In response to the demand for quicker and extra handy cost choices, the Federal Reserve has launched a plan to modernize the US cost system, together with the implementation of real-time funds.

The thought for this modern cost service has been within the works for over a decade. Its implementation is anticipated to revolutionize the banking business by offering prospects with a extra environment friendly and seamless cost expertise.

FedNow is anticipated to revolutionize the best way transactions are carried out within the US, making it simpler and faster for companies and people to switch funds.

However, what’s the new Federal Reserve Cost System, how will it have an effect on the Fintech business, who can take part within the FedNow Pilot program, and when will FedNow be accessible? These questions and extra might be answered by our Finance professional on this useful

information.

A Temporary Background on US Cost Methods

America has been utilizing the Automated Clearing Home (ACH) for nearly 50 years to switch cash between financial institution accounts. Nevertheless, ACH transactions can take as much as two enterprise days to finish, inflicting inconvenience for patrons who require quicker

funds. In distinction, different international locations have adopted immediate companies and real-time funds (RTP), permitting for instantaneous transfers.

The Federal Reserve is now spearheading change with the launch of FedNow real-time funds, which might permit home US funds to be processed 24/7 and all 12 months spherical with speedy settlement and immediate funds availability. Actual-time funds are a

main step in the direction of modernizing the US cost system, bringing it consistent with different superior economies.

RTPs make funds frictionless for patrons, guaranteeing they’ve pace in funds, immediate monetary and settlements, and easy accessibility to their cash each time they want it.

The implementation of cost rails will assist higher end-to-end communication and make enterprise processes and communication round funds way more environment friendly.

The FedNow cost system is a big enchancment over the standard ACH system, providing quicker, extra handy cost options that profit each people and companies.

What’s FedNow?

FedNow, the Federal Reserve’s cost system, will facilitate real-time transactions for monetary establishments of any measurement, 24 hours a day, three hundred and sixty five days a 12 months.

By using clearing capabilities, banks can immediately trade the required info to debit or credit score their prospects’ accounts throughout cost settlements. Plus, with the implementation of FedNow, banks can now present higher notifications to their end-users

relating to cost acceptance or failure.

In distinction to RTP, FedNow will service all federal reserve banks by way of the FedLine community, offering cost and knowledge companies, together with safe digital messaging methods and IP-based options, to over 10,000 monetary establishments.

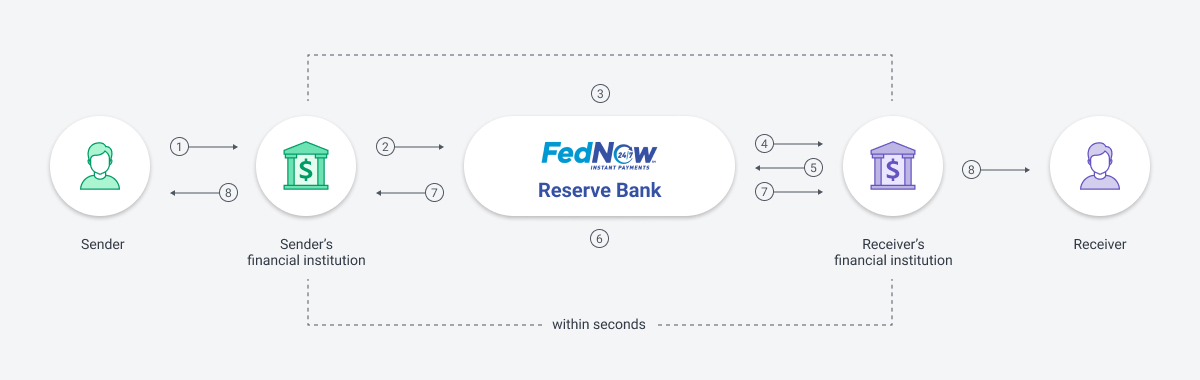

How Will FedNow Work?

To make sure the effectiveness of real-time cost methods, simplicity for customers and sturdy safety measures are essential elements.

Customers of the FedNow Service are unlikely to note any important variations from different real-time cost methods. They are going to proceed to log in to their checking account to provoke funds, and monetary establishments will proceed to supply safety measures,

display screen funds, and handle account modifications and reconciliations.

Nevertheless, the first distinction with FedNow is the cost switch course of between monetary establishments. FedNow will act as an middleman between the sender’s and receiver’s monetary establishments, validating cost messages, and debiting and crediting

the suitable accounts, all inside seconds.

I might examine the direct entry to prospects’ accounts supplied by the FedNow Service to a “good contract on the blockchain,” as it should allow smoother and faster transactions between members. Nevertheless, the elevated management and centralization of the

system could lead to increased prices for customers.

Whereas the FedNow service is designed to keep up excessive ranges of safety, the necessity for elevated safety measures can also be attributed to the prices of utilizing the system.

FedNow has been designed to function alongside different real-time cost methods and can make the most of the ISO 20022 commonplace. Initially, it should solely cowl home funds.

What’s ISO 20022?

ISO 20022 is a globally acknowledged cost messaging commonplace that gives richer and extra structured knowledge throughout the cost course of.

In comparison with different requirements, ISO 20022 permits for about 10 instances extra knowledge to be despatched per cost. This extra knowledge could embrace details about the cost’s objective, supply, and supreme beneficiary. This enhances the cost system’s knowledge construction,

creating a standard language and mannequin for cost knowledge worldwide.

Nevertheless, constructing a brand new real-time product that meets all these necessities is complicated because it entails modernizing legacy methods. The US adoption of ISO 20022 has introduced extra deal with messaging and knowledge for real-time funds inside a world monetary

framework.

What’s the FedNow Launch Date?

In mid-March, the Federal Reserve has revealed that the FedNow Service is ready to begin its operations in July. In April, the Federal Reserve will welcome those that want to be early adopters to provoke a buyer testing and certification program.

Who Can Use FedNow?

FedNow might be accessible to each people and companies. For the preliminary launch, the Federal Reserve intends to set a transaction restrict of $25,000. Because of this cover, small companies and retail funds made by people will profit extra from

FedNow till the Federal Reserve will increase the transaction restrict.

Ranging from the primary week of April, the Federal Reserve will provoke a proper certification course of for collaborating banks who want to use the service. Early adopters will undertake a buyer testing and certification program, which might be guided

by suggestions acquired from the FedNow Pilot Program, to arrange for reside transactions through the system.

The FedNow Pilot Program concerned over 100 members from totally different credit score unions and depository establishments. In June, the Federal Reserve and authorized members will conduct manufacturing validation actions to make sure that they’re absolutely ready

for the July launch.

As soon as monetary establishments take part within the FedNow Service, each companies and people will have the ability to ship and obtain immediate funds at any time of day, and the recipients could have full entry to the funds instantly.

What are the Advantages of FedNow Funds?

The Federal Reserve’s initiative to modernize the cost system is anticipated to convey quite a few advantages, together with larger effectivity, decrease prices, elevated competitors, and improved buyer expertise. It is usually prone to encourage innovation within the

cost business, resulting in the event of recent cost companies and merchandise.

The usage of FedNow in wire transfers between banks as an middleman can enhance charges of transactions. Regardless of these prices, the usage of intermediaries in financial institution transactions can enhance the method of Anti-Cash Laundering (AML) and Workplace of Overseas Belongings

Management (OFAC) checking.

For instance, FedNow can play a job in guaranteeing compliance with AML and OFAC laws by conducting due diligence on the events concerned in transactions and reviewing the transactions for any suspicious exercise.

The advantages of immediate funds aren’t restricted to fintech corporations and banks. The elimination of chargeback dangers that retailers at the moment face may result in larger consumer satisfaction, and immediate funds may make banking and cost processing extra

accessible to underbanked and unbanked communities.

The implementation of real-time funds can permit staff to obtain their wages promptly, and retailers to obtain cost with out the ready interval for funds to settle.

What Does FedNow Imply for Fintechs in 2023?

The FedNow program is at the moment solely accessible to licensed banks, which limits the advantages that non-bank monetary establishments can get pleasure from.

Fintechs, particularly, may benefit tremendously from this system, as it could permit them to expedite funds at a decrease value to customers. From depositing checks to paying payments, immediate funds may very well be a game-changer for fintech giants, like Stripe and

Clever, and will result in larger innovation within the banking business.

The Monetary Expertise Affiliation (FTA), which represents a spread of fintech corporations, has referred to as for “broader entity entry” to this system. If Fintechs are ultimately granted entry, it may open up a world of potentialities for quicker and extra handy

banking and cost processing.

For instance, real-time funds may allow suppliers to be paid immediately, mortgage funds to be processed extra shortly, and contract work to be paid out on the day it’s accomplished.

Regardless of the potential advantages, it stays unclear when non-bank monetary establishments might be granted entry to the FedNow program. Softjourn’s Cost Skilled, Yuriy Kropelnytsky, finds that “tighter governmental management and laws surrounding nonbank

lenders could also be vital to make sure that they’ll adjust to FedNow’s elevated client safety and fraud prevention”.

Within the meantime, we propose fintech corporations proceed to work on overlaying their know-how onto current financial institution methods, which may nonetheless present important enhancements within the pace and comfort of banking and cost processing.

Do not let your fintech enterprise get left behind on this quickly altering business. Softjourn has deep expertise in serving to fintechs digitally remodel their enterprise to maintain up with essentially the most highly effective rising applied sciences, akin to integrating with current

cost gateways or constructing their very own cost gateways.

Our fintech advisors, with nearly 20 years of expertise, will help you navigate the digital-first strategy and overcome any challenges that come up. We’ll assist you to perceive the advantages and downsides of real-time funds, develop a plan to combine

it into your system, and guarantee compliance with regulatory necessities.

How Will Fraud be Tackled with Instantaneous Funds?

Instantaneous funds and fraud are sometimes mentioned collectively, with the idea that quicker funds result in extra fraud. Nevertheless, in response to Jim Colassano, the Senior Vice President of RTP product administration at The Clearing Home, this isn’t essentially

the case for credit score ‘push’ transactions, that are inherently safer than direct debit transactions.

Whereas some folks fear in regards to the potential irreversibility of immediate funds, the transactions are literally processed by way of safe financial institution rails, that are among the many most safe cost channels on this planet.

With real-time funds altering the sport, banks should educate prospects to consider immediate funds like money funds and act accordingly. To make sure even larger security, some fintech corporations are growing commonplace APIs to assist monetary establishments

combine with fraud suppliers.

In the end, banks and networks have an obligation to guard their shoppers, which incorporates educating them and offering further layers of safety.

How Will FedNow Impression Different Actual-Time Cost Merchandise?

You could have seen the current information in regards to the FedNow Ripple controversy. Ripple presents related know-how to FedNow, besides it makes use of blockchain-based options. Ripple has been gaining recognition for providing low cost cross-border funds utilizing XRP – a token

used for representing the switch of worth throughout the Ripple Community. Nevertheless, Ripple has an ongoing case with the SEC over whether or not XRP is an unregistered safety.

FedNow strives to supply a safer various to Ripple and different related real-time, cross-border cost options within the US, for banks to maneuver funds throughout the US monetary system.

Jim Colassano, the Senior Vice President of Actual-Time Funds product administration at The Clearing Home (THC), mentioned the next in regards to the launch of FedNow:

There’s an enormous quantity of upside on this house, and I welcome the introduction of FedNow. FedNow and TCH have labored to guarantee that there aren’t any technical points for any originator who would need to use each networks.

Colassano believes that over time, FedNow, TCH, and different real-time suppliers could have wholesome competitors. “Over time,” he mentioned, “we’re going to be aggressive companions and we are going to be taught to distinguish our companies such that we are able to acquire aggressive benefits…

This might be wholesome for the business, and can enhance the companies that we’re offering to our shoppers.”

Wanting Forward

We predict that immediate funds will scale since there might be such excessive demand for this performance within the close to future. The truth is, it’s doubtless that suppliers will lose prospects in the event that they don’t supply that performance.

Dan Baum, FedNow’s head of funds product, mentioned 90% of companies have reported that the supply of immediate funds might be an essential a part of their banking decision-making.

This isn’t so stunning after we contemplate that as much as 80% of customers are actively utilizing quicker cost options, whereas one other 70% of customers say that they contemplate quicker funds as a significant factor in whether or not they’re glad with their monetary companies

suppliers.1

Total, the transfer in the direction of real-time funds is a constructive step for the US cost business, and one that’s prone to have a big affect on the best way transactions are carried out within the nation.

Do not miss out on the alternatives that real-time funds supply! By incorporating new companies into your online business, you possibly can unlock new enterprise fashions, develop buyer relationships, and enhance profitability.

Now’s the time to start out considering the mixing of FedNow and envisioning the way forward for real-time funds in the long run.

.jpeg?itok=EJhTOXAj'%20%20%20og_image:%20'https://cdn.mises.org/styles/social_media/s3/images/2025-03/AdobeStock_Supreme%20Court%20(2).jpeg?itok=EJhTOXAj)

{kind=link}