DNY59

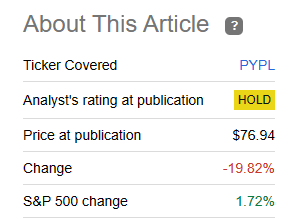

In our final article on PayPal Holdings Inc. (NASDAQ:PYPL), we gave the drained bulls some excellent news and a few unhealthy information.

The excellent news is that PYPL does have a good valuation. 4.3% adjusted free money move yield or 23 instances GAAP earnings are literally very good valuations relative to what insanity transpired over the markets within the final 2 years. The unhealthy information is that it isn’t remotely low sufficient when you perceive the historical past of bubbles. Bubbles finish with excessive undervaluation and we aren’t there but.

Should you embrace that forecast, one of the best ways to play it’s to promote money secured places at $60 or decrease strikes, after the inventory takes tough tumble. We fee this a maintain at current. Marrying our pondering on PYPL with our outlook in the marketplace, makes us imagine {that a} long run shopping for alternative will current itself in late 2023.

Supply: One Of The Greatest Values In Development

Refusing to purchase the inventory paid off as soon as once more and PYPL headed sharply decrease after what seemed to be a good quarter.

One Of The Greatest Values In Development

We have a look at the Q1-2023 numbers and let you know why we’re extra optimistic for returns from right here however usually are not prepared to purchase simply but.

Q1-2023

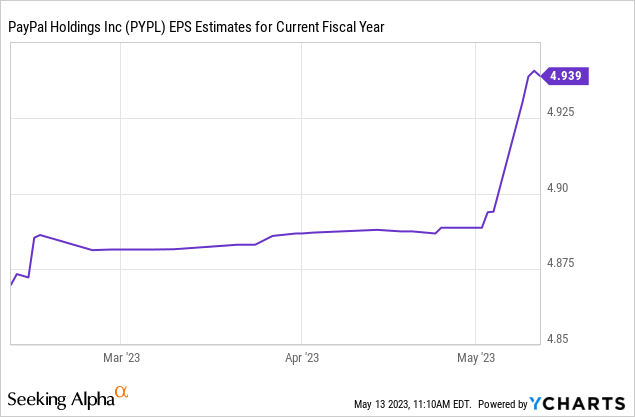

Q1-2023 delivered each revenues and earnings that have been higher than anticipated. Now, within the final 6 months we have now had no scarcity of the analysts neighborhood downgrading estimates to assist setup “beats”. This was not the case for PYPL although. Earnings estimates have been comparatively flat happening and the analyst neighborhood was not pitching any favors. You’ll be able to see that within the chart under. The massive bump up got here after the outcomes.

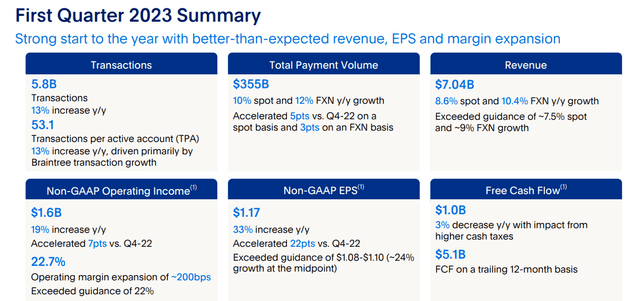

So PYPL did a kind of true earnings beats and numbers have been additionally far forward of the place we thought they might land.

PYPL Q1-2023 Presentation.

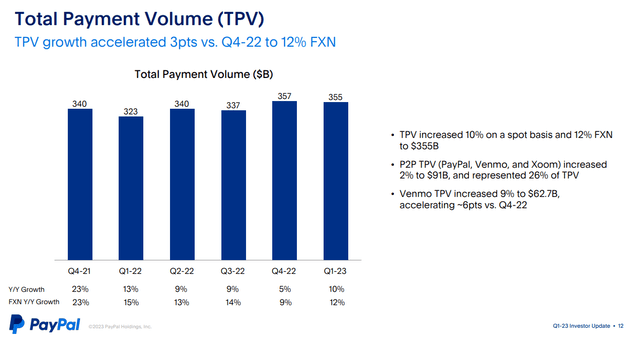

Complete fee quantity was up by 10% and 12% when you took out foreign exchange affect.

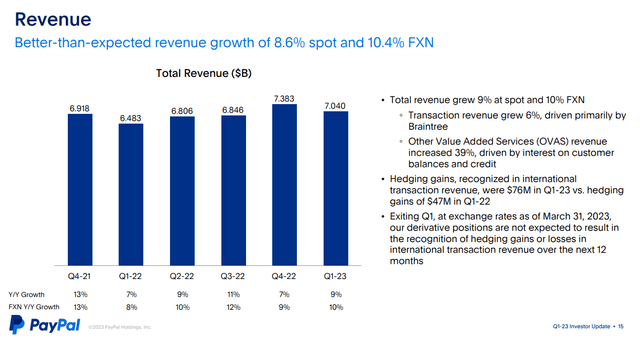

PYPL Q1-2023 Presentation.

Income development which tends to comply with the above metric (although not at all times completely), additionally got here in the identical ballpark.

PYPL Q1-2023 Presentation.

Should you appeared round for corporations which might be uncovered to the identical quantity traits on shopper spending, you didn’t get significantly better than this. Visa (V) for instance confirmed income positive aspects of 11% and fee quantity development of 10% for his or her quarter ended March 31, 2023 (observe that it’s their fiscal Q2). Visa inventory is up fractionally since then.

VISA Q2-2023 Outcomes

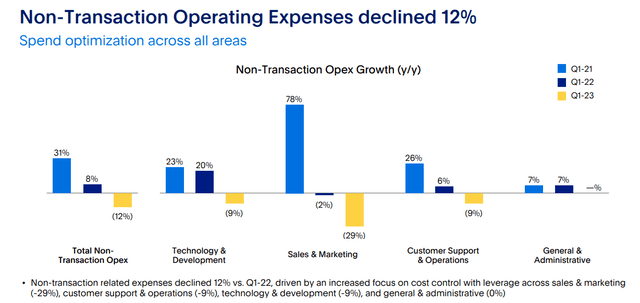

PYPL did properly right here relative to what anybody anticipated and matched that income development with a decline in non-transactional bills.

PYPL Q1-2023 Presentation.

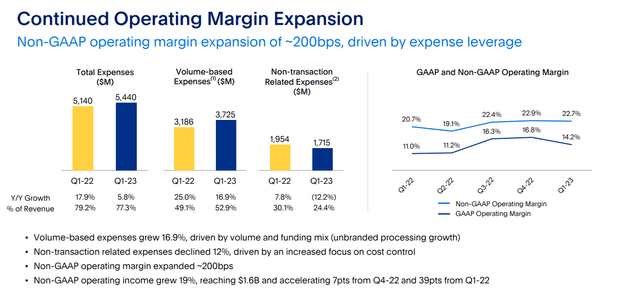

The margin enlargement once more proved the bears improper and PYPL is leveraging its enterprise fairly properly at this level within the cycle.

PYPL Q1-2023 Presentation.

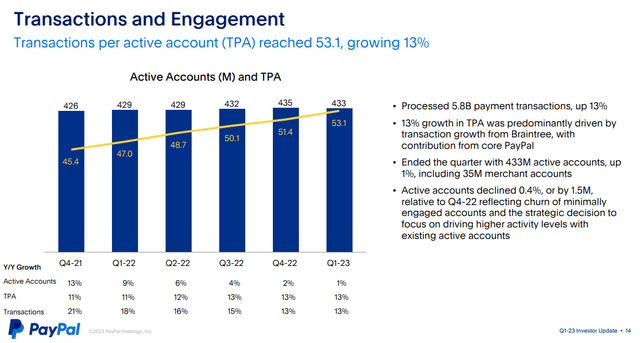

If there was one small piece of bear fodder, it got here from complete lively accounts. There was a small drop to 433 million from 435 million.

PYPL Q1-2023 Presentation.

One might argue that this was greater than offset with transactions per account rising 13%. However that is the distinction between bull runs and bear runs. In the course of the former the slightest optimistic information is embraced to blow extra air right into a bubble. If there was information about PYPL increasing into Moldova, then buyers could be completely satisfied so as to add that nation’s GDP equal to PYPL’s market cap. Why not, proper? In the course of the latter you are able to do all the things proper and nonetheless get punished mercilessly. This was the important thing piece that acquired many analysts to begin taking down their purchase scores. It appears foolish and even illogical however the inventory they felt was a purchase at $300, is now a promote at $60, though each valuation metric has improved by leaps and bounds.

Outlook

In case you are anticipating the discover the affect of analyst downgrades within the earnings space, you’re out of luck. Earnings are anticipated to go up at a robust double digit fee for 2024 and 2025

Searching for Alpha

In reality, it’s uncommon to see so many “up revisions” to earnings alongside a tanking inventory.

PYPL Q1-2023 Presentation.

So if you wish to say this is unnecessary, we’re with you there. If there’s a bear leg to the PYPL thesis, it’s that we actually need to cease this foolish non-GAAP quantity dialogue. That 12X earnings what folks seek advice from comes from the adjusted earnings estimates. GAAP numbers are nonetheless fairly poor as compared. PYPL nonetheless trades at 18X GAAP numbers.

PYPL Q1-2023 Presentation.

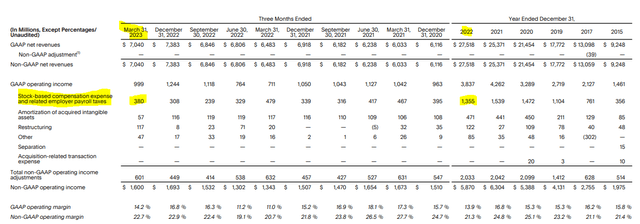

The majority of this GAAP to non-GAAP differential comes from inventory primarily based compensation. You’ll be able to see the close to $400 million of quarterly expense for this quantity in non-flashy slides on the finish of the PYPL presentation.

PYPL Q1-2023 Presentation.

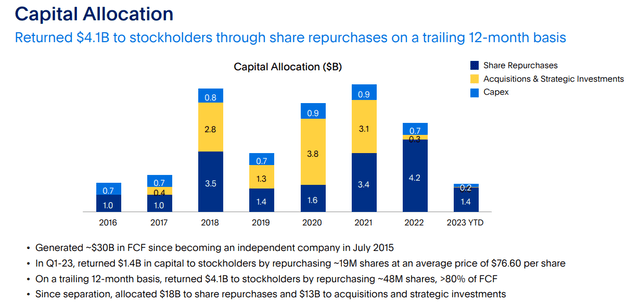

This traits to shut to $1.5 billion yearly after which PYPL turns round and makes use of its “free money move” to purchase again the identical inventory. So that is the principle gripe that bears and people sitting on the fence (like us) have with the PYPL mannequin.

PYPL Q1-2023 Presentation.

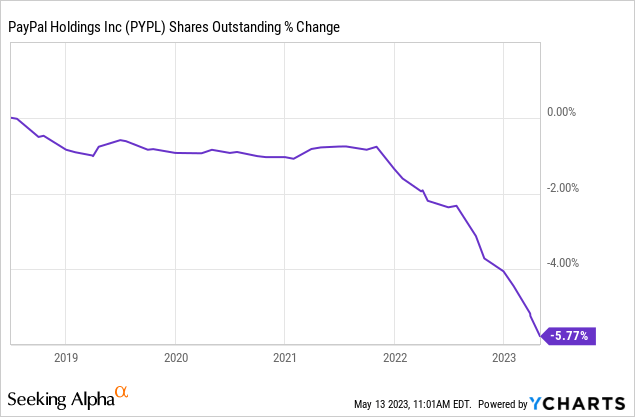

Heck, even they admit it right here when you look carefully sufficient on the slide above. PYPL has spent $18 billion on share repurchases since separation. Complete share rely was basically flat between 2018 and finish of 2022 for PYPL. It was solely after 2022 that the share rely began declining.

In order that interval between 2018 and 2022 was the timeframe of extraordinarily poor capital allocation as PYPL purchased again its inflated inventory to offset inventory primarily based compensation. Solely when the value declined sufficient relative to its free money move, did PYPL begin making a dent in its shares excellent.

Verdict

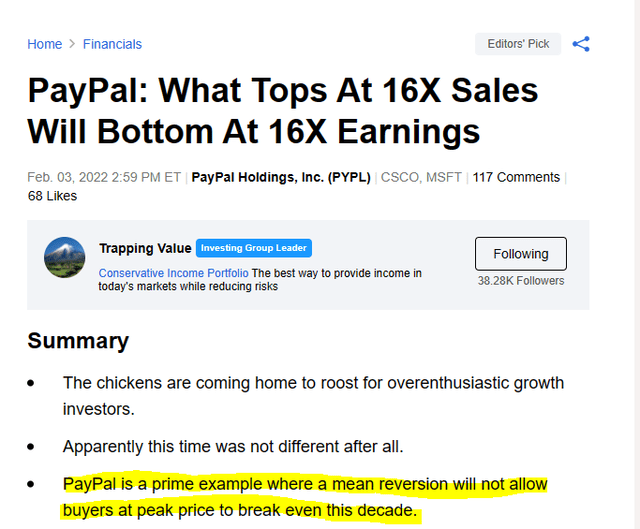

We want we might let you know that you might go hand over fist right here however the valuation remains to be demanding. Sure you may have development however with out new accounts exhibiting up, you’re more likely to begin monitoring nominal GDP for income development. We might not put 18X GAAP earnings within the class of low-cost for such shares. We would definitely not put it as low-cost after we imagine a recession is shut by. We had beforehand used this title with out the “GAAP” included.

What Tops At 16X Gross sales Will Backside At 16X Earnings

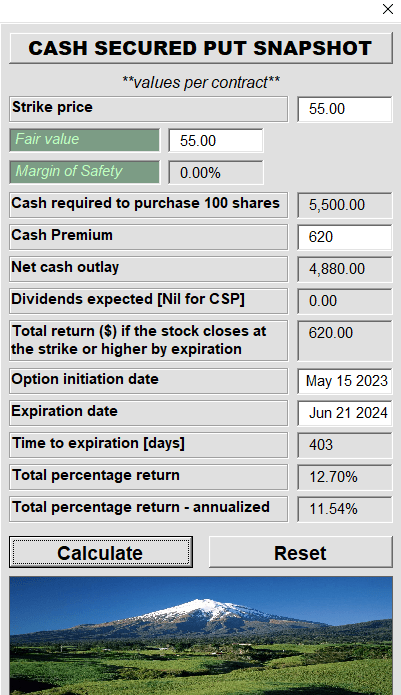

In fact, since then inflation has confirmed extra persistent and rates of interest have headed far greater. In such an surroundings, we might look for no less than 16X GAAP earnings because the purchase level. We’re shut right here to a major backside and one that can reward the affected person patrons. If we have been compelled to choose a play right here it could be to goal for the $55 strikes on longer dated money secured places.

Writer’s App

The margin of security is appropriate and it supplies a stable revenue for ready.

Please observe that this isn’t monetary recommendation. It could appear to be it, sound prefer it, however surprisingly, it isn’t. Traders are anticipated to do their very own due diligence and seek the advice of with an expert who is aware of their goals and constraints.

{kind=link}