DakotaSmith/iStock Editorial by way of Getty Pictures

Introduction

The truck manufacturing business has undergone some modifications lately, as three most important gamers had been spun-off from different conglomerates targeted on automobile manufacturing. Due to this fact, up till these spin-offs, traders may put money into truck producers solely by buying both Volvo Group (OTCPK:VLVLY, OTCPK:VOLAF) or PACCAR (PCAR). Now, there are three extra gamers which might be publicly traded: Traton (OTCPK:TRATF, OTCPK:TRATY), Iveco Group (OTCPK:IVCGF) and Daimler Truck (OTCPK:DTRUY, OTCPK:DTGHF).

The explanation for these spin-offs is kind of clear. Whereas being half of a bigger conglomerate, these three corporations weren’t as worthwhile as the opposite two gamers. Whereas the latter reported stable outcomes with double-digit margins, the previous was barely worthwhile.

Since they’ve been despatched to face on their very own, these corporations have to execute their enterprise in a greater means. I stored on monitoring the progress of the three, and after a 12 months, I noticed that Daimler Truck is on its means to depart behind the opposite two gamers and meet up with the main two. For this reason I lately initiated a small place within the firm that {couples} my funding in Volvo Group. There’s, the truth is, sufficient proof to point out our economies cannot do and not using a rising use of trucking. On this atmosphere, Daimler Truck is an business chief, particularly in North America, that has but to be detected by many traders’ radars and search instruments.

On this article, I want to undergo the newest earnings report to know if the corporate retains on being on monitor or not.

Q1 Earnings Report

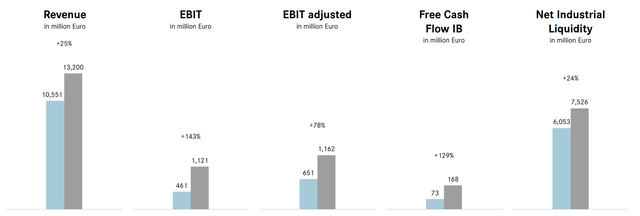

Daimler Truck launched its earnings report for the previous quarter and disclosed these most important information:

unit gross sales in comparison with prior-year’s quarter elevated by 15% to 125,172 items (Q1 2022: 109,286). as a consequence, income rose by 25% to €13.2 billion (Q1 2022: €10.6 billion). unsurprisingly, adj. EBIT elevated by 78% to €1,162 million within the reporting interval (Q1 2022: €651 million). internet revenue got here in at €795 million (Q1 2022: €275 million). industrial free money stream was up 129% YoY to €168 million (Q1 2022: €73 million). This had an influence on return on gross sales (margin) reached 8.8% (Q1 2022: 5.9%)

To assist us visualize these knowledge, we will use the slide Daimler Truck confirmed throughout its earnings presentation. In gentle blue we’ve the outcomes of the identical quarter in 2022, in gray we see this previous quarter’s outcomes.

Daimler Truck Q1 2023 Outcomes Presentation

General, we’re earlier than a development exhibiting a rising and increasing firm. To assist who’s studying, let me give just a little clarification about one knowledge: industrial FCF. Often, corporations reminiscent of Daimler have a seasonality the place they construct up stock within the first quarter(s) of the 12 months. This results in poor, if not unfavorable FCF. The very fact Daimler Truck greater than doubled its FCF this quarter reveals how its operations have gotten as soon as once more easy with much less provide chain hiccups.

With the ability to generate constructive money stream, the corporate is initiating an annual dividend paying 40% of the corporate’s internet revenue. This 12 months, on July 21, the corporate will thus pay a dividend of €1.3 per share. This can be a 4.4% yield, however be mindful the German withholding tax on dividends is round 26%.

Now, these outcomes had been extensively anticipated for 2 causes. To start with, many equipment manufacturing are releasing outcomes which have simple comparables. I consider Deere (DE), although in one other business, defined the scenario in a transparent means: in Q1 2022, on account of provide chain disruptions, many producers had been, on one aspect, growing their inventories due to unfinished supplies (thus damaging the general free money stream), on the opposite, the automobiles that had been being shipped had been offered with 2021 costs. For this reason the primary half of 2023 will see, typically talking, a couple of of those corporations with blow-out outcomes.

Consequently, these manufacturing corporations are certainly now harvesting the outcomes many different corporations achieved final 12 months on the peak of the post-Covid restoration.

Due to this fact, since investing makes use of previous outcomes to forecast what may come subsequent, we have to ponder two elements:

In a positive atmosphere, is Daimler Truck performing consistent with its friends or is it outperforming them when it comes to monetary outcomes? How is Daimler Truck order guide doing?

Daimler Truck is enhancing its profitability

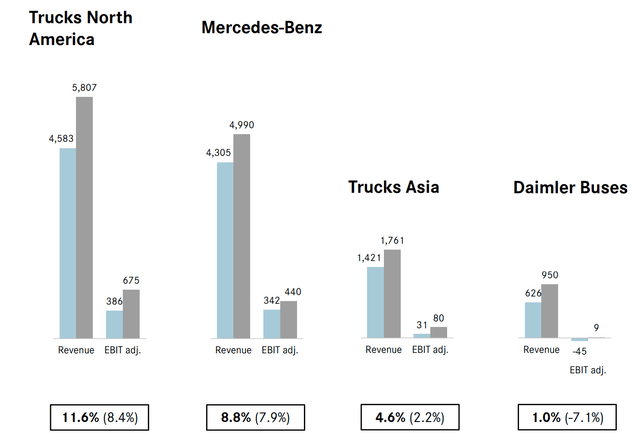

To reply the primary query we’ve the help of two completely different knowledge that we will evaluate. To start with, we all know Daimler Truck declared that its spin-off was aimed toward reaching double-digit margins.

As a matter of reality, we all know from the report how worthwhile every section of the corporate is. We see how Vans North America is already properly above 10% when it comes to margins. Mercedes-Benz, which covers Europe, is getting nearer to this threshold, although it’s not there but. The 2 smaller segments are enhancing, too, with Asia greater than doubling its margins and buses turning into worthwhile as soon as once more after the pandemic.

Daimler Truck 1Q 2023 Outcomes Presentation

Certainly, among the many three corporations lately spun-off, Daimler Truck has been extra worthwhile than its two different friends Traton and Iveco for the reason that starting. Nonetheless, we have to acknowledge that Traton’s latest quarterly report was forward of expectations and introduced the corporate to a 8.4% return on gross sales that comes near Daimler Truck’s 8.8%. Nonetheless, Traton continues to be largely depending on Scania (1Q income of €4.17 billion with 13.3% RoS), whereas Navistar, its North-American model continues to be a lagger (€2.74 billion in income and 6.3% RoS) in comparison with Daimler Truck’s North-American section the place Freightliner and Western Star making up collectively € 5.8 billion in income for the quarter with a 33% market share within the heavy-duty truck section.

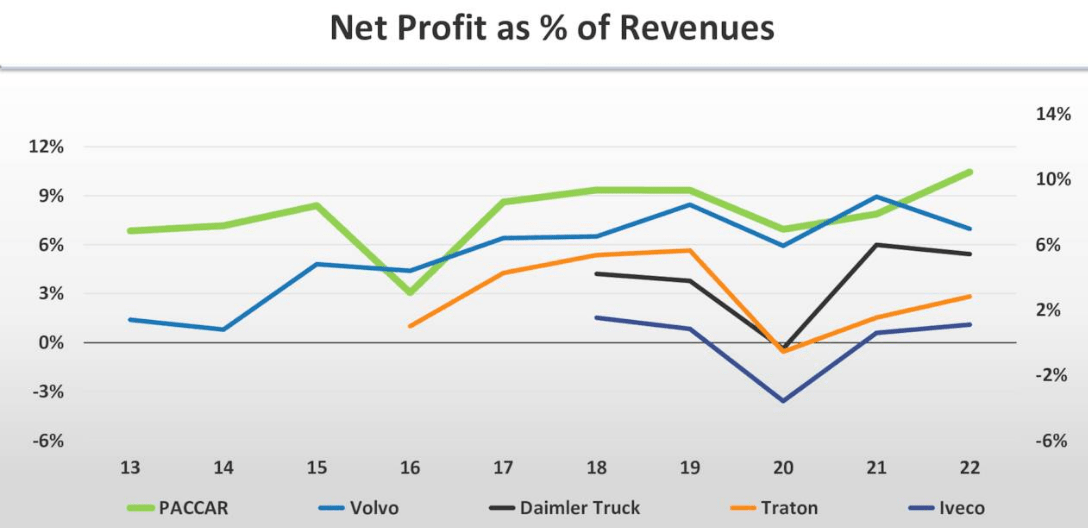

To assist us visualize how Daimler Truck appears to be racing at a quick velocity to hitch the 2 main corporations within the business, we will use this graph taken from a direct competitor, Paccar. Right here we see how, for the reason that pandemic, Daimler Truck has been capable of depart Traton and Iveco behind, whereas catching up with Paccar and Volvo.

Paccar Q1 2023 Outcomes Presentation

The velocity Daimler Truck confirmed in its execution is among the information that made me provoke a place within the inventory, forecasting we are going to see that firm obtain its double-digit aim over the following two years.

Revenue orders

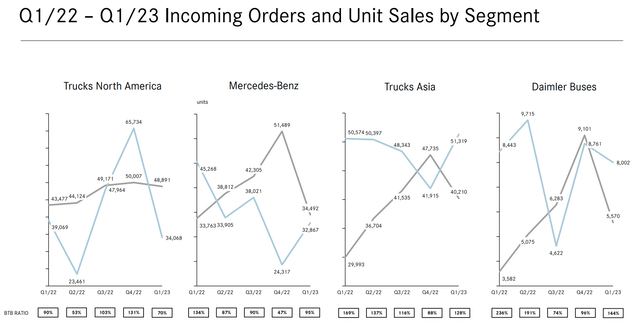

We’ve got already seen how robust gross sales had been to be anticipated. However the query is: can these ranges be sustainable? To reply we have to understand how order consumption is performing. Daimler Truck is kind of clear when talking of this metric and it permits us to watch quarter after quarter the book-to-bill ratio.

Daimler Truck 1Q 2023 Outcomes Presentation

In gentle blue, we see incoming orders in gray unit gross sales. We see how North America orders decreased sharply by nearly 50% QoQ but when we zoom out and take a look at the identical quarter previously 12 months, the decline is a bit over 10%. That is acceptable, contemplating how 2022 was an distinctive 12 months when it comes to demand for equipment normally. Mercedes-Benz appears to be recovering QoQ, though it’s properly beneath its Q1 2022 highs. Nonetheless, Vans Asia and Daimler Buses are nonetheless on restoration mode and partially offset the order consumption decline within the Western world. This reveals a well-diversified firm.

Nonetheless, we’d like additionally to think about one facet which isn’t proven by these numbers. Final 12 months, seeing robust inflationary stress, many producers, beginning with Volvo Group, determined to limit their order books with the intention to hold them beneath management when it comes to value administration and margin safety. Daimler Truck did this, too. In actual fact, over the past earnings name we heard its administration state that

“Demand for vehicles in each of our Industrial segments remained on a really robust degree because the pent-up demand in all our key areas continues to be excessive. That is clearly seen within the demand and gross sales of our merchandise in addition to in our nonetheless excessive order backlog.

In our key areas, we’re kind of offered out for this 12 months. Whereas the availability chain actually has improved in comparison with final 12 months, we nonetheless have challenges and we nonetheless anticipate some extra periodic provider shortages affecting manufacturing. Nonetheless, we’re changing our growing unit gross sales into robust financials.”

In different phrases, though we see demand a bit down this 12 months, it’s nonetheless excessive sufficient to have the corporate already booked for the rest of the 12 months. I’ve been saying for a lot of months that this example might lead many cyclical corporations reminiscent of Daimler Truck to reside the expected-to-come gentle recession in a novel means. Whereas this gentle financial pullback ought to happen, these corporations will probably be targeted on fulfilling their orders and shortening their lead time. In the meantime, a recession of a few quarters might go by with out these corporations nearly noticing it. As demand picks up once more, they might be prepared to satisfy it with out the availability chain disruptions we noticed final 12 months.

As well as, Daimler Truck appears to be studying Paccar’s lesson. The latter, the truth is, is well-known as a frontrunner when it comes to monetizing its truck base via after-sale service and spare components gross sales. Daimler Truck simply introduced it’s going to do one thing related in Europe, too, with Mercedes-Benz Vans organising central logistics hub for the worldwide provide of spare components. A brand new hub, the truth is, will probably be in-built Halberstadt, Saxony-Anhalt and it ought to be capable to ship, as defined throughout the earnings name, “as much as 300,000 completely different gadgets to nearly 3,000 automobile sellers in over 170 nations world wide”.

Conclusion

Given these outcomes, I nonetheless see it cheap for an organization whose development in profitability is prone to begin buying and selling at a bit greater multiples. In my previous protection, I ran my discounted money stream mannequin and gave a goal worth of €39. Given the newest outcomes and a forecast that sees the corporate reaching a margin round 9%, the corporate continues to be buying and selling round 51% decrease than the sector common. Contemplating the corporate is catching up with Paccar and Volvo, it might be anticipated to commerce at a better fwd PE in comparison with the present 7 it’s being given by traders. Daimler Truck is predicted to do round €55 billion in income this 12 months. With a internet revenue margin of 9% we’re speaking a few internet earnings of just about €5 billion. Divided by present market cap of €23.7 billion we’re speaking a few fwd PE beneath 5, which I think about low, contemplating the multiples Paccar and Volvo are buying and selling at. Due to this fact, I hold my purchase ranking and my goal worth of at the very least €39 per share, which equals to a potential 34% upside.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}