however clearly we’re nearer to being on pattern. So if cash progress went via this horrible perturbation does that matter if we wind up again at pattern? I believe the reply to that is ‘sure’ and I believe most economists could be fairly upset with the growth and the bust conduct of cash inventory on this cycle. On the identical time I additionally suppose that the bust coming after the growth imbues the bust with a unique character than if it occurred by itself with out being preceded by a growth.

In the long run…

In the long run, curiously, we get the identical indicators from cash provide that we get from actual rates of interest. Actual rates of interest have gone via their gyrations however proper now they’re really again close to impartial. Cash provide progress has boomed and busted however now it is mainly again on (or near) its pattern, a minimum of its pattern ratio to GDP.

Thus far all of this has been a dialogue and an outline of how financial coverage has behaved both taking a look at rates of interest actual rates of interest or cash provide progress or the ratio of cash the GDP and I actually have not stated something about inflation itself. However, after all, now we have inflation. And inflation clearly has an vital worldwide and geopolitical element. We see the battle happening between Russia and Ukraine we see inflation excessive around the globe – even Japan has managed to have some inflation after a protracted interval of not with the ability to have any in any respect. And whereas we all know financial coverage has been extreme and stoked inflation together with fiscal coverage, the inflation price in the US does not look like out of line with the inflation that we’re seeing in different main developed international locations. In Europe inflation is worse…

Does the worldwide nature of inflation trump home mismanagement?

That is the explanation why some Democrats have grow to be so hostile in opposition to the Fed Chair, arguing that inflation is actually an exogenous occasion as a result of it is occurred each place and which you could’t blame Joe Biden and his fiscal coverage for it – or Donald Trump’s fiscal coverage earlier than that. They argue that since financial coverage did not trigger inflation leaning on financial coverage to resolve the issue isn’t going to be the correct resolution. And whereas that makes for a pleasant sound chunk it is not logically or economically right.

In the course of the first oil shock within the early Seventies we had a worldwide inflation and the US managed the state of affairs very badly whereas West Germany managed it fairly effectively. Even when there is a world inflation shock home coverage can both act to blunt it, ignore it, or exaggerate it. One clear function of financial coverage on this state of affairs is to maintain the inflation that’s too excessive from changing into a part of a wage value spiral and making the inflation course of worse.

A current paper delivered at a College of Chicago Sales space Enterprise College convention in New York concluded that the Federal Reserve had by no means contained and diminished a considerable inflation price with out the economic system experiencing recession. That paper joins the idea of the Fed controlling inflation, elevating rates of interest, and recession in a tidy however uncomfortable bundle. Underneath strain in his testimony final week Fed Chair Powell reassured everybody that the Fed’s objective is to not create recession. However the Fed’s objective is to chill mixture demand and one side-effect of cooling mixture demand is creating unemployment and whenever you cool mixture demand and create an employment the chances are high that you create recession…however it’s not the target.

The state of coverage artwork

So that is the state of know-how for economics. Coverage slows mixture demand and that brings provide and demand again into stability and it reduces the inflation price, nevertheless, the facet impact is that it creates unemployment and the economic system seemingly falls into recession. In fact, there are some lacking elements right here… trendy central bankers additionally imagine in credibility and expectations, considering if central bankers can set these proper they will push via to success. What’s unclear in taking a look at historical past is whether or not it is doable for the Fed to lift charges and to damp mixture demand to manage inflation however not a lot that it creates substantial unemployment and recession. Can setting expectations resolve that dilemma? I am positive that somebody can fiddle with an econometric mannequin and present that it may be completed, however the true query is whether or not it may be completed by mortal people working coverage in actual time. I am skeptical of that.

On the finish of 2021 I used to be writing in regards to the inevitability of recession. There have been no explicit financial statistics that had gone off the crushed monitor just like the main financial index or something like that. I used to be merely observing some extraordinary relationships that had been coexisting in markets. They did not appear cheap to me and steered that they might solely be introduced again into alignment by having a recession. The primary three issues that I noticed had been (1) that the Fed funds price was extraordinarily low, (2) the inflation price had risen extraordinarily excessive, and (3) the 10-year notice yield appeared nonetheless to be snug and low at round 3% effectively under the tempo of inflation. I might in all probability be happy with any two of these traits, however not with all three of them collectively. And I doubted that expectations actually defined that conduct and – in the event that they did – I doubted that they had been accurately set.

I started considering that there was going to should be some sort of a major change in coverage to get management of inflation that the bond market didn’t appear to understand. For a very long time, the Fed didn’t recognize it both, because the Fed continued to push out forecasts that had minor will increase within the federal funds price and had inflation coming down all by itself with out a lot Fed motion. This led me to model the fed funds price as ‘the magic fed funds price.’ A type of financial counterpart to the neutron bomb that killed folks however left buildings intact. The Fed’s new weapon killed inflation leaving unemployment intact. What was I doing when the Fed found this?? Apparently, I used to be not consuming sufficient…

Now we see occasions shifting.

The main indicators are forecasting a major slowdown or recession within the economic system. The yield curve is now deeply inverted forecasting what some say can be a extra treacherous recession than what’s being anticipated. Job progress, nevertheless, has been a lot stronger than we imagined. Even so lots of people have left the labor market and the market is tight and the stop price is excessive and wages proceed to rise although actual wages proceed to be eroded. Right here we see the influence of ongoing financial stimulus.

Recession ho!

I nonetheless have little question that recession is coming. Nevertheless, I believe it’s extremely arduous to pin down the date due to the issues that I outlined above. And I believe a part of it’s due to Fed communication. The Fed continues, maybe for political causes, however it continues to speak about soft-landings. And, the place we will measure inflation expectations even out to 5 years, they look like comparatively effectively behaved for probably the most half. That has inspired the Fed to suppose that it is nonetheless in management and doing a superb job. However is {that a} dependable metric? As little as they’re, inflation expectations are nonetheless amongst among the highest values now we have seen in recent times…So beware the way you interpret them.

Since 2015 there’s little or no the Fed has completed that I’d take into account to be a ‘good job.’ Its ‘bygones’ coverage begun in 2015 was a mistake. Its adoption of a brand new pro-labor working framework was a catastrophe. I believe that’s the place the Fed started to get itself into actual deep hassle by claiming that it will emphasize management and ship full employment within the brief run, along with value stability. Maybe financial coverage has realized its lesson that the Financial Authority cannot have its cake and eat it too. However then I believed we knew that years in the past. Sigh!

{kind=link}