Pgiam/iStock by way of Getty Photos

Funding Thesis

Argan, Inc. (NYSE:AGX) is properly positioned to capitalize on the rising demand from the worldwide transition to zero carbon emission. Along with the robust demand, the corporate’s sturdy undertaking backlog is predicted to contribute to elevated income year-over-year within the coming quarters. Moreover, the corporate is at present buying and selling at a reduction with its 5-year common EV/EBITDA ratio. Given the promising progress prospects and a decrease valuation relative to historic developments, I maintain a bullish outlook on this inventory.

Enterprise Overview

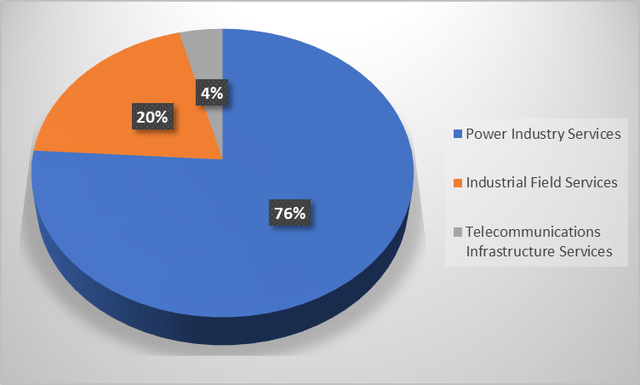

Argan, Inc. operates via its wholly owned subsidiaries, specifically Gemma Energy Programs (GPS), Atlantic Tasks Firm Restricted (APC), The Roberts Firm (TRC), and Southern Maryland Cables, Inc. GPS and APC symbolize the ability business companies section of the corporate, providing a complete vary of companies together with engineering, procurement, building, commissioning, upkeep, undertaking improvement, and technical consulting to the ability era market, together with the renewable power sector. TRC, however, focuses on industrial fabrication and gives on-site companies to assist the development of recent crops, facility expansions, upkeep turnarounds, shutdowns, and emergency mobilizations for industrial crops. Lastly, SMC which represents the telecommunications infrastructure companies section of AGX, gives undertaking administration, building, set up and upkeep companies to industrial, native authorities and federal authorities prospects.

AGX’s segment-wise income (Investor presentation)

Sturdy Trade Tailwinds

In response to current estimates by McKinsey Vitality Insights World Vitality Perspective, the worldwide transition to reaching web zero carbon emissions by 2050 is anticipated to value $275 trillion. This transition entails a considerable discount of a further 70% in coal-fired energy era methods from 2022 to 2050. As of 2022, coal-based power accounts for round 20% of complete electrical energy era. Nevertheless, it’s anticipated to say no considerably to five% by the yr 2050. In response to the rising want for electrification and alternative of coal-power era, there may be an anticipated enhance within the utilization of pure gasoline and renewable power sources within the upcoming years. Pure gasoline demand is predicted to expertise a progress of 10% inside the subsequent decade, whereas renewables are anticipated to contribute to 50% of the ability combine by 2030 and a staggering 85% by 2050. Contemplating Argan’s experience in designing and developing large-scale power tasks, I’m assured that the corporate is in an advantageous place to capitalize on the rising demand ensuing from the worldwide power transition.

Energy In Backlog

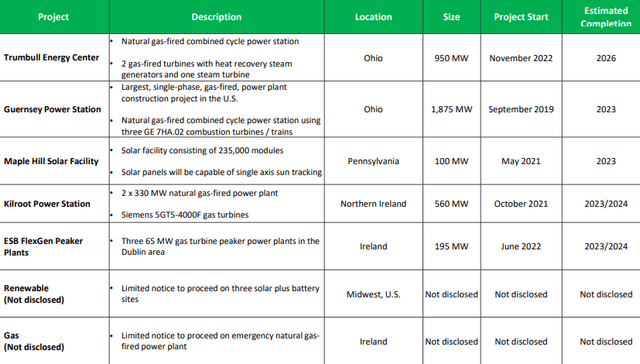

As of thirty first January 2023, Argan’s undertaking backlog stood at $822 million, a rise of 15% Y/Y. Notably, the ability section contains a considerable 85% of the entire backlog, showcasing the presence of a number of important tasks. Because the Guernsey Energy Station and the Maple Hill Photo voltaic Facility strategy completion, it’s anticipated that their income ought to lower year-over-year within the coming quarters. Nevertheless, I anticipate an increase in income from the Kilroot Energy Station and the ESB FlexGen Peaker Vegetation. These tasks are at present working at or close to their peak exercise ranges. Moreover, the Trumbull Vitality Centre, which remains to be in its early levels of building, is projected to contribute to elevated income for AGX within the coming quarters. Consequently, with a strong undertaking backlog in place, I firmly imagine that the corporate is poised to attain improved top-line outcomes year-over-year in FY2023.

AGX’s Venture Backlog (Investor presentation )

Lengthy-Time period Worth Creation

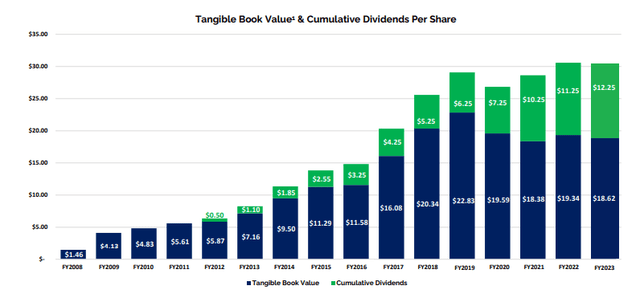

Argan has persistently prioritized long-term worth creation for its shareholders. Often, the corporate’s quarterly outcomes might seem a bit lumpy, however that is primarily attributed to the timing of contracts and the inherent nature of its enterprise. On the outset of a undertaking, money influx is often greater on account of prepayments acquired on the contract’s graduation. However, because the undertaking advances into its later levels, money outflows are likely to surpass money inflows. The unstable efficiency of shares like AGX typically raises issues amongst traders. Nevertheless, it is very important notice that regardless of these fluctuations, AGX has showcased progress in its tangible guide worth and cumulative dividends per share.

Tangible guide worth and cumulative dividends (Investor presentation )

Danger

As of January 2022, Argan had a undertaking backlog with a complete worth of ~$800 million. You will need to notice that there’s a risk of undertaking cancellations or modifications, which might cut back the quantity of its undertaking backlog and consequently affect the corporate’s revenues and income. Typically, AGX grants its prospects the correct to terminate contracts at their discretion, supplied they compensate AGX for the work already accomplished. Any unanticipated delays, suspensions, or terminations of contracted work might have unfavourable results on the corporate’s total efficiency and inventory market efficiency.

Valuation & Conclusion

Argan is at present buying and selling at an EV/EBITDA (TTM) of 5.10x which is a reduction of roughly 51% with its 5-average EV/EBITDA (TTM) of 10.42x. Furthermore, upon comparability with the sector median of 11.31, the corporate seems to be undervalued. In my evaluation, I discovered that AGX is well-positioned to capitalize on the robust demand arising from the clear power transition within the coming years. Moreover, the corporate’s wholesome undertaking backlog signifies potential income progress within the coming quarters. Contemplating the beneficial progress alternatives and the present valuation beneath its historic common, I’m bullish on this inventory.

{kind=link}