aluxum

The iShares J.P. Morgan USD Rising Markets Bond ETF (NASDAQ:EMB) seeks to trace the funding outcomes of an index composed of US dollar-denominated rising market bonds. The ETF provides a median yield to maturity of seven.4%, reflecting elevated UST yields and above common credit score spreads. With financial coverage shifting into easing mode, the EMB seems set to profit from decrease UST yields and narrower credit score spreads within the close to time period, which ought to enable the ETF to generate 20%+ returns over the following 2 years.

The EMB ETF

The iShares J.P. Morgan USD Rising Markets Bond ETF seeks to trace the funding outcomes of an index composed of US dollar-denominated, rising market authorities and government-backed bonds. EMB holds bonds of governments with greater than USD1bn excellent and no less than two years remaining in maturity. The most important issuer within the ETF is Mexico, with a 5.9% weighting, adopted by Saudi Arabia, Indonesia, and Turkey, which all have weighing of over 5%. By way of credit score high quality, simply over half of the issuers are funding grade, whereas the typical maturity is 12.4 years. Regardless of the excessive maturity, period is comparatively low at 7.3 years, with a lot of the volatility within the ETF coming from credit score danger. The EMB tends to maneuver extra carefully according to rising market shares than it does with US Treasuries as credit score spreads are the dominant short-term driver of returns. The fund costs an expense price of 0.39% which is comparatively excessive for a bond fund however remains to be low in comparison with the present yield to maturity of seven.4%.

11% Annual Returns Probably

I final wrote concerning the EMB in early January, arguing that bettering credit score danger and decrease bond yields would set off a breakout within the index. Since then, whereas 10-year UST yields have moved barely decrease, EM credit score spreads have widened, inflicting the EMB’s common yield to maturity to rise. On the similar time, breakeven inflation expectations have additionally fallen, and sit at simply 2.1%. Because of this, the anticipated actual yield on provide on the EMB has risen to five.3%.

This enhance in the actual yield has occurred regardless of an aggressive shift in Fed coverage expectations. Over the previous two weeks December Fed funds futures have fallen 140bps, with the Fed now anticipated to decrease charges by the tip of the yr. Not solely has this strengthened the case for US Treasuries, it additionally seems to have stabilized danger urge for food within the close to time period, with rate of interest delicate sectors like Know-how seeing a restoration according to decrease bond yields, and the greenback resuming its weakening development. As Fed tightening has been a significant driver of rising EM credit score spreads over the previous yr, there may be important scope for narrowing because the Fed’s coverage reversal helps liquidity and eases default issues.

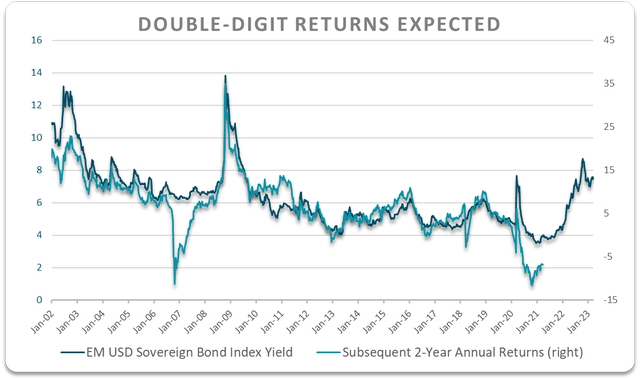

If we take a look at historic returns on EM USD Sovereign bonds versus the prevailing yield on the index, the correlation over the previous 20 years suggests present yields are in line with annual returns of 11% over the following 2 years. The two-year underperformance of the EMB relative to what would have been anticipated primarily based on the yield displays the truth that yields have risen sharply over this era, which recommend future returns might be even stronger as has been the case up to now.

Bloomberg, Writer’s Calculations

From a longer-term perspective, there may be a fair nearer correlation between the yield on EM bonds and whole subsequent returns as one would anticipate, with the present yield in line with annual returns of round 7-8%. Curiously, EM USD Sovereign bonds have truly misplaced cash over the previous 5 years for the primary time on document going again 30 years. Earlier durations of great underperformance relative to return expectations have given strategy to durations of subsequent outperformance.

Bloomberg, Writer’s calculations

World Recession A Threat, However EMB A Nice Threat-Reward Play

The principle danger is that Fed easing measures fail to stabilize liquidity and danger urge for food and the continued development of declining international financial exercise accelerates. As we noticed when the EMB misplaced 33% decline through the international monetary disaster, rising credit score spreads could cause important losses within the ETF even when UST yields head decrease. Nonetheless, the risk-reward outlook for the EMB is more and more compelling as actual yields transfer greater and rate of interest outlook strikes decrease. The 7.4% yield on the EMB is ample reward for the chance of a spike in credit score spreads, significantly with 10-year inflation expectations simply above 2%. I anticipate to see returns of over 20% over the following 2 years within the EMB as yields transfer decrease according to decrease UST yields.

{kind=link}