artoleshko/iStock through Getty Pictures

Introduction

Popping out of the pandemic, the Federal Reserve raised rates of interest at an unprecedented tempo. Over the course of about 15 months, the federal funds price was raised to five.25%, a degree not seen since the Nice Recession. What was unthinkable three years in the past is now a actuality, and it more and more appears to be like as if the times of “straightforward cash” are lastly over. Firms are going through the next price of capital, which places them in danger particularly those that succumbed to the siren songs and took on extreme debt. Debt is just not a nasty factor per se, however with extraordinarily low rates of interest, malinvestments are more and more frequent. Firms are being acquired at ridiculous valuations (e.g., V.F. Corp. (VFC) bought vogue label Supreme for 3.7 instances gross sales), shares are being purchased again at all-time highs (e.g., The Dwelling Depot, Inc. (HD) purchased again $14.8 billion price of inventory at a mean value of $388), and a few firms would rapidly stop to exist with out a regular infusion of capital.

I’ve most likely checked out greater than 100 firms within the final two years and infrequently have I seen one which hasn’t elevated its debt to a kind of vital diploma. On the floor, this appears to be like like a reasonably dangerous setup in an surroundings the place rates of interest are more likely to stay excessive for a big time period. The satan is within the particulars, and it is very important take a detailed take a look at an organization’s debt utilizing quite a lot of metrics. Nevertheless, among the kind of generally accessible ratios can simply be misinterpreted, resulting in false positives or, most likely worse, false negatives.

On this article, I’ll focus on the commonest leverage ratios – how they’re outlined, when they need to be used, and once they can produce deceptive outcomes. Don’t fret, no mathematical equations are used, and in reality, my most well-liked metrics may be defined in a sentence or two and supply illustrative outcomes.

Debt To Property, Debt To Capital

This can be a easy ratio that places debt in relation to an organization’s whole belongings, and is typically additionally known as the gearing ratio. “Debt” refers to all of an organization’s liabilities, akin to interest-bearing debt and different liabilities, however definitions fluctuate. Generally solely funded debt is taken into account. Typically, subtracting fairness from whole belongings yields probably the most conservative model of the ratio as a result of it implicitly takes into consideration all liabilities.

The debt to capital ratio may be considered as a variant of the debt to belongings ratio, since “capital” consists of each debt and fairness. Nevertheless, traders must be cautious to not examine debt to asset or debt to capital ratios from completely different sources, and it is very important know what’s included in debt and capital. For my part, given the simplicity of the method, traders ought to take the time to take a look at the steadiness sheet and calculate the ratios themselves or persist with a single supply.

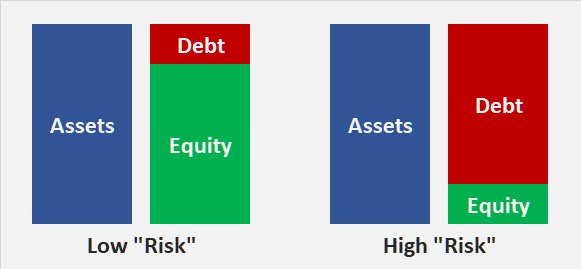

Typically, a low debt to belongings ratio signifies conservative administration as a result of a comparatively excessive proportion of belongings are financed by fairness (Determine 1), which has no contractual proper to curiosity funds, making the corporate extra financially sturdy in a downturn. All different issues being equal, an organization with a low debt to belongings ratio has a excessive loss-absorbing capability (see beneath). A ratio better than 1 signifies that an organization has extra liabilities than belongings and is usually very rigid in an financial downturn and more and more on the mercy of its collectors (i.e., an elevated danger of insolvency).

Determine 1: Comparability of a steadiness sheet with a low debt to belongings ratio (left) and a excessive debt to belongings ratio (proper) (personal work)

Conversely, the upper the debt to belongings ratio, the decrease the loss absorption capability and the upper the theoretical likelihood that there is not going to be sufficient left over to fulfill the claims of suppliers, pensioners, bondholders, shareholders and different stakeholders within the occasion of chapter. This, after all, raises the query of the particular worth of an organization’s belongings within the occasion of chapter – a query that’s troublesome (inconceivable?) to reply ex ante.

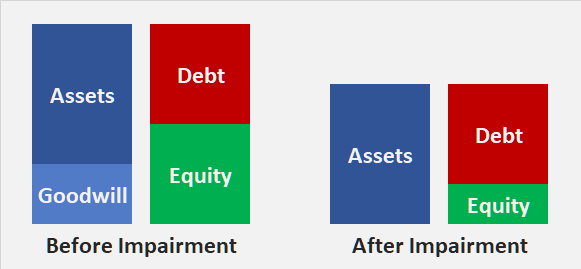

Whereas I acknowledge that the majority traders take a look at an organization on a going concern foundation and due to this fact don’t essentially must know the “true” worth of the belongings, it’s nonetheless essential to observe for a probably inflated asset base. Take, for instance, an organization that grows by acquisitions, assuming goodwill (the premium paid along with the worth of the belongings) within the course of. If an organization in some unspecified time in the future sooner or later determines that the honest worth of the acquired cash-generating unit is lower than its carrying quantity, the goodwill (and presumably different intangible belongings) is impaired. This reduces the belongings and impacts the corporate’s fairness, leading to a rise within the debt to belongings ratio (Determine 2).

Determine 2: Schematic illustration of the lower in fairness when an organization acknowledges a goodwill impairment cost (personal work)

Frequent sense tells us that firms whose belongings include a excessive share of goodwill may have to acknowledge impairment expenses in some unspecified time in the future. Kraft Heinz Co (KHC), for instance, had a debt to belongings ratio of 45% on the finish of 2017. 37% of belongings consisted of goodwill and 50% consisted of different intangible belongings (e.g., emblems). In 2018, KHC incurred impairment expenses of $7.0 billion and $8.9 billion on goodwill and different intangible belongings, respectively. The corporate didn’t incur any further debt in 2018, so impairment expenses had been the first motive for the five hundred foundation level enhance in KHC’s debt to belongings ratio.

All in all, I am not a giant fan of utilizing debt to belongings ratios as a measure of leverage. They don’t take into consideration an organization’s earnings energy and require at the very least a tough thought of the worth of an organization’s belongings. Such ratios are problematic when calculated for steadiness sheets with a excessive share of goodwill or a listing place liable to markdowns (see my article on Goal Company (TGT)). I acknowledge that the ratio offers a sign of how conservatively or aggressively an organization is financed, however there are a number of different ratios that serve the identical function and supply further perception. In closing, I personally don’t pay a lot consideration to debt to belongings ratios.

Debt To Fairness

The debt to fairness ratio is one other leverage ratio that’s equally straightforward to calculate because the debt to belongings ratio, however in its pure kind solely requires knowledge from the correct facet of the steadiness sheet (whole debt divided by whole fairness). As above, a number of definitions exist. An investor could select to deduct money and money equivalents in the event that they symbolize a big share of whole belongings and are usually not wanted for day-to-day operations. After all, it isn’t at all times straightforward to find out the true share of extra money.

The ratio could also be “easier” in that it requires solely inputs from the correct facet of the steadiness sheet, however that makes an investor probably liable to ignoring the asset base. Recall Determine 2 – an investor trying solely on the legal responsibility facet of the steadiness sheet could also be lulled right into a false sense of safety by the 50% fairness funding.

That is particularly related when taking a look at banks’ steadiness sheets. Regulators require banks to carry a specific amount of fairness relative to their so-called risk-weighted belongings (RWA, see this text for a “easy” method primarily based on inside scores – IRB method). Taking a look at a financial institution’s fairness ratio or debt to fairness ratio may be extraordinarily deceptive, because the unlucky instance of Silicon Valley Financial institution (OTCPK:SIVBQ) has taught us (see my clarification and outlook on banks). Different banks’ belongings have additionally come beneath elevated scrutiny, notably these with a considerable amount of fairness prone to being eroded by giant unrealized losses of their funding portfolios. Truist Monetary Company (TFC) and U.S. Bancorp (USB) are two notably notable examples, as that they had unrealized losses of $8.8 billion and $9.6 billion, respectively, of their held-to-maturity portfolios on the finish of the primary quarter of 2023. Whereas the theoretical influence on their respective fairness is definitely vital and probably devastating (Determine 3), I nonetheless think about the 2 shares speculative buys and have just lately added them to my portfolio.

Determine 3: Truist Monetary Company [TFC] vs. U.S. Bancorp [USB]: Comparability of debt to fairness ratios earlier than and after hypothetical realization of the losses of their held-to-maturity portfolios (personal work, primarily based on the businesses’ 2023 first quarter 10-Qs).![Truist Financial Corporation [TFC] vs. U.S. Bancorp [USB]: Comparison of debt to equity ratios before and after hypothetical realization of the losses in their held-to-maturity portfolios](https://static.seekingalpha.com/uploads/2023/6/8/49694823-16862300327339408.png)

Nevertheless, a excessive leverage ratio is just not essentially a sign of issues. Such static ratios don’t take into consideration an organization’s money earnings energy and may due to this fact result in false positives. A superb instance is Philip Morris Worldwide Inc. (PM), which aggressively purchased again shares after its spin-off from Altria Group Inc. (MO) in 2008 and whose debt to fairness ratio due to this fact truly turned unfavourable in 2012 (Determine 4). Although PMI’s debt to fairness and debt to belongings ratios have appeared fairly scary since 2012, I might argue that the corporate can simply handle its unfavourable fairness due to its very secure earnings and money circulate, in addition to its infamous profitability as a significant tobacco firm.

Determine 4: Philip Morris Worldwide Inc. [PM]: Debt to belongings and debt to fairness ratio because the spin-off from Altria Group, Inc. [MO] (personal work, primarily based on the corporate’s 2009 to 2022 10-Ks)![Philip Morris International Inc. [PM]: Debt to assets and debt to equity ratio since the spin-off from Altria Group, Inc. [MO]](https://static.seekingalpha.com/uploads/2023/6/8/49694823-16862302132049923.png)

The buybacks have considerably improved PMI’s earnings per share, however I might not go as far as to conclude that administration purchased again inventory to spice up in any other case poor earnings. There are different firms, akin to Kimberly-Clark Company (KMB), that I’m assured have purchased again inventory to prop up earnings and money circulate per share. As I mentioned in one other article, KMB’s free money circulate has been treading water since at the very least 2010, however has elevated by greater than 22% when share repurchases are taken into consideration.

In abstract, the debt to fairness ratio may be very straightforward to calculate, however its usefulness is proscribed. It offers a fast view of how aggressively an organization is financed. Just like the debt to belongings ratio, this metric ought to solely be used to match firms in a selected business. A excessive debt to fairness ratio signifies that an organization could also be over-reliant on debt, whereas a low ratio means that administration could also be too conservative and never utilizing debt appropriately to develop (as a reminder, fairness is at all times dearer than debt). A rise within the debt to fairness ratio over time as a consequence of:

impairment of goodwill and different intangible belongings, accelerated depreciation and amortization of fastened belongings and different belongings, incurring debt to fund unpromising tasks, or incurring debt to aggressively repurchase shares to spice up earnings per share.

… could point out a deterioration in fundamentals. Nevertheless, a excessive debt to fairness ratio doesn’t essentially sign issues, as the instance of Philip Morris Worldwide Inc. confirmed. As will likely be mentioned beneath, I imagine it is rather essential to think about an organization’s money earnings energy when assessing the manageability of its debt.

Debt To EBITDA

The ratio of debt to earnings earlier than curiosity, taxes, depreciation and amortization (EBITDA) offers a dynamic view of the debt of an organization. Whereas the above ratios are helpful for a fast peer group comparability and for figuring out probably problematic developments, they don’t enable a conclusion to be drawn concerning the sustainability of the debt. Earlier than we take a more in-depth take a look at the ratio, a phrase of warning. EBITDA is also known as a money circulate metric. I will not go into element about why that is problematic, and I believe it suffices to cite the feedback of Warren Buffett and Charlie Munger within the 2000 annual report of Berkshire Hathaway Inc. (BRK.A, BRK.B):

“Traders are sometimes led astray by CEOs and Wall Road analysts who equate depreciation expenses with the amortization expenses we have now simply mentioned. On no account are the 2 the identical: With uncommon exceptions, depreciation is an financial price each bit as actual as wages, supplies, or taxes. Actually that’s true at Berkshire and at just about all the opposite companies we have now studied. Moreover, we don’t assume so-called EBITDA (earnings earlier than curiosity, taxes, depreciation and amortization) is a significant measure of efficiency. Managements that dismiss the significance of depreciation – and emphasize “money circulate” or EBITDA – are apt to make defective selections, and you must maintain that in thoughts as you make your individual funding selections.”

Web page 65, 2000 annual report, Berkshire Hathaway Inc.

The debt to EBITDA ratio sometimes relates all interest-bearing debt to EBITDA. It’s essential to make a significant estimate of EBITDA, and traders must be cautious of one-time expenses or tailwinds. I normally take a look at the three-year common of EBITDA, however after all, that does not assist with firms which are rising aggressively or are in decline. It is a very descriptive metric as a result of it exhibits the variety of years it theoretically takes an organization to pay down its debt. After all, that is the place the issues begin, as a result of I’ve but to come back throughout an organization that doesn’t must make common investments and pay taxes and curiosity.

Suffice it to say, I do not like to make use of the debt to EBITDA ratio due to these critical flaws and solely use it for firms that do not have precise free money circulate, akin to utilities. In a nutshell, the debt to EBITDA ratio assumes an indefinite lifetime of the corporate’s belongings. I acknowledge that the investments of those firms are usually very long-lived, however they finally depreciate, so I stay very cautious about utility debt usually, and particularly within the present excessive rate of interest surroundings.

Take the instance of The Southern Firm (SO), a utility I’ve reported on prior to now. Metrics akin to internet monetary debt to belongings and internet monetary debt to fairness are usually not useful on this context:

Determine 5: The Southern Firm [SO]: Internet monetary debt to belongings and internet monetary debt to fairness ratio since 2017 (personal work, primarily based on the corporate’s 2017 to 2022 10-Ks)![The Southern Company [SO]: Net financial debt to assets and net financial debt to equity ratio since 2017](https://static.seekingalpha.com/uploads/2023/6/8/49694823-1686231258402452.png)

If one takes into consideration (adjusted) EBITDA as a proxy for earnings, issues look completely different. After all, one may argue that the substantial capital expenditures related to the development of Vogtle Models 3 and 4 will end in larger earnings in a while and that the price overruns are one-time in nature, however I might argue that there’s at all times a approach to make debt metrics look good. Nevertheless, even utilizing EBITDA earlier than “particular objects,” it’s clear that Southern’s debt solely is aware of one path. In 2012, internet monetary debt was 3.0 instances adjusted EBITDA, and by 2022 it had elevated to five.6 instances.

Though this all sounds very unfavourable and maybe implies that the debt to EBITDA ratio is a kind of ineffective metric, traders ought to nonetheless control the ratio, as many collectors have formulated debt covenants primarily based on this ratio. Not solely can they immediately influence an organization’s entry to sources of liquidity, however a breach of debt covenants can rapidly result in a dividend minimize or different disagreeable administration selections.

On this regard, diversified producer Leggett & Platt, Inc. (LEG) serves as instance. As a result of cyclical nature of its earnings, administration acted prudently in 2020 and agreed with its collectors to change among the debt covenants. For instance, the debt covenant related to LEG’s revolving credit score facility was modified from gross debt to internet debt in Might 2020 and once more in September 2021, to three.5 instances internet debt to EBITDA from 2.5 instances beforehand (p. 94, 2021 10-Ok), creating extra headroom for short-term liquidity wants. Determine 6 exhibits the evolution of Leggett’s leverage because the first quarter of 2020. Those that have adopted my articles on the corporate know that free money circulate fell off a cliff in 2021, underscoring the usefulness of adjusted EBITDA within the context of debt covenants, as it’s much less delicate to short-term fluctuations than precise free money circulate.

Determine 6: Leggett & Platt, Inc. [LEG]: Internet monetary debt to trailing 12-month adjusted EBITDA since 2020 (personal work, primarily based on the corporate’s quarterly earnings releases)![Leggett & Platt, Inc. [LEG]: Net financial debt to trailing 12-month adjusted EBITDA since 2020](https://static.seekingalpha.com/uploads/2023/6/8/49694823-16862316960432389.png)

Debt To Free Money Circulation

My common readers know that I place nice emphasis on free money circulate. As an income-oriented investor, I want to make sure that the businesses I personal generate sufficient money to fund their operations, develop, and pay a (rising) dividend. I acknowledge {that a} significant estimate of the debt to free money circulate ratio requires a bit of labor. For one, the analyst should be cautious of seemingly non-cash prices (e.g., stock-based compensation and associated share repurchases to offset dilution). It’s also essential to have understanding of working capital actions, particularly for firms with excessive working capital wants and/or these working in cyclical industries. These curious about calculating debt relative to free money circulate themselves ought to learn this text detailing my changes to traditional free money circulate.

Placing (interest-bearing) debt in relation to free money circulate provides the same illustrative quantity to the ratio of debt to EBITDA. One can subtract common bills akin to dividends to shareholders to reach at a extra conservative estimate of an organization’s leverage. The debt to free money circulate ratio is unquestionably my most well-liked leverage metric, together with the curiosity protection ratio (see beneath).

It’s inconceivable to make a suggestion for an acceptable debt to free money circulate ratio. Firms with dependable money flows and low capital expenditures, akin to tobacco firms or IT firms with sturdy subscription fashions akin to Microsoft Company (MSFT), can clearly deal with a lot larger leverage ratios than cyclical industrial firms akin to 3M Firm (MMM). On this context, it’s after all attention-grabbing to notice that Microsoft is extraordinarily conservatively financed (Determine 7) regardless of its extremely dependable money flows, whereas 3M’s leverage is changing into extra of an issue, partly as a consequence of excessive anticipated settlement expenses and declining money flows from operations – which is attributable to rising competitors, its cyclicality, and operational inefficiencies.

Determine 7: Microsoft Company [MSFT]: Gross and internet monetary debt to normalized free money circulate; be aware that Microsoft’s unfavourable internet debt to nFCF ratio signifies that the corporate has a internet money place on its steadiness sheet (personal work, primarily based on the corporate’s fiscal 2016 to fiscal 2022 10-Ks)![Microsoft Corporation [MSFT]: Gross and net financial debt to normalized free cash flow; note that Microsoft's negative net debt to nFCF ratio indicates that the company has a net cash position on its balance sheet](https://static.seekingalpha.com/uploads/2023/6/8/49694823-1686231972653794.png)

In precept, I think about a leverage ratio of as much as 4 instances internet debt to free money circulate to be unproblematic, even for slightly cyclical firms. After all, a rise on this ratio over time must be appropriately questioned, because it may point out earnings issues or different challenges. It’s also essential to think about working capital. The post-pandemic interval confirmed us how rapidly money circulate can evaporate when, for instance, provides get caught in transit or components wanted for completion are unavailable.

Lastly, if an organization’s administration is pretty conservative and maintains a low (and even unfavourable) internet debt to free money circulate ratio, I take that into consideration in my valuation. I’m prepared to pay a premium for firms with dependable free money circulate and low debt. In addition to Microsoft, names like The Procter & Gamble Firm (PG) come to thoughts. Beneath strain from activist investor Nelson Peltz, the portfolio has been streamlined, debt compensation has been accelerated by divestitures, and cost-cutting measures have helped to considerably enhance profitability. Consequently, PG’s internet debt is now about 1.4 to 1.8 instances the normalized free money circulate. And even after paying dividends, the corporate would solely want three to 4 years to repay all its interest-bearing monetary liabilities.

Curiosity Protection Ratio

That is my second go-to metric when assessing an organization’s leverage. In response to many textbooks, the curiosity protection ratio is obtained by dividing an organization’s internet working revenue after taxes (NOPAT) by the online curiosity expense incurred. Once more, it can be crucial that the info be significant (e.g., use two- or three-year averages). In its basis, the ratio is simple to calculate and really descriptive. The upper it’s, the higher, as the corporate solely has to spend a relatively small share of its working revenue on curiosity funds.

As at all times, the satan is within the particulars. For instance, it may be harmful to take internet curiosity expense at face worth. Whereas an organization with a considerable money place could offset a few of its curiosity expense with curiosity revenue from short-term investments, this revenue is delicate to fluctuations in rates of interest, whereas the weighted-average rate of interest on the corporate’s whole debt adjusts comparatively slowly. On this context, I discover it extraordinarily useful to think about the debt maturity profile, additionally calculating the weighted-average rate of interest on debt maturing over a given interval. In my latest article on The Dwelling Depot, Inc. and Lowe’s Firms, Inc. (LOW), I mentioned a number of essential implications of rates of interest, noting, for instance, that HD is more likely to face larger curiosity expense because of the comparatively low rate of interest on its debt maturing within the subsequent few years:

Determine 8: The Dwelling Depot, Inc. [HD]: Lengthy-term debt maturities as of year-end 2022 (personal work, primarily based on the corporate’s 2022 10-Ok)![The Home Depot, Inc. [HD]: Long-term debt maturities as of year-end 2022](https://static.seekingalpha.com/uploads/2023/6/8/49694823-16862323874477353.png)

Within the context of rates of interest, it is rather essential to search for potential debt with adjustable charges. Organon & Co. (OGN), the ladies’s health-focused spin-off from Merck & Co. (MRK) that I just lately reported on, is an efficient instance. On the finish of the second quarter of 2022, administration anticipated curiosity expense to be $400 million, and though the corporate voluntarily repaid $250 million of its long-term debt within the first quarter of 2023, curiosity expense in 2023 is predicted to be $515 million.

Since earnings are comparatively straightforward to handle, I desire to calculate curiosity protection utilizing normalized free money circulate earlier than curiosity. I notice that including internet curiosity expense to free money circulate is just not totally correct, because it doesn’t take into consideration the tax defend impact of curiosity expense, however it’s a ample proxy for my part. An curiosity protection ratio of six instances free money circulate earlier than curiosity is completely acceptable, and I’m prepared to pay a premium for a corporation whose curiosity protection ratio is properly above the peer group common.

Lastly, I believe it may be worthwhile to do situation analyses. The yr 2022 has taught us that we shouldn’t be fooled by the obvious “new regular” of a zero rate of interest surroundings. Traders who made certain their firms may face up to a excessive rate of interest surroundings earlier than rates of interest rose may gracefully keep away from firms with a problematic capital construction. On the similar time, calculating the curiosity protection ratio beneath stress situations may assist in the context of a possible ranking downgrade, which is normally related to a rise within the firm’s price of capital. On this article, I’ve defined a easy method to performing such calculations that may be simply carried out in Excel or the same spreadsheet program.

A Few Last Phrases Of Warning

The curiosity protection ratio and the debt to free money circulate ratio are the 2 ratios I exploit most frequently when evaluating an organization’s debt. They require a little bit work, however they supply a really clear and easy-to-understand view of the state of affairs. Debt due diligence would not finish there, nevertheless, and I would like to finish the article with two remaining phrases of warning.

Working leases have traditionally not been acknowledged on the steadiness sheet. Nevertheless, leases may be vital, particularly for retailers, and the related contractual funds can change into problematic in an financial downturn or when company-specific points come up. Starting in 2019, working leases should be acknowledged on the steadiness sheet (ASC 842 and IFRS 16), so it has change into harder to miss this merchandise. There are a number of methods to account for working leases. I personally account for them by calculating a modified model of the debt to free money circulate ratio. On this context, it is very important solely examine members of a consultant peer group.

Second, pension-related obligations may be thought of kind of delicate to rates of interest. Specifically, “outdated financial system” firms with slightly standard compensation fashions could have vital unfunded pension-related obligations on their steadiness sheets. I mentioned Lockheed Martin Company’s (LMT) pension obligations in one other article, noting positively that the corporate has transferred a good portion of the obligations to retirement providers firms akin to Athene Holding Ltd. (ATH.PB, ATH.PC, ATH.PD), thereby taking strain off its personal steadiness sheet.

Conclusion

The article supplied an summary of a number of kind of frequent ratios that can be utilized to evaluate an organization’s leverage.

Ratios akin to debt to belongings (debt to capital) or debt to fairness, with all their nuances, are straightforward to find out and may present an preliminary indication of an organization’s vulnerability in an financial downturn or level to inefficiencies as a consequence of inappropriate use of debt. Nevertheless, as a result of they’re static ratios, they supply solely a really restricted image, so it is very important evaluation the evolution of those ratios over a number of years. The debt to fairness ratio may be very straightforward to acquire, because the asset facet of the steadiness sheet may be ignored. Nevertheless, this places the analyst prone to overlooking belongings which are prone to write-downs, which immediately influence fairness and, due to this fact, loss absorption capability. The asset facet of the steadiness sheet must be critically examined, and that is notably true for banks or firms with a excessive proportion of goodwill and different intangible belongings.

Nevertheless, as the instance of Philip Morris Worldwide and The Southern Firm has proven, these ratios can produce deceptive outcomes. Within the first case, traders could also be unjustifiably alarmed, whereas within the second case, a possible deterioration within the firm’s fundamentals could also be ignored.

Dynamic metrics akin to debt to EBITDA or debt to free money circulate present higher perception into the state of affairs. Nevertheless, since EBITDA is just not a real earnings metric (all firms must pay taxes, make common investments, and pay kind of curiosity), traders must be cautious when evaluating debt to EBITDA. However, this ratio is essential within the context of debt covenants and will due to this fact be reviewed frequently, particularly for cyclical firms and/or firms prone to short-term liquidity points. Debt covenants additionally typically immediately influence an organization’s potential to pay dividends.

My favourite metrics are the debt to free money circulate ratio and the curiosity protection ratio. Utilizing precise money earnings as an alternative of reported earnings elegantly avoids a number of pitfalls and may present a reasonably clear view of an organization’s debt servicing potential. Consideration of the debt maturity profile permits identification of a possible near-term enhance in curiosity expense, and correct evaluation of free money circulate volatility (notably when it comes to working capital actions) permits an knowledgeable conclusion about an organization’s debt servicing potential in any financial local weather.

Nevertheless, debt due diligence doesn’t finish with an examination of an organization’s interest-bearing debt. It is very important additionally think about kind of sector-specific obligations akin to working leases and pension obligations. Evaluation ought to at all times be restricted to a particular peer group. It is not sensible to match the leverage of a retailer with excessive working leases with that of an organization with low belongings akin to a tobacco firm or an asset supervisor. Equally, it is not sensible to lament the excessive leverage of financial institution steadiness sheets and examine them to these of non-financial firms.

Lastly, it is very important at all times examine debt and curiosity expense to steadiness sheet or earnings ratios. It is not sensible to keep away from an organization due to its seemingly excessive debt in absolute phrases. At instances, information retailers take pleasure in sensational reviews that an organization has racked up tens of billions of {dollars} in debt, with out placing the quantity into correct perspective.

Additionally, traders have to be cautious when evaluating debt metrics from completely different knowledge suppliers. There are a selection of definitions, and it is very important know what truly went into the calculation. Generally knowledge suppliers’ calculations are opaque, or the required data is troublesome to acquire.

As at all times, please think about this text solely as a primary step in your individual due diligence. Thanks for taking the time to learn my newest article. Whether or not you agree or disagree with my conclusions, I at all times welcome your opinion and suggestions within the feedback beneath. And if there’s something I ought to enhance or develop on in future articles, drop me a line as properly.

{kind=link}