Kevin Brine/iStock Editorial by way of Getty Photographs

Introduction

Over the previous few years I’ve written quite a few articles on Plaza Retail REIT (OTC:PAZRF) (TSX:PLZ.UN:CA), a Canadian REIT specializing in industrial actual property within the Jap a part of the nation. I picked up the debentures on the peak of the COVID disaster at a yield to maturity of in extra of 10% (which was fairly good given the low rates of interest on the markets throughout these days). The debenture was absolutely repaid earlier this 12 months so I wished to take a look to see if I ought to maybe dip my toe into the frequent models of Plaza Retail REIT to retain publicity to the corporate.

The FFO and AFFO had been fairly robust within the first quarter

I received’t go into an excessive amount of element discussing the property and the principle tenants of Plaza Retail REIT and I’d prefer to refer you to this older article from February which reviewed all these components. I’d fairly deal with the REIT’s current earnings report and the way it plans to take care of the growing rates of interest on the monetary markets which is able to finally hit its financing construction as properly.

The REIT remained worthwhile and though profitability isn’t metric for any REIT to be judged on, I prefer to take a second to take a look on the revenue assertion because it permits an investor to establish sudden adjustments in, as an example, the G&A bills and the curiosity bills.

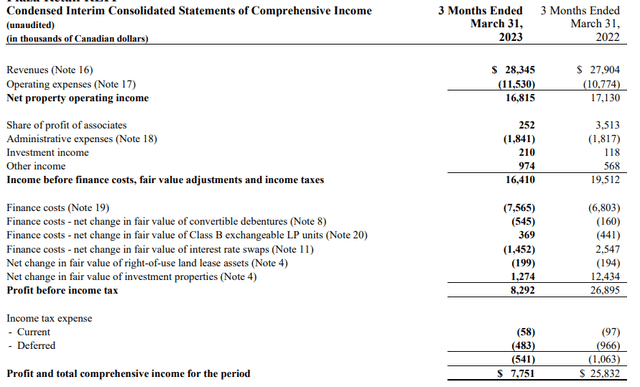

Plaza Retail Investor Relations

As you possibly can see above, the online property revenue decreased in comparison with Q1 2022. Regardless of a 1.5% income enhance, the sudden 7% enhance within the working bills threw a wrench on the monetary efficiency and the online property revenue decreased by roughly 2% to C$16.8M. Wanting on the breakdown of these working bills, the rise seems to be primarily associated to the non-recoverable bills together with a C$0.14M unhealthy debt expense. Moreover, the REIT needed to grant a tenant a C$235,000 allowance for the delayed supply of premises. So there look like some non-recurring gadgets there and adjusted for even simply these two components, the NOI would have proven a small enhance. And on a same-asset NOI, there would have been a 0.8% enhance.

Plaza Retail Investor Relations

The revenue assertion additionally exhibits a ten% enhance within the curiosity bills, which elevated from C$6.8M to C$7.6M. I count on the curiosity bills to proceed to extend as current fastened fee mortgages will roll off and should be refinanced.

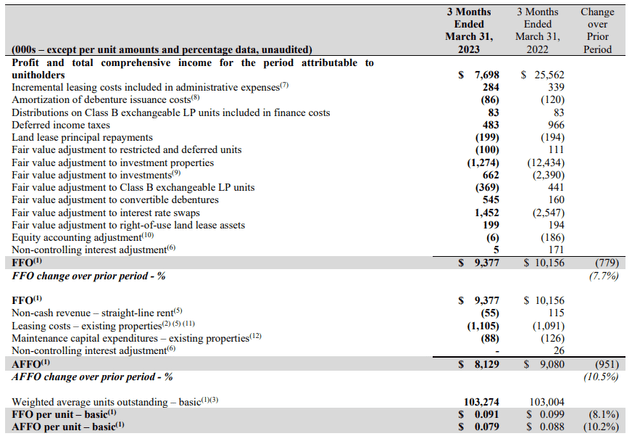

The FFO and AFFO clearly are higher metrics to evaluate a REIT on. As you possibly can see under, Plaza Retail REIT generated a complete FFO of C$9.4M and a internet AFFO of C$8.1M. Each are down in comparison with the primary quarter of final 12 months and this is also defined by the impression of the 2 non-recurring gadgets on the NOI in addition to the upper curiosity bills.

Plaza Retail Investor Relations

With an AFFO of just below C$0.08 per share, the inventory is presently buying and selling at about 12 occasions the annualized AFFO.

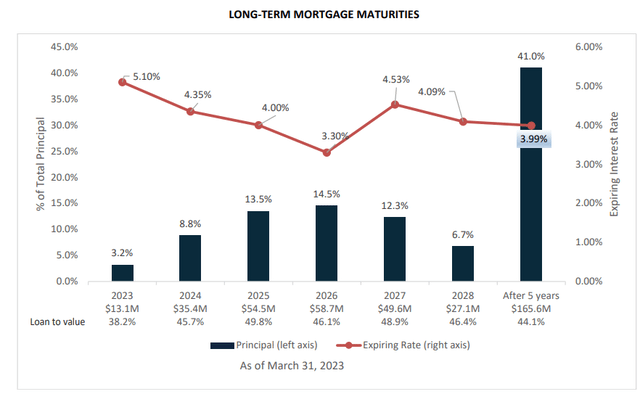

What about debt maturities and the anticipated curiosity price enhance?

Whereas that a number of sounds engaging, let’s not neglect the worst is but to return in relation to curiosity bills. The debt degree has just lately decreased due to a purchased deal and the entire debt to gross asset worth decreased to 52%. The LTV ratio (outlined as internet debt versus actual property property) is lower than 50% and even 47.5% should you’d embody the opposite investments on the stability sheet.

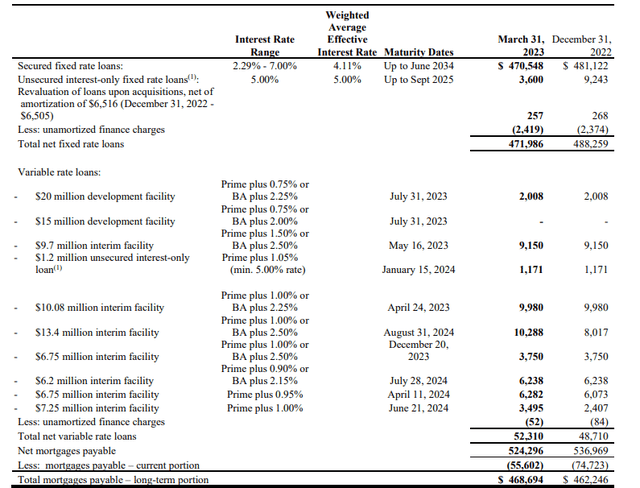

A very powerful portion of the debt consists of mortgage financings and of the C$525M in complete quantity of mortgages, about 90% has a set fee.

Plaza Retail Investor Relations

The following few years can be attention-grabbing however thankfully Plaza’s maturity dates are very properly unfold out in time. In 2024 solely C$35M of debt should be refinanced adopted by simply C$54.5M in 2025. The common weighted rate of interest for these maturities is roughly 4.13%. Assuming the common price of debt will increase to six.25% for a mortgage mortgage, the REIT will see its curiosity bills enhance by simply over C$1.8M per 12 months. That’s C$0.45M per quarter and roughly 5% of the present AFFO consequence.

Plaza Retail Investor Relations

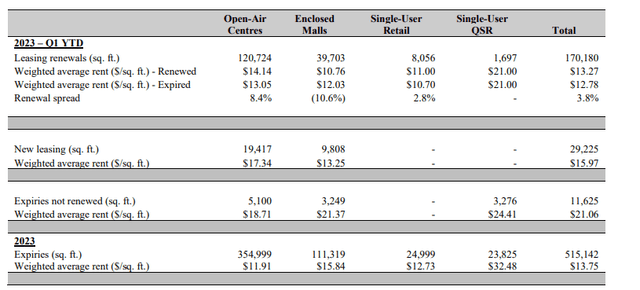

This doesn’t imply we’ll see the AFFO lower by 5% within the subsequent few years because the leasing efforts are going properly. The full renewal unfold in Q1 was a bit weaker than I had anticipated (at 3.8%) and the picture under exhibits this was attributable to a destructive renewal unfold within the enclosed malls division. In accordance with Plaza this was primarily associated to 1 tenant which dragged all the efficiency down and excluding that one renewal the entire renewal unfold would have been a optimistic 7.3%.

Plaza Retail Investor Relations

Apparently, the brand new lease agreements are at a considerably greater fee. As you possibly can see above, the common hire of the open air centres was C$14.14 per sq. foot for renewed contracts, however new leasing agreements had been signed at a considerably greater fee of C$17.34 per sq. foot. And looking out on the enclosed malls there additionally was a 25% uptick in comparison with the renewal fee. After all these are simply smaller agreements so for now I’ll take into account them to be ‘anecdotal’, however the brand new lease spreads are very encouraging. So Plaza undoubtedly has the potential to mitigate the impression of the upper curiosity bills.

Funding thesis

Plaza Retail Charge doesn’t look like overly costly at 12 occasions the anticipated AFFO for this 12 months, however I believe it’s protected to imagine there received’t be a lot development over the subsequent few years as current debt should be refinanced. The full refinancing requirement for 2024 and 2025 is just below C$150M and primarily consists of mortgages in addition to some financial institution debt and the fee of principal on different mortgages (that aren’t maturing).

Retaining the AFFO steady at round C$0.32-0.34 per share per 12 months would already be a powerful achievement for Plaza. It could additionally imply the present distribution of C$0.28 per 12 months remains to be absolutely lined, whereas the present share worth represents a reduction of roughly 20% to the NAV utilizing a 6.75% capitalization fee can also be fairly engaging. A rise of the capitalization fee to 7.5% (excluding the impression of future hire hikes) would end in an NAV of round C$4/share.

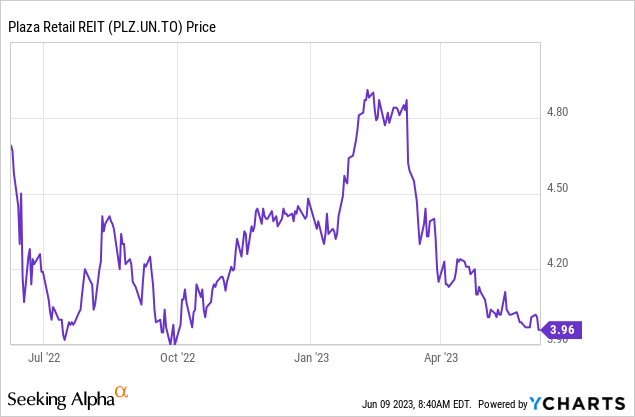

I additionally recognize administration’s determination to boost cash in March when the inventory worth was greater. The REIT accomplished a C$40M purchased deal providing in March at C$4.68 per share and used the proceeds to repay the convertible debentures. The impression of the dilution on the AFFO needs to be fairly impartial contemplating the capital increase was used to cut back the gross debt excellent.

I presently haven’t any place in Plaza however I’m nonetheless conserving observe of the story.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}