Lorado/E+ by way of Getty Photos

Article Thesis

Exxon Mobil Company (NYSE:XOM) reported its first-quarter earnings outcomes on Friday morning. The corporate outperformed expectations and delivered sturdy outcomes throughout the board. Buyers might be very proud of XOM’s operational efficiency, however its valuation will not be the bottom within the vitality area – though it is not excessive in absolute phrases, both.

What Occurred?

Exxon Mobil Company reported its first-quarter earnings outcomes on Friday earlier than the market opened. The corporate’s top-line and bottom-line outcomes might be seen right here:

Looking for Alpha

Whereas revenues had been down on a year-over-year foundation, and lacking estimates, Exxon Mobil was far more worthwhile than what the analyst neighborhood had anticipated. For a mature worth firm comparable to Exxon Mobil, income are extra vital than gross sales, I imagine, thus I see these numbers positively.

Exxon Mobil: The King In The Vitality Area

Not too way back, the market wasn’t appreciating Exxon Mobil. The corporate misplaced its place within the Dow Jones Index, and for a while, its peer Chevron Company (CVX) was buying and selling at the next market capitalization versus Exxon Mobil. On the time, the market did not like Exxon Mobil’s progress spending and its concentrate on bringing new main oil initiatives ahead, comparable to its huge asset base in Guyana.

However with oil costs rising considerably following the pandemic, Exxon Mobil is now again the place it belongs – on the high of the vitality area. This holds true after we take a look at its market capitalization, but additionally after we take a look at the underlying outcomes that Exxon Mobil generates. These weren’t solely sturdy throughout 2022, however XOM continued to carry out very nicely in early 2023, even if oil and gasoline costs have pulled again considerably from the highs seen in the summertime months of 2022.

Exxon Mobil generated web earnings of $11.4 billion throughout the first quarter, which was round 15% beneath the degrees seen throughout the earlier quarter, This autumn 2022, however which was up massively on a year-over-year foundation. Even higher, Exxon Mobil’s Q1 2023 outcomes had been one of the best Q1 leads to the corporate’s historical past – not even in 2008, when oil costs peaked at round $150 XOM was this worthwhile. This may be defined by a number of contributing components.

First, Exxon Mobil’s ongoing investments in its asset base are more and more paying off. Whereas another vitality corporations have modified their enterprise mannequin by decreasing oil and gasoline investments whereas placing extra money into inexperienced vitality investments, XOM has remained centered on growing hydrocarbon property, primarily within the Permian Basin and in Guyana. On the similar time, Exxon Mobil has additionally been investing in refining property – its 250,000 barrels per day Beaumont refinery enlargement began manufacturing and reached capability in Q1, for instance. Exxon Mobil can also be energetic within the “inexperienced” business by way of its rising carbon-capture enterprise, which is probably very promising, however we do not know but how worthwhile this franchise will grow to be. However in contrast to friends comparable to BP p.l.c. (BP) or Shell plc (SHEL), XOM continues to pursue progress within the hydrocarbon area, which is paying off within the present oil worth surroundings. Excluding the influence of divestments and the Sakhalin-1 expropriation, manufacturing was up by a hefty 300,000 barrels per day throughout the first quarter, relative to the earlier yr’s first quarter.

Second, Exxon Mobil has been laser-focused on bringing down bills with a view to increase margins. Most vitality corporations moved on this path following the 2014 oil worth crash, and much more so following the 2020 oil worth disaster throughout the preliminary part of the pandemic. Total, the business has grow to be leaner and extra environment friendly, however Exxon Mobil stands out amongst its friends. Its cost-cutting efforts have been extremely efficient, and the corporate continues to pursue further value financial savings, even if it is vitally worthwhile already. By the tip of 2023, XOM plans to have achieved $9 billion in structural value financial savings, whereas the price financial savings totaled $7.2 billion on the finish of 2023. All through the approaching three quarters, XOM thus plans to shave one other $2 billion in bills. Buyers might be very joyful about this shareholder value-driving strategy of enhancing XOM’s effectivity – a leaner and meaner XOM is a extra worthwhile, lower-risk XOM.

Exxon Mobil’s sturdy profitability naturally additionally interprets right into a compelling money circulate image. The corporate generated working money flows of $16.3 billion throughout the first quarter, which interprets into free money flows of $11.4 billion as soon as we account for investments and divestments. With $6.3 billion in capital expenditures throughout the quarter, XOM is just about on monitor to realize its ~$24 billion funding goal for the present yr. With annualized free money flows within the $46 billion vary, Exxon Mobil trades at a little bit greater than 10x free money flows proper now, which is much from a excessive valuation in absolute phrases.

There are a number of methods for an organization to make the most of its free money flows. They are often returned to shareholders by way of dividends and/or buybacks, they can be utilized for deleveraging, or they can be utilized for M&A. Whereas there are rumors about potential acquisitions by Exxon Mobil (Pioneer Pure Assets (PXD) is a rumored goal), XOM has not made any main M&A strikes within the current previous. The corporate is thus centered on shareholder returns and debt discount, which isn’t a nasty factor.

Through the first quarter, Exxon Mobil paid out $8.1 billion to its house owners, with a little bit greater than half of that by way of buybacks, and the rest by way of dividends. The buyback tempo of round 4% may be very strong, though by far not the best within the vitality area. The dividend yield of three.1%, likewise, is strong however not nice relative to the peer group common. In relation to strengthening the steadiness sheet, Exxon Mobil has made large progress lately. As of the tip of the primary quarter, Exxon Mobil’s web debt (whole debt minus money and equivalents) stood at simply $8 billion – that is down from a peak of greater than $60 billion on the finish of 2020. It might not be shocking to see Exxon Mobil finish 2023 with a optimistic web money place, as paying down one other $8 billion in web debt should not be too onerous for the corporate over the following three quarters, not less than if there isn’t any main acquisition. Exxon Mobil has guided for $17.5 billion in buybacks throughout 2023, which is comparatively in step with the buyback tempo in Q1, thus it doesn’t appear like shareholder returns can be ramped up once more within the close to time period.

Until oil costs drop considerably, XOM ought to thus have ample extra free money circulate in Q2-This autumn that can be utilized for debt discount whereas persevering with to supply shareholder funds at an analogous degree as in Q1. Exxon Mobil’s fortress steadiness sheet that’s getting stronger each quarter insulates the corporate from rising rates of interest and reduces dangers – even when oil costs had been to fall off a cliff (which appears unlikely to me), XOM can be well-positioned to abdomen that.

XOM’s Valuation

From an operational foundation, there are a lot of issues that look nice. Manufacturing is rising, the corporate owns sturdy low-risk, low-cost property within the Permian Basin and Guyana, and administration has finished an important job in the case of bringing down bills and enhancing margins.

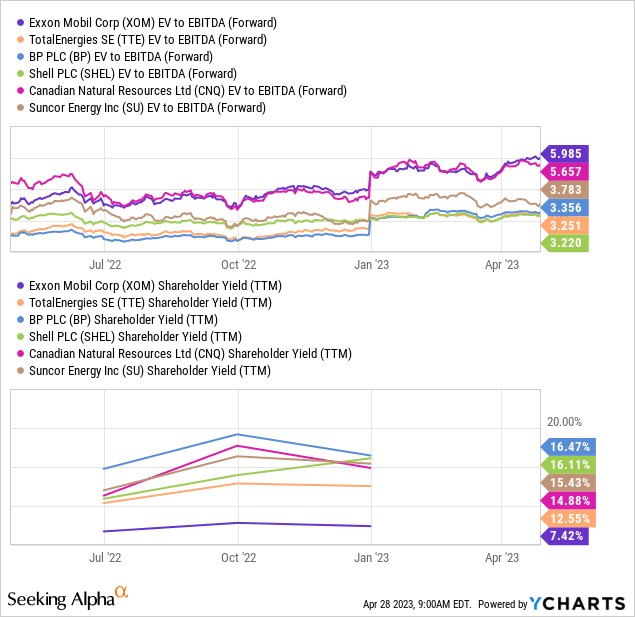

Sadly, whereas not being costly in absolute phrases, XOM is by far not as low cost as a few of its friends:

XOM trades with an enterprise worth to EBITDA a number of of 6.0, which is considerably increased in comparison with the valuation its European friends commerce at, comparable to TotalEnergies SE (TTE), Shell, and BP. The Canadian built-in vitality corporations comparable to Canadian Pure Assets (CNQ) and Suncor (SU) are additionally cheaper. That is not XOM’s fault, however it implies that shareholders should pay a considerable premium in the event that they wish to personal XOM over different main vitality gamers. On the similar valuation, I certainly would like XOM over Shell or BP – however when the latter two commerce at half the valuation XOM trades at, I believe otherwise.

XOM’s premium valuation additionally leads to a relatively weak shareholder yield – not in absolute phrases, however in relative phrases. Whereas a 7% shareholder yield may be very strong, the 13%-16% shareholder yields of XOM’s friends are much more engaging, in fact.

Takeaway

Exxon Mobil Company is the biggest (Western) oil firm and one of many strongest for positive. Its efficiency has been nice, and its technique of specializing in property comparable to Guyana is paying off. The Q1 outcomes had been extremely compelling as nicely, and I imagine that XOM can rightfully be known as the king within the vitality area.

However with a few of its friends buying and selling at exceptionally low valuations, whereas Exxon Mobil Company is significantly costlier, I nonetheless favor to carry its cheaper, higher-yielding friends, though I might certainly swap to Exxon Mobil Company in case they had been to commerce at related valuations and yields.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}