JuSun

Whereas shopping for high quality companies and holding for the long-term actually has its deserves, there are additionally instances when it is very important know when to prune your portfolio. On this article we clarify our philosophy regarding when to promote a inventory. We then go on to elucidate why we not too long ago bought 2 excessive yield shares in our portfolio and record some locations the place we’re placing capital to work as nicely.

When To Promote A Inventory

Deciding when to promote a inventory is the second most essential resolution you ever make as an investor (an important being when to purchase). In spite of everything, whereas it could be true that you simply earn a living whenever you purchase, executing a sale on the proper time is essential for limiting your losses and maximizing your features.

Promoting a inventory on the proper time is essential for minimizing losses as a result of some shares are merely doomed to be perennial underperformers and a few even are destined for $0 as their companies go bankrupt. Regardless of how low cost it could look relative to its inventory chart and even when in comparison with varied valuation metrics, if the steadiness sheet is in horrible form, the enterprise’ aggressive positioning is quickly weakening, the macroeconomic dynamics are just too difficult for the enterprise to beat, and/or there are basic shifts within the nature of the inventory’s trade resulting from technological disruption or modifications in client habits, there’s a sturdy likelihood that the inventory is value promoting.

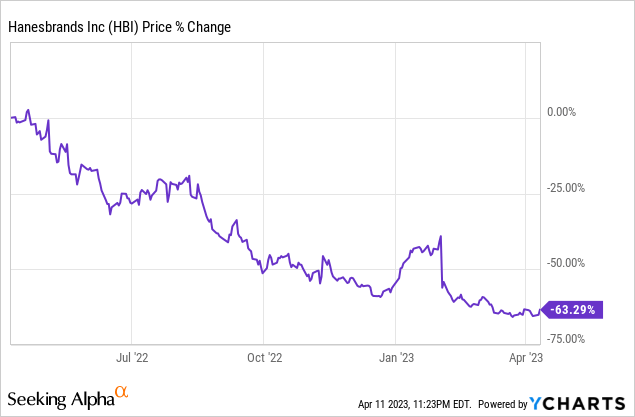

A reasonably current instance of that is Hanesbrands (HBI). Whereas administration appears glorious and carefully aligned with shareholders (the comparatively new CEO is a former senior Walmart (WMT) govt pursuing a daring “Full Potential Plan” for the corporate and he has been shopping for shares aggressively on the open market since becoming a member of the corporate), the corporate was hit by an ideal storm of hovering inflation, provide chain imbalances, and a cyberattack. Whereas the inventory regarded low cost a 12 months in the past, the corporate’s substantial working leverage and substantial leverage on the steadiness sheet indicated that it had loads of room to fall if issues didn’t go its manner.

It seems that one factor led to a different and ultimately the corporate not solely minimize, however solely eradicated its dividend whereas additionally having to change its debt covenants with its collectors. Evidently, the inventory received crushed in consequence:

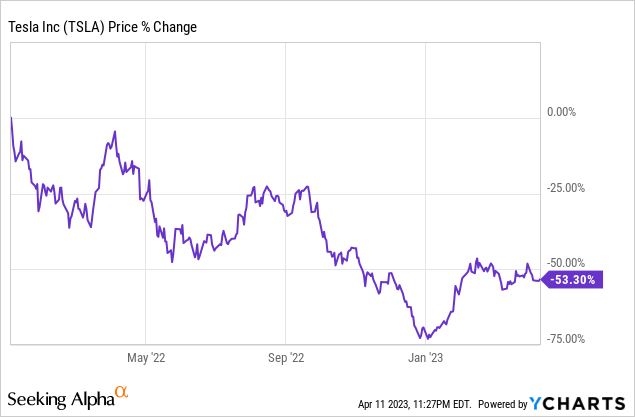

Furthermore, generally it’s even important to know when to promote a profitable inventory as a result of there are many instances when the valuations assigned to shares of nice companies merely get manner out in entrance of the corporate’s fundamentals. In case you fall in love with the inventory, you might endure a speedy evaporation of earnings or threat vital future underperformance by holding it too lengthy whereas it’s overvalued. An ideal current instance of that is Tesla (TSLA). Whereas the enterprise is clearly an outstanding success story and continues to generate sturdy progress, the inventory merely received bid up too far forward of the underlying fundamentals, throughout the tech inventory (ARKK) mania of late 2020 by means of 2021. In consequence, regardless of the corporate persevering with to develop its manufacturing capability and gross sales, for the reason that starting of 2022, TSLA inventory has misplaced greater than half its worth. Therefore, for individuals who subscribe religiously to the “purchase, maintain, and by no means promote” method to investing, they’ve actually paid the value with TSLA over the previous 15 months.

In abstract, there are two instances after we imagine it’s best to promote a inventory:

When the funding thesis breaks, making the inventory now not investible. This mainly implies that the corporate has a number of severe vulnerabilities that make figuring out a conservative valuation estimate extraordinarily troublesome and the dangers subsequently change into too nice to make the inventory value holding, regardless of how “low cost” it appears to be like. Even when the enterprise fundamentals are sound sufficient to find out a conservative truthful worth estimate, the inventory value is excessive sufficient that the chance price of continuous to carry the inventory is solely not value it. In these instances, it’s best to make the most of the simple and comparatively frictionless liquidity that Mr. Market affords right this moment’s investor and promote the place so as to reinvest the proceeds into extra opportunistically priced securities.

Clearly tax ramifications additionally play a task in promoting, however that could be a matter for an additional article at one other time. This text’s evaluation assumes the shares are being held in a tax-advantaged account, so for the needs of this text, we’re ignoring tax ramifications.

Why We Just lately Bought Two Shares

With that philosophy in thoughts, we not too long ago determined to promote two excessive yield dividend progress shares: Important Properties Realty Belief (EPRT) and Cogent Communications (CCOI). Right here is why:

We bought each of those shares primarily resulting from valuations.

Since buying EPRT final September, it considerably outperformed the broader REIT sector (VNQ), by producing 12.7% whole returns (24.83% annualized) whereas VNQ returned -9.65% over that very same time interval. Furthermore, there are a number of blue chip REITs with related and even increased yields than EPRT which have fallen by over 20% throughout that very same time interval.

For instance, over the previous two months, the bifurcation in efficiency between EPRT’s and life sciences REIT Alexandria Actual Property’s (ARE) inventory costs has been particularly pronounced:

In consequence, in our view ARE affords each higher whole return potential in addition to a considerably superior risk-reward profile relative to EPRT.

Furthermore, our portfolio at the moment already has loads of publicity to center market companies by way of our Enterprise Improvement Firm (BIZD) investments. Whereas we expect there may be engaging risk-reward on this phase of the economic system, additionally it is a bit riskier throughout a recession. In consequence, by promoting EPRT (whose tenants are nearly solely center market companies), we’re lowering our publicity to this sector.

In distinction, we’ve got lacked a lot publicity to healthcare not too long ago and lots of of our members have expressed a want for the portfolio to characteristic extra publicity to healthcare. On condition that we aren’t expert biochemists and are unable to supply value-add evaluation of drug pipelines and portfolios among the many massive pharma corporations, we’ve got been unable to search out excessive yielding alternatives within the healthcare area. Nevertheless, because of the in-depth evaluation of our REIT analyst Jussi Askola, we do have an excellent grasp of the true property sector. With ARE we’re in a position to leverage that actual property information to additionally get significant publicity to a better yielding safety that additionally provides us vital publicity to the healthcare trade.

Whereas EPRT at the moment trades at a premium to its web asset worth and affords good – however not nice – whole return potential between its 4.5% yield and a ~5-7% anticipated per share progress CAGR within the coming years, we see little valuation a number of growth potential with this inventory.

In distinction, ARE at the moment affords a ~4% yield and together with an ~8-10% anticipated per share AFFO CAGR within the coming years. On high of that, it at the moment trades at a ~33% low cost to NAV, so we see vital valuation a number of growth potential within the coming years, bringing its anticipated whole return profile to fifteen%+.

Furthermore, EPRT has a BBB- credit standing whereas ARE has a BBB+ credit standing and an especially sturdy steadiness sheet, with the bottom leverage ratio in its historical past, virtually no floating charge debt, no debt maturing till 2025 (with well-staggered maturities thereafter), and loads of liquidity. It owns trophy, mission-critical life science lab properties that take pleasure in long-leases and are experiencing very sturdy re-leasing spreads. In consequence, its properties usually take pleasure in a stronger moat relative to EPRT’s single tenant triple web lease retail and repair properties. Lastly, its tenants are largely funding grade and/or giant publicly traded biotech/pharmaceutical corporations which can be recession resistant and have excessive capability for servicing the leases on these mission-critical properties, making them higher candidates for weathering a recession than lots of EPRT’s tenants. You may learn our in-depth ARE evaluation in addition to takeaways from administration at a current REIT convention right here.

In the meantime, we additionally simply bought our place in CCOI, locking in engaging 13% (13.6% annualized) whole returns within the course of. CCOI additionally meaningfully outperformed the broader inventory market (SPY) in addition to the excessive yield (DIV) and communications (XTL) sectors over that time period, with SPY producing a -0.33% whole return, DIV producing a -10.44% whole return, and XTL producing a -2.86% whole return over that interval.

Whereas CCOI stays undervalued in our view, its low cost to our Purchase Beneath Worth estimate has narrowed to a degree that’s meaningfully under the brink that may be required for it to be thought of a Robust Purchase. As such, it’s now not a excessive conviction decide for us. With so many deeply undervalued alternatives within the excessive yield area for the time being, we imagine that recycling this capital elsewhere will enhance our risk-reward profile.

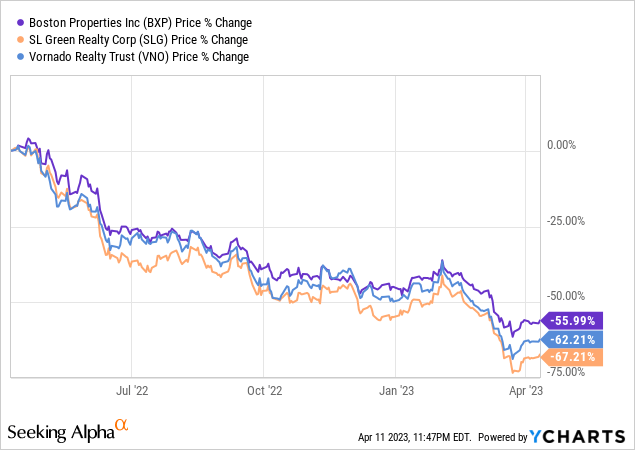

CCOI’s core enterprise is very delicate to workplace area demand/occupancy. As such, it has struggled to recuperate from the headwinds it suffered throughout COVID-19 because the work-from-home development has gained steam. Furthermore, workplace actual property is struggling mightily proper now as illustrated by the current inventory value efficiency of main workplace REITs like Boston Properties (BXP), SL Inexperienced (SLG), and Vornado (VNO):

Because of the lingering headwinds to workplace, CCOI has needed to sluggish its dividend progress charge not too long ago whereas additionally betting closely on a take care of T-Cellular (TMUS) to reignite the expansion engine. Whereas CCOI’s monitor file provides us confidence that the corporate will be capable to efficiently combine these new belongings and show the deal to be accretive over time, it nonetheless stays extra of a speculative progress story than if CCOI’s core enterprise have been rising in-line with its historic norms.

Finally, with CCOI’s inventory value outperforming our notion of its fundamentals and quite a few different engaging excessive yielding alternatives being out there for the time being with even higher progress prospects and extra defensive enterprise fashions and steadiness sheets than CCOI’s, we determined it was prudent to promote the place now to lock in features and unencumber capital for reallocation elsewhere.

Investor Takeaway

Promoting a inventory may be extraordinarily troublesome, however it’s actually essential to get proper. When a inventory retains dropping – and for good motive – it may be actually troublesome to chop it free. Promoting a giant loser feels dangerous since you are locking within the loss and in the end admitting that you simply made a mistake and Mr. Market was proper all alongside. Anytime you damage your pocketbook and your ego with a single click on of the mouse, it’s usually an especially painful course of.

Promoting and even trimming a giant winner can be actually troublesome as a result of it’s simple to fall in love with shares that hold hovering increased and better with seemingly little regard for valuations. Nevertheless, as Benjamin Graham as soon as mentioned:

Within the quick run, the market is a voting machine however in the long term, it’s a weighing balance.

By permitting feelings to supersede rational inventory value evaluation, buyers who successfully marry their overvalued winners set themselves as much as doubtlessly witness a big proportion of their features quickly evaporate or on the very least expertise vital underperformance transferring ahead.

By promoting our positions in EPRT and CCOI after they considerably outperformed the market and as such have been now not compellingly undervalued, we freed up capital to recycle into extra attractively priced alternatives like ARE and others which provide us superior risk-adjusted return potential transferring ahead.

{kind=link}