themacx/iStock by way of Getty Photos

We often put up our articles to members of our service 1 week earlier than we publish them to the general public. This text was first printed on Could 29, 2023.

In our funding group, we monitor on a day by day foundation all of the exchange-traded fixed-income automobiles in an try to be most adequately diversified in our portfolios. Selecting the very best in our opinion picks is simply half of the job achieved, the opposite half being eliminating the securities that not provide us some “alpha.” Every so often we discover ourselves in a scenario when all the things we monitor for some merchandise is telling us “promote.”

We imagine that below the present market situations, that is the case with AT&T Inc. (NYSE:T) perpetual fixed-rate most well-liked shares (T-A) and (T-C). With this text, we’ll attempt to defend the thesis why, in our opinion, an investor ought to take into account closing their lengthy positions in these merchandise. It isn’t solely the truth that these funding automobiles don’t have anything to supply, on a relative foundation, as upside potential. The whole lot we thought-about about them is displaying us that they’re approach overvalued within the fixed-income universe and have big depreciation potential.

Furthermore, it’s weird for T-A and T-C (Ba1 by Moody’s) to commerce at yields just like the yield of the most secure exchange-traded most well-liked inventory GDV-H (Aa3 by Moody’s) when there’s apparent misery for the frequent inventory of the corporate. We strongly imagine that phrases have which means and that “high-yielder” ought to yield approach increased than the highest credit-rated investment-grade most well-liked inventory. So allow us to dive into the evaluation that follows.

The frequent inventory of AT&T

AT&T is among the world’s largest telecommunications corporations by income and one of many three largest suppliers of cell phone providers in the US. The corporate is offering providers for fairly a very long time and has established itself as one of many reliable names within the business.

Inventory Chart (Sterling Dealer)

Regardless of how massive, outdated, or well-renowned an organization is, it’s not insured towards a tough time. The downtrend within the value of the frequent inventory T for the final couple of years is apparent from the buying and selling graph posted. We settle for that the market may very well be unsuitable in pricing a inventory occasionally however such a long-term depreciation often is an indicator of a gentle decline within the curiosity of most people.

One other indicator apart from the value motion that we monitor is the Worth to Earnings ratio for the frequent inventory of the corporate. AT&T’s P/E ratio as of Could 25, 2023, is 6.47. Now it is a quite low quantity that may be interpreted by the traders in two other ways, relying on their private understanding of the scenario:

Together with the buying and selling graph above one can count on such a small worth for the P/E ratio to point a troubled firm with a standard inventory that can’t appeal to traders regardless of the very enticing earnings it provides them. That, in our opinion, means dangerous information for the popular shares holders. There may be actually no logical monetary purpose for such most well-liked shares to be priced at related yields to the very best credit-rated investment-grade securities traded on the alternate. One other approach to take a look at AT&T’s P/E ratio is to treat it as an awesome mispricing and a chance to go lengthy the frequent inventory. An organization that may finance its debt with investment-grade bonds (BBB rated by S&P) ought to commerce with a quite increased worth for its P/E ratio. This sort of interpretation has its personal deserves, however it means nothing for the popular shares. Once more, there isn’t a sound clarification for the 5.7% CY of T-A and T-C.

T-A and T-C

As talked about above, AT&T has two fixed-rate perpetual exchange-traded most well-liked shares – T-A and T-C:

Most popular inventory data (proprietary software program)

The popular shares of AT&T are rated two notches decrease than its exchange-traded notes (“ETNs”) TBB and TBC and have a credit standing of BB+ from S&P. This can be a fairly customary credit score analysis of the popular shares in comparison with the unsecured debt of an organization. So, in keeping with S&P the debt of AT&T is investment-grade, however the prefs are high-yielders. As a normal rule, two notches distinction within the credit standing means round 0,5% yield distinction. But T-A and T-C commerce at CY just like the YTM of TBB and TBC. It’s past our comprehension why the market loves equally the popular shares and the debt of a troubled firm.

A typical process when evaluating a fixed-income safety yield is to check it to its benchmark bond yield and examine if there are some deviations. For perpetuity, that is the 30-years Treasury bonds. The logic behind that is that safety is pretty priced at its IPO. Within the means of IPO, the safety is evaluated completely by top-tier professionals, and the credit score unfold it receives to its corresponding benchmark at that second is of key significance for future evaluations.

credit score unfold dynamics (proprietary spreadsheet)

Within the desk above, we’ve got calculated the credit score unfold at IPO and on the present second for the 2 most well-liked shares which are of curiosity to us right this moment – T-A and T-C. These are quite easy calculations that give us a transparent end result – the credit score unfold for each revenue automobiles has narrowed by 1%. For the three+ years for the reason that IPOs of those securities, the benchmark charge has a double enhance in worth. If all the things associated to the corporate stays the identical for that time period, the credit score unfold of its securities ought to widen. Effectively, clearly not all the things has been the identical with the corporate – its frequent inventory presently is buying and selling at half the value it did on the time of the IPOs. So for these 3 years, one thing occurred to AT&T that worn out half of its worth, and concurrently with this made its most well-liked shares safer securities.

At this level, I can hear you asking “What sort of sorcery is that this?” and let me inform you – it’s a simply query. For us, there’s an evident market mistake within the present pricing of T-A and T-C and they need to commerce at approach increased yields. In line with our understanding, the credit score unfold narrowing alone is a sign that T-A and T-C usually are not priced proper. That together with AT&T’s frequent inventory conduct and a P/E ratio of 6.5 is giving us a robust “promote”/”go brief” sign on its most well-liked shares.

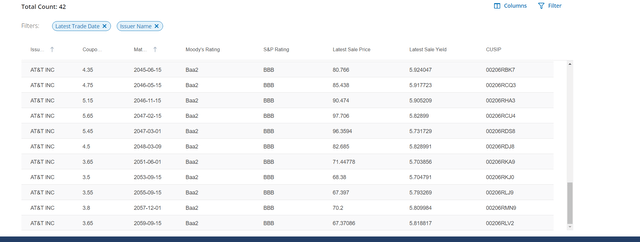

The Bonds

AT&T Bonds (Finra)

These are the long-term bonds of the corporate which are rated BBB and have yields within the vary of 5.7% – 5.9%. Similar to the exchange-traded: Child bonds:

Child Bonds of AT&T (proprietary software program)

In keeping with the popular shares, the newborn bonds have additionally narrowed their spreads:

Child Bonds credit score unfold dynamics (proprietary spreadsheet)

New ALL IPO

On the finish of this brief evaluation, we wish to flip your consideration, for comparability functions solely, towards the brand new Allstate Company IPO. ALL-J (ALL.PJ) might be BBB rated by S&P perpetual most well-liked inventory with a 7.375% mounted nominal yield. Allstate has at all times been a first-rate issuer and if it can not finance its operations at decrease prices for the time being which means no approach AT&T can. We imagine that T-A and T-C sooner quite than later may have a actuality examine and regulate their yields to extra sufficient, increased ranges.

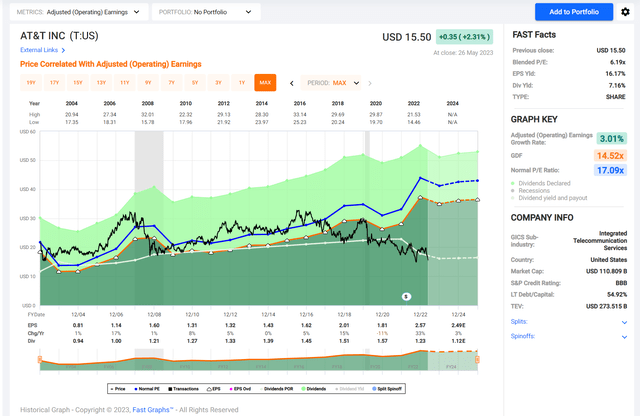

The best way to benefit from the scenario

All of it will depend on the attitude and in your private understanding of the scenario. If one believes the mounted revenue market is appropriate about AT&T, then the T frequent inventory has by no means offered such an apparent mispricing as a a number of to the working earnings:

T inventory historic efficiency (Fastgraphs)

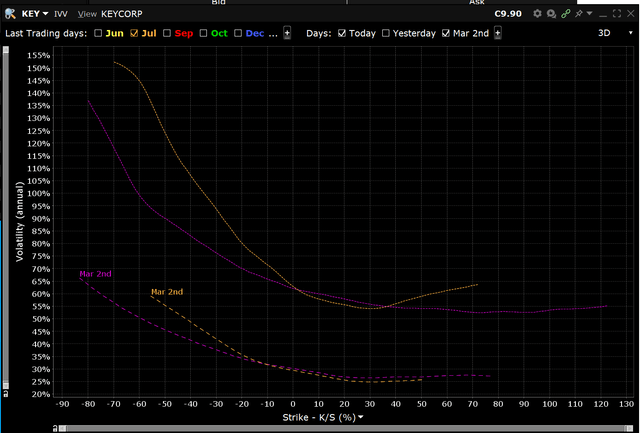

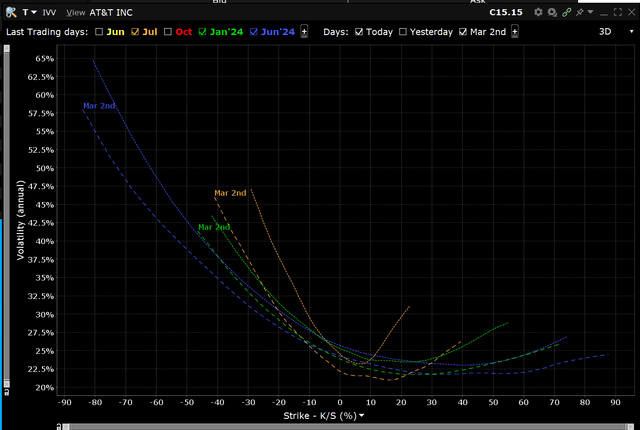

If the analysts are appropriate of their prognosis for the longer term, you’ve the uncommon probability to spend money on such an iconic firm at near 16% earnings yield. This can be a primary would count on from a distressed firm. One additional constructive for the investor in AT&T is the truth that the implied volatility for the frequent inventory has been fairly steady regardless of the horrible inventory efficiency. Right here is how the Implied volatility modifications when there’s a downside:

Implied volatility instance (Interactive Brokers)

Right here is similar chart however for T

AT&T implied volatility (Interactive Brokers)

Plainly the market has not risen its expectation for a pointy decline within the firm’s value. Whereas the popular shares, the bonds, and the IV of the corporate usually are not signaling any downside. one must be very tempted to purchase the frequent inventory as a result of it is rather uncommon to have the ability to purchase these Buffet-like corporations cheaply. In fact, as merchants of mis-pricings, we want the much less apparent commerce. As talked about earlier, the credit score unfold of the popular shares is at historic lows and we see quite a lot of worth in buying and selling its widening. The best approach to do this is to guess on the widening by way of some unique CDS product on the popular inventory. We shouldn’t have such a product accessible for buying and selling and the one commerce we are able to make out of that is to be lengthy the same length treasury bond whereas shorting the popular inventory. To some extent, this commerce is just like what Invoice Ackman did in 2020.

Abstract

Based mostly on the popular shares, child bonds, implied volatility, and the entire yield curve of AT&T Inc., we are able to conclude that it is a sound investment-grade firm with no vital credibility points forward. The narrowing of the credit score spreads, suggests improved credibility and a market keen to finance the underlying enterprise at a lower-than-usual credit score premium.

As it’s arduous for us to know the longer term, we solely spotlight the apparent convergence between the AT&T Inc. frequent inventory value conduct and the way the danger premiums have narrowed. It is among the only a few conditions the place the corporate’s frequent inventory appears to be undervalued compared to the popular inventory, all else being equal.

{kind=link}