Introduction: UK home costs rise in April after seven consecutive falls

Good morning, and welcome to our rolling protection of enterprise, the world economic system and the monetary markets.

UK home worth progress picked up in April, constructing society Nationwide studies this morning, with the primary month-to-month enhance in seven month.

Common home costs rose by 0.5% final month, Nationwide’s information exhibits, following seven consecutive falls going again to final September.

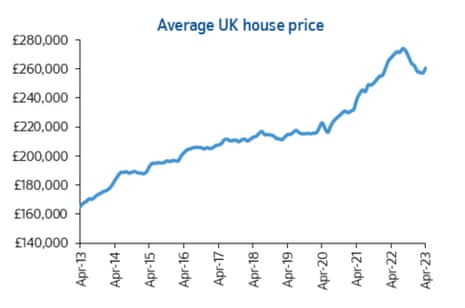

The common worth elevated to £260,441, up from £257,122 in March.

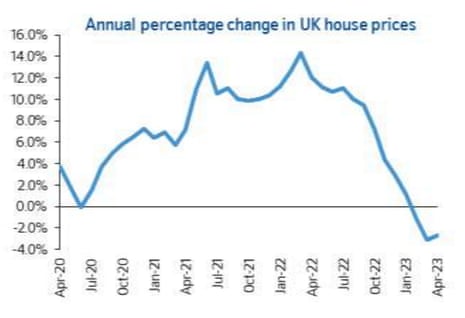

This has lifted the annual price of home worth progress to -2.7%, from -3.1% in March (the largest fall since 2009), as calm returned to the markets after the chaos of final autumn’s min-budget.

Robert Gardner, Nationwide’s chief economist, studies there have been “tentative indicators of a restoration” available in the market final month, though this nonetheless leaves costs 4% beneath their August 2022 peak.

Gardner explains:

“Current Financial institution of England information means that housing market exercise remained subdued within the opening months of 2023, with the variety of mortgages authorized for home buy in February practically 40% beneath the extent prevailing a yr in the past, and round a 3rd decrease than pre-pandemic ranges.

Nonetheless, in current months business information on mortgage purposes level to indicators of a pickup.

Final month, Rightmove reported that asking costs had been at report ranges:

Gardner says the current pick-up in UK client confidence could also be serving to the housing market, however cautions that….

….any upturn is more likely to stay pretty pedestrian, as it would take time for family funds to recuperate, since common earnings have been failing to maintain tempo with inflation, and by a large margin over the previous couple of years.

Mortgage rates of interest are additionally more likely to act as a headwind. Whereas they’re nicely beneath the highs seen within the wake of the mini-Funds final yr, charges are nonetheless greater than double the extent prevailing a yr in the past.

Additionally arising in the present day

Britain’s largest supermarkets are dealing with requires the UK’s competitors watchdog to analyze claims of profiteering amid the price of dwelling disaster, as meals worth inflation soared to a report excessive in April.

In a single day, Australia’s central financial institution has stunned buyers by elevating rates of interest once more.

The RBA board raised its money price 25 foundation factors to three.85% at its month-to-month assembly on Tuesday, defying buyers who had wager the central financial institution would prolong its pause for a second month.

Greater rates of interest raise income at banks….. comparable to HSBC, which has reported a three-fold bounce in earnings within the final quarter, On a continuing forex foundation, HSBC’s revenue earlier than tax elevated by $9.0bn to $12.9bn, main the financial institution to launch as much as $2bn of share buybacks and a ten cent-per-share dividend.

BP has defied an easing in power costs to submit one of many largest first-quarter income in its historical past, reigniting a debate over windfall good points by oil and fuel companies.

The power big stated its underlying income hit $5bn (£4bn) within the first three months of the yr, outstripping analysts’ forecasts. Extra on this shortly…

The newest manufacturing facility PMI studies will present how producers within the UK and the eurozone fared in April. That follows a shock contraction in China’s manufacturing facility output, reported on Sunday.

We get the most recent eurozone inflation report this morning, with costs anticipated to have risen by 7% within the 12 months to April, up from 6.9%. Core inflation may stick at 5.7%, worryingly excessive for the European Central Financial institution.

The agenda

7am BST: Nationwide home worth index for April

9am BST: Eurozone manufacturing PMI for April

9.30am BST: UK manufacturing PMI for April

10am BST: Eurozone core inflation price on April

3pm BST: US Manufacturing facility Orders for March

Up to date at 02.57 EDT

Key occasions

UK manufacturing downturn continues as demand falls

The downturn within the UK manufacturing sector continued in April as factories had been hit by weak demand, the most recent survey of manufacturing facility buying managers exhibits.

April’s manufacturing PMI survey exhibits that output and new orders at UK factories contracted final month, because the manufacturing downturn continued.

Output, new orders, employment and shares of purchases all contracted throughout April, with firms reporting a drop in demand, on account of “consumer destocking” as prospects tried to chop their prices.

This pulled the S&P World / CIPS UK manufacturing PMI all the way down to a three-month low of 47.8 in April, from 47.9 in March, beneath the 50-point mark exhibiting stagnation – however higher than the sooner flash estimate of 46.6.

New export orders contracted for the fifteenth consecutive month, with companies reporting softer demand from the US, China and mainland Europe.

However, there are additionally indicators that provide chain pressures have eased. Producers’ enterprise optimism rose to 14-month excessive, whereas vendor supply instances shortened for the third successive month.

The downturn within the #UK manufacturing sector continued in April (#PMI at 47.8; Mar: 47.9) amid sustained contractions in output and new orders. However there’s a silver lining in the truth that provide and inflationary pressures eased on the month. Learn extra: https://t.co/TtSS4TDrnu pic.twitter.com/iub3OFVTXC

— S&P World PMI™ (@SPGlobalPMI) Might 2, 2023

Rob Dobson, director at S&P World Market Intelligence, stated:

“The UK manufacturing sector remained within the doldrums in the beginning of the second quarter. Output and new orders contracted, as producers felt the impacts of consumer uncertainty, destocking and tightening value controls.

There was no escape from the subdued temper of the market, with each home and export prospects remaining reticent to decide to new contracts.

However, the autumn in provider lead time is best information, serving to to push down uncooked materials worth pressures, Dobson provides:

“Higher-running provide chains have helped producers cut back backlogs of orders, amassed in prior months amid element shortages. However the concern is that these backlogs are being depleted, leaving companies with much less work in hand.

There could also be some gentle on the horizon, as producers stay stoically optimistic in regards to the outlook for the yr forward. Over 60% of companies count on to increase manufacturing over the subsequent 12 months. However demand might want to choose up within the months forward to warrant any enhance in manufacturing, and with the UK seeing stubbornly excessive home inflation coupled with a worsening export development, dangers appear skewed to the draw back.”

Eurozone manufacturing facility downturn deepens, however enter worth pressures ease

The eurozone manufacturing facility downturn deepened final month, based on the most recent survey of buying managers, whereas uncooked materials costs have dropped.

The HCOB ultimate manufacturing Buying Managers’ Index (PMI), compiled by S&P World, has fallen to 45.8 in April from March’s 47.3. That’s barely higher than the ‘flash’ studying of 45.5, however nicely beneath the 50 mark separating progress from contraction for the tenth month in a row.

The PMI was pulled down by a drop in the price of uncooked supplies, which suggests inflationary pressures are easing. Corporations reported the largest drop in working bills in virtually three years.

This allowed companies to sluggish their very own worth rises; the output costs index fell to a 29-month low of 51.6 from 53.4.

An index measuring output fell beneath the breakeven mark to 48.5 from 50.4.

Cyrus de la Rubia, chief economist at Hamburg Business Financial institution, says:

“This decline has been pretty broad-based throughout the euro zone, with regional PMI indices in France and Italy additionally exhibiting a drop in output, whereas output in Germany and Spain was practically stagnant.”

In Germany, retail gross sales have dropped by greater than anticipated, as customers in Europe’s largest economic system retrench.

German retail gross sales fell by 2.4% in March in actual phrases from the earlier month, the Federal Statistics Workplace reported this morning, that means retail gross sales had been down 8.6% year-on-year in actual phrases.

Analysts polled by Reuters had predicted a month-on-month enhance of 0.4%.

German retail gross sales stumbled in March falling to 9% beneath their pre-pandemic development on broad weak point. Probably a key motive for Q1 GDP coming in beneath expectations. Even permitting for some revisions that is a horrible carryover into Q2. https://t.co/P90VdXvWMO pic.twitter.com/JTtAlTu3OL

— Oliver Rakau (@OliverRakau) Might 2, 2023

European monetary markets have made a subdued begin to the brand new month.

The FTSE 100 index was barely larger in early buying and selling, led by rallying housebuilders (see earlier submit), and HSBC (up 4.3% after asserting a share buyback following a bounce in income).

UK rates of interest may rise as much as 4.75% this yr, economist predicts

The shock rise in UK home costs in April is reigniting curiosity in how excessive the Financial institution of England might elevate rates of interest this yr.

Professor Costas Milas, of the Administration College at College of Liverpool, argues that the BoE may raise rates of interest to 4.75% this yr.

In a brand new blogpost, Professor Milas explains that prime public expectations of inflation have the potential of placing extra stress on present inflation by means of demand for larger wages.

However this prediction is conditional on monetary stress not escalating additional. If, as a substitute, monetary stress worries take over, UK rates of interest may find yourself beneath 4% by the tip of 2023, he suggests.

Professor Milas says:

In reality, there’s rising expectation that the Chancellor of the Exchequer will enhance the extent for assured UK deposits, from £85,000 at present. This implies to me that UK regulators are considerably anxious that we now have not absolutely escaped the chance of a monetary/banking disaster.

Subsequently, I don’t rule out the likelihood that the BoE will lower UK rates of interest beneath 4 per cent by the tip of the yr.

JPMorgan’s transfer (over the weekend) to accumulate most of failed US financial institution First Republic is a (fixed) reminder that monetary stress just isn’t over.

The total blogpost is right here:

Housebuilder shares rally

Shares in UK housebuilders have jumped this morning, after Nationwide reported an sudden enhance in UK home costs final month.

Persimmon are up 5.8% in early buying and selling, with Barratt Improvement (+2.5%) and Taylor Wimpey (+2.5%) and Berkeley Group (+2%) additionally within the prime FTSE 100 risers.

The sector may be benefitting from studies that Rishi Sunak is drawing up plans to spice up help for first-time house patrons.

In line with The Occasions, officers in Downing Avenue and the Treasury are taking a look at proposals to assist 1000’s of renters who’ve been unable to get on the housing ladder within the face of excessive costs and rising rates of interest.

Up to date at 04.28 EDT

BP’s ‘heinous’ income of just about $5bn (£4bn) within the final quarter present the necessity for a everlasting ‘polluters tax’, says World Justice Now, the marketing campaign group:

“At this time’s heinous income from BP are one other kick within the tooth to the hundreds of thousands of people that can’t afford to warmth their houses.

BP has additionally quietly lowered its already weak local weather targets, leaving us all to undergo much more from their local weather damages while they line their pockets in a cost-of-living disaster.

We want a everlasting polluters tax on massive oil to account for this rampant profiteering and their persevering with unabashed function within the local weather disaster.”

Right here’s our information story on BP’s income:

BP shares fall 4.5% regardless of bumper income

Within the Metropolis, shares in BP have dropped by 4.5% in early buying and selling regardless of the oil big reporting bumper income of aroudn $5bn for the final quarter.

BP made $4.963bn on its favoured revenue measure in January-March, up from $4.8bn in October-December 2022, however decrease than the $6.245bn in Q1 2022 when the Ukraine battle drove up costs.

That was forward of expectations for $4.3bn, and BP’s second-best outcome since 2012 due to sturdy oil and fuel buying and selling.

Bernard Looney, BP’s chief government officer, says Q1 was “1 / 4 of sturdy efficiency and strategic supply”, including:

And importantly we proceed to ship for shareholders, by means of disciplined funding, reducing web debt and rising distributions.

However buyers, considerably ungratefully, appear disenchanted that BP has lower its share buyback programme. The corporate plans to spend one other $1.75bn shopping for up its inventory, decrease than the $2.75bn share buyback introduced after the final quarter of 2022.

Share buybacks are a method of funnelling money to buyers; Joseph Evans, researcher at IPPR, argues they need to be taxed within the UK:

“BP continues to revenue from the cost-of-living disaster. Whereas some UK households spent the winter dealing with the grim selection between heating or consuming, BP continued to take advantage of geopolitical fallout from battle in Ukraine – driving up costs and income.

“As a substitute of utilizing these income to spend money on net-zero or cut back prices for customers, BP is transferring an outrageous sum of wealth from abnormal households to their buyers. The USA and Canada have already taken motion on extreme shareholder payouts: it’s lengthy overdue for the federal government to observe go well with by introducing a tax on share buyback schemes.”

BP has simply introduced income of £4 billion for the final quarter + a brand new spherical of share buybacks, transferring £1.4 billion ($1.75 billion) to shareholders.@evansjoseph_ says BP are “driving up costs and income” on the expense of households. pic.twitter.com/w2pCWxRZEx

— IPPR (@IPPR) Might 2, 2023

UK housing market ‘might have troughed’, however affordability nonetheless very difficult

At this time’s Nationwide home worth information is one other signal that weak point within the housing market “might have troughed”, studies Martin Beck, chief financial advisor to the EY ITEM Membership.

Beck says:

“One month doesn’t make a development and, given the diploma of volatility in home worth measures, April’s rise within the Nationwide gauge may show short-lived. However it’s according to different indicators that weak point available in the market might have bottomed out. The Halifax measure of costs rose in every of the primary three months of 2023. Whereas mortgage approvals had been nonetheless very low in February, they elevated for the primary time since final summer time.

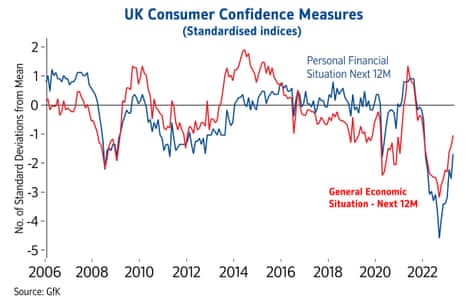

And survey proof on new purchaser curiosity and the supply of houses on the market has just lately proven indicators of life. On prime of that, the economic system could also be turning a nook, aided by falling power costs, with job creation persevering with at a strong tempo and client confidence recovering.

However, home costs stay very excessive on most measures of affordability, Beck factors out:

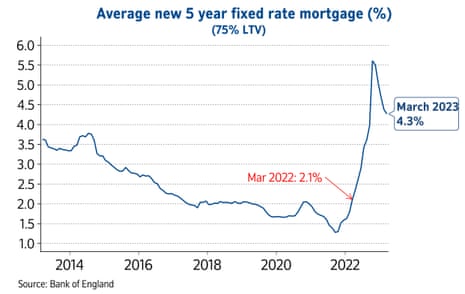

Mortgage charges have seen a big rise over the past yr, with the common price on a brand new mortgage rising to 4.26% in February from 1.60% 12 months earlier. Borrowing prices may enhance additional if, because the EY ITEM Membership expects, the Financial institution of England raises rates of interest once more this month.

And whereas the prospect of quickly falling inflation ought to cut back monetary strains dealing with households, actual incomes are more likely to nonetheless fall over most of this yr. Subsequently, the chance of a sustained correction in home costs hasn’t gone away.”

Hopes that the Financial institution of England might quickly cease elevating rates of interest are supporting demand for house purchases, studies Victoria Scholar, head of funding at interactive investor:

Over the previous eight months, the housing market has been trying to regain a way of normality after the chaos round September’s mini price range which despatched mortgage charges hovering and potential householders fleeing from the market.

With mortgage charges since easing, the Financial institution of England close to the height of the speed mountaineering cycle, client sentiment bettering, and inflation seen easing this yr, mortgage purposes have began to choose up once more with patrons cautiously coming again.

Spring tends to be a seasonally busy interval for housing market exercise because the improved climate brightens demand and attracts in additional sellers forward of the summer time vacation lull.”

The BoE is extensively anticipated to raise Financial institution Fee once more this month, from 4.25% to 4.5%, with charges seen approaching 5% earlier than the tip of this yr. However they’re then forecast to drop in 2024.

Up to date at 02.56 EDT

April breaks 7 consecutive months of home worth falls with a 0.5% subdued “spring” in its step. Regardless of this home worth progress stays detrimental at -2.7% in April, leaving costs 4% beneath their Aug 22 peak @AskNationwide pic.twitter.com/FXtV7pBRxM

— Emma Fildes (@emmafildes) Might 2, 2023

Matt Thompson, head of gross sales at Chestertons, studies that April was a busy month.

“Savvy home hunters used the Easter holidays to proceed their search on-line and enquire about properties to rearrange a viewing as quickly as attainable. April has due to this fact been a busy month; notably as patrons are much more conscious of in the present day’s aggressive market situations.

In consequence, most patrons have additionally been making ready their paperwork as a lot as they might in an effort to make a proposal and safe a property earlier than the summer time.”

‘Reverberations from the mini-Funds are fading’

April’s rise in UK home costs exhibits that the reverberations from the mini-Funds that shook the UK property market are fading, says Tom Invoice, head of UK residential analysis at Knight Frank:

Value declines are bottoming out and lots of patrons have accepted the brand new regular for mortgage charges as stability returns to the lending market.

Boosted by financial savings amassed in the course of the pandemic, report ranges of housing fairness and a powerful jobs market, exercise has been strong with out being spectacular this yr. Provide is rising, which can enhance downwards stress on costs however the market is returning to earth moderately than falling off a cliff. Properties that tick all the fitting bins will maintain their worth however among the pandemic froth has disappeared so asking costs will come beneath stress.

Invoice predicts that after a normal election, successive lockdowns, a stamp obligation vacation and the mini-Funds, the UK housing market ought to have its most predictable yr since 2018.

Nonetheless, we don’t count on widespread standoffs over worth due to lingering financial uncertainty and a rising realisation that subsequent yr’s normal election might shake issues up once more. Switched-on patrons and sellers are performing now whereas issues are comparatively uneventful.”

UK home costs: the important thing charts

Listed here are the important thing charts from Nationwide’s home worth report, exhibiting the primary month-to-month rise in costs since final August.

Introduction: UK home costs rise in April after seven consecutive falls

Good morning, and welcome to our rolling protection of enterprise, the world economic system and the monetary markets.

UK home worth progress picked up in April, constructing society Nationwide studies this morning, with the primary month-to-month enhance in seven month.

Common home costs rose by 0.5% final month, Nationwide’s information exhibits, following seven consecutive falls going again to final September.

The common worth elevated to £260,441, up from £257,122 in March.

This has lifted the annual price of home worth progress to -2.7%, from -3.1% in March (the largest fall since 2009), as calm returned to the markets after the chaos of final autumn’s min-budget.

Robert Gardner, Nationwide’s chief economist, studies there have been “tentative indicators of a restoration” available in the market final month, though this nonetheless leaves costs 4% beneath their August 2022 peak.

Gardner explains:

“Current Financial institution of England information means that housing market exercise remained subdued within the opening months of 2023, with the variety of mortgages authorized for home buy in February practically 40% beneath the extent prevailing a yr in the past, and round a 3rd decrease than pre-pandemic ranges.

Nonetheless, in current months business information on mortgage purposes level to indicators of a pickup.

Final month, Rightmove reported that asking costs had been at report ranges:

Gardner says the current pick-up in UK client confidence could also be serving to the housing market, however cautions that….

….any upturn is more likely to stay pretty pedestrian, as it would take time for family funds to recuperate, since common earnings have been failing to maintain tempo with inflation, and by a large margin over the previous couple of years.

Mortgage rates of interest are additionally more likely to act as a headwind. Whereas they’re nicely beneath the highs seen within the wake of the mini-Funds final yr, charges are nonetheless greater than double the extent prevailing a yr in the past.

Additionally arising in the present day

Britain’s largest supermarkets are dealing with requires the UK’s competitors watchdog to analyze claims of profiteering amid the price of dwelling disaster, as meals worth inflation soared to a report excessive in April.

In a single day, Australia’s central financial institution has stunned buyers by elevating rates of interest once more.

The RBA board raised its money price 25 foundation factors to three.85% at its month-to-month assembly on Tuesday, defying buyers who had wager the central financial institution would prolong its pause for a second month.

Greater rates of interest raise income at banks….. comparable to HSBC, which has reported a three-fold bounce in earnings within the final quarter, On a continuing forex foundation, HSBC’s revenue earlier than tax elevated by $9.0bn to $12.9bn, main the financial institution to launch as much as $2bn of share buybacks and a ten cent-per-share dividend.

BP has defied an easing in power costs to submit one of many largest first-quarter income in its historical past, reigniting a debate over windfall good points by oil and fuel companies.

The power big stated its underlying income hit $5bn (£4bn) within the first three months of the yr, outstripping analysts’ forecasts. Extra on this shortly…

The newest manufacturing facility PMI studies will present how producers within the UK and the eurozone fared in April. That follows a shock contraction in China’s manufacturing facility output, reported on Sunday.

We get the most recent eurozone inflation report this morning, with costs anticipated to have risen by 7% within the 12 months to April, up from 6.9%. Core inflation may stick at 5.7%, worryingly excessive for the European Central Financial institution.

The agenda

7am BST: Nationwide home worth index for April

9am BST: Eurozone manufacturing PMI for April

9.30am BST: UK manufacturing PMI for April

10am BST: Eurozone core inflation price on April

3pm BST: US Manufacturing facility Orders for March

Up to date at 02.57 EDT

{kind=link}