naphtalina/iStock through Getty Photographs

I really like the truth that markets are inefficient, giving worth traders loads of alternatives to layer into above common firms at under common costs, as long as they’re keen to be affected person. Within the phrases of Warren Buffett, “I would be sitting on the road with a tin cup in hand if markets had been environment friendly.”

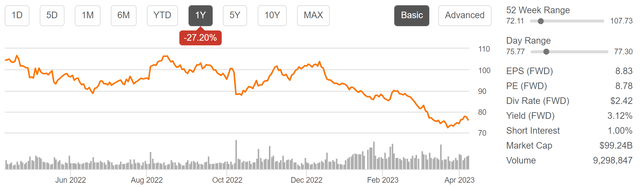

This brings me to CVS Well being (NYSE:CVS), which as proven under, has fallen by 27% over the previous 12 months. On this article, I spotlight what makes now a wonderful time to layer into this deep worth title for probably extremely rewarding long-term returns, so let’s get began.

CVS Inventory (Searching for Alpha)

Why CVS?

CVS has performed an admirable job of transitioning itself from being a neighborhood pharmacy to a number one well being options firm. This consists of buying Aetna and having a really massive pharmacy advantages supervisor. These strikes assist CVS to have extra management over its personal future within the healthcare panorama and higher handle prices for its members.

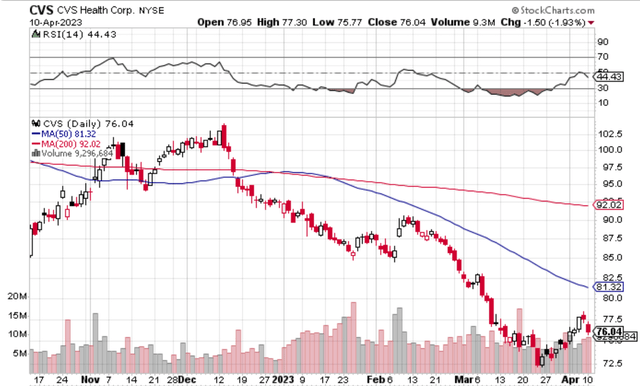

To get a way for the way low cost CVS has gotten, it is seen a double-dip in worth for the reason that begin of December. As proven under, CVS now trades under each its 50 and 200 day shifting averages of $92 and $81, respectively.

StockCharts

One of many causes for why market sentiment could also be working towards the inventory is the pending Oak Avenue acquisition, which is anticipated to shut within the first half of the 12 months. Oak Avenue will not be but worthwhile, and therefore the market seems to be spooked by lowered 2023 EPS estimates for CVS in consequence.

For these unfamiliar with the acquisition, Oak Avenue is a number one Medicare value-based main care platform with 169 main care clinics for which CVS is paying $10.6 billion to amass. It grew its income from $1.4 billion in 2021 to $2.2 billion in 2022, however nonetheless posted a internet loss in extra of $500 million final 12 months.

Nonetheless, the worth on this acquisition comes from enabling CVS to turn into a payer-agnostic enterprise inside the firm. As well as, Oak Avenue has a robust repute and gives a lower-cost setting than conventional care. These components mixed with CVS’s plans to attain profitability had been highlighted by fellow Searching for Alpha Analyst, Edmund Ingham, in a latest article:

Oak Avenue has a robust repute in healthcare. It reduces costly hospital admissions. It gives holistic affected person care, which incorporates lowering depressive signs. Physicians spend extra time with sufferers, and facilities are situated in medically underserved areas. Throughout the medical insurance enterprise, the flexibility to regulate your members is extraordinarily vital.

CVS additionally believes that there’s a “clear path to profitability” – regardless of the very fact Oak Avenue’s enterprise mannequin has misplaced >$1bn throughout the previous three years.

The trail is predicated on fast development of clinics – from 169 to >300 by 2026, with every clinic producing ~$7m of EBITDA (analysts had been advised on CVS’s Q422 earnings name), which provides as much as >$2bn of EBITDA contribution by 2026, and unlocks ~$500m of value synergies, CVS says, which is able to permit it (CVS) to drive general earnings per share >$10 by 2025.

In the meantime, CVS continues to expertise respectable development, with income rising by 9.5% YoY throughout its fourth quarter. This capped a robust 12 months, throughout which income grew by 10.4% over the prior 12 months. This was pushed partly by a decrease MBR (medical advantages ratio) from 85% in 2021 to 84% in 2022, because of much less affect from COVID-19. Additionally encouraging CVS’s medical memberships grew by greater than half one million (548,000 internet new members) to 24.4 million as of the final reported quarter.

Importantly, CVS stays a money wealthy enterprise, producing $16.2 billion in working money movement final 12 months, of which it utilized $3.5 billion in share buybacks within the final reported 12 months. Contemplating that CVS’s inventory traded at or under $100 throughout most of this time, it could be protected to imagine that CVS bought a gorgeous 9%+ weighted common earnings yield on these buybacks (primarily based $8.69 EPS final 12 months).

Furthermore, CVS is rewarding earnings traders with a ten% dividend bump earlier this 12 months. Whereas the three.2% dividend yield is not significantly excessive, it does include a really protected 28% payout ratio primarily based on the midpoint of administration’s 2023 EPS steering.

CVS additionally has loads of stability sheet capability to completely fund the Oak Avenue deal, because it has $15.7 billion in money and short-term investments available. CVS has additionally made nice strides in deleveraging, because it lowered long-term debt by $21.7 billion since 2018 (the time of the Aetna acquisition). This went a good distance in lowering the online debt to EBITDA ratio to 2.8x, which sits under the 3x stage that the majority rankings businesses contemplate to be protected, and helps its BBB credit standing from S&P.

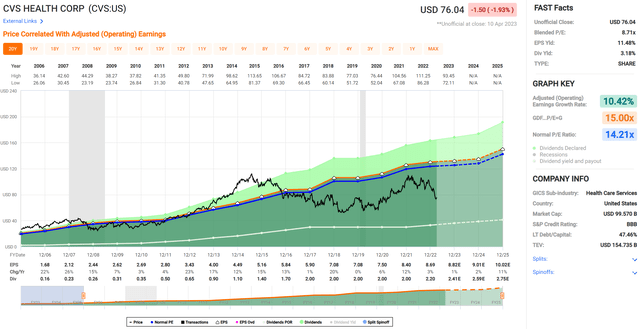

Lastly, I view CVS as being in deep discount territory on the present worth of $76 with a really low ahead PE ratio of simply 8.6, sitting far under its regular PE of 14.2. At this valuation, the market is actually pricing in a zero development future.

This does not seem like the case, as whereas present 12 months EPS is anticipated to develop by simply 1.5%, analysts anticipate 4% to eight% annual development within the 2024 to 2025 timeframe. Promote facet analysts have a consensus Purchase ranking with a mean worth goal of $111, implying probably very sturdy whole returns over the subsequent 12 to 24 months.

FAST Graphs

Investor Takeaway

CVS’s acquisition of Oak Avenue is a daring transfer, however one which seems to make strategic sense. The corporate has a transparent path to profitability and can profit from value synergies and fast development in clinics. CVS stays money wealthy, with loads of stability sheet capability to fund the deal, and has rewarded affected person earnings traders with a dividend enhance and share buybacks.

With the inventory presently buying and selling at deep discount ranges, there seems to be loads of upside potential over the subsequent 12 to 24 months. For traders on the lookout for a protected defensive play with loads of worth and stable development prospects, CVS could also be a gorgeous possibility.

{kind=link}