DKosig

I’m altering the format of those weekly updates. Slightly than publishing one lengthy weekly word, the weekend word will cowl simply the market and financial information of the week. The overall commentary portion will probably be revealed one other day throughout the week. We can even be publishing some new analysis notes throughout the week.

Surroundings

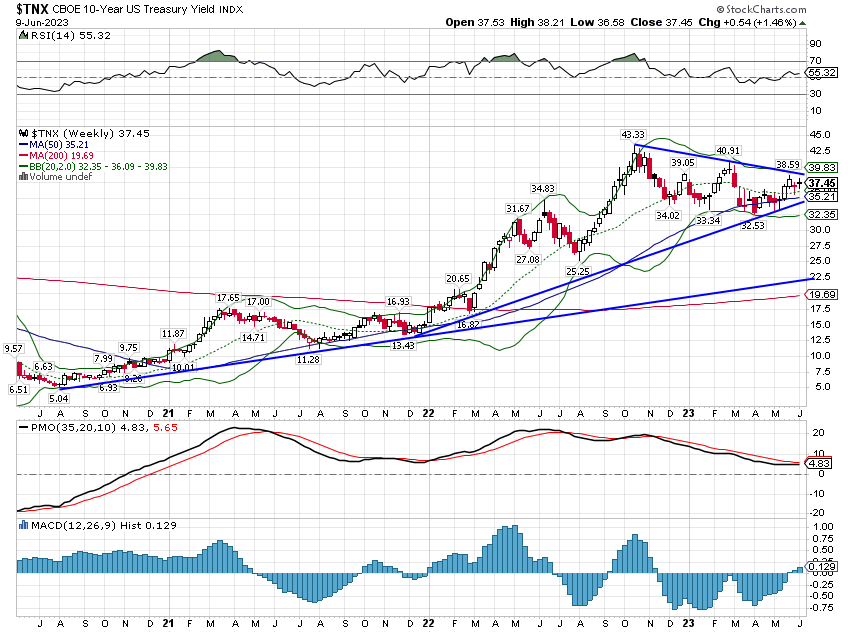

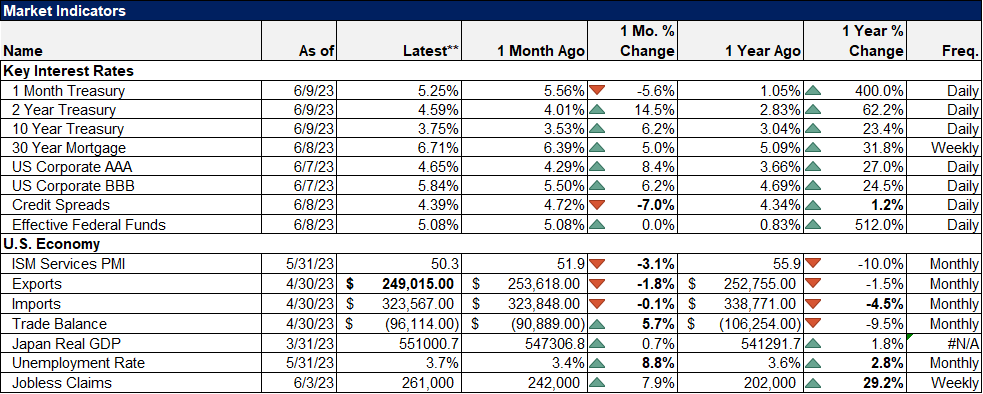

The ten-year Treasury yield was modestly larger final week however the development – or lack thereof – hasn’t modified. The ten-year fee remains to be in the identical short-term downtrend/impartial sample it has been in since peaking in October. We could get some readability on the long run development this week with the most recent CPI studying and the June FOMC assembly.

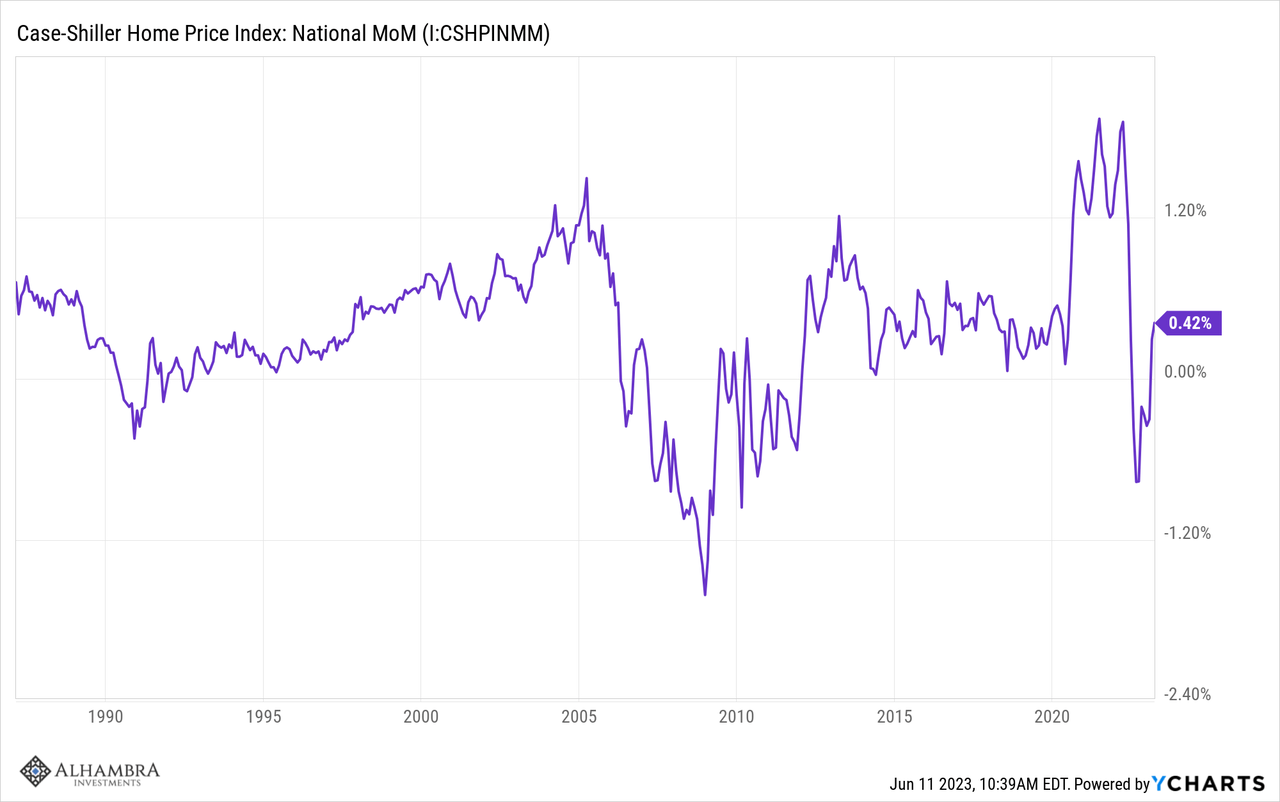

The two-year Treasury yield was additionally larger and, just like the 10-year, continues to meander sideways. Shorter-term invoice charges (1- and 3-month) had been a tad decrease on the week however no developments have modified. I don’t know which manner charges will go from right here however there was a widespread expectation that inflation would average this yr as decrease home costs feed by way of to decrease rents within the CPI. Which will show true within the very quick time period however home costs haven’t actually come down that a lot so I’m skeptical it might be the beginning of a development, even when the discharge subsequent week exhibits a slowdown in inflation. The Case-Shiller nationwide house value index peaked in June of final yr and the next value drop took costs all the best way again to the place they had been in…March of final yr. For those who’re trying to actual property for a moderation in core CPI, you is perhaps trying within the mistaken place.

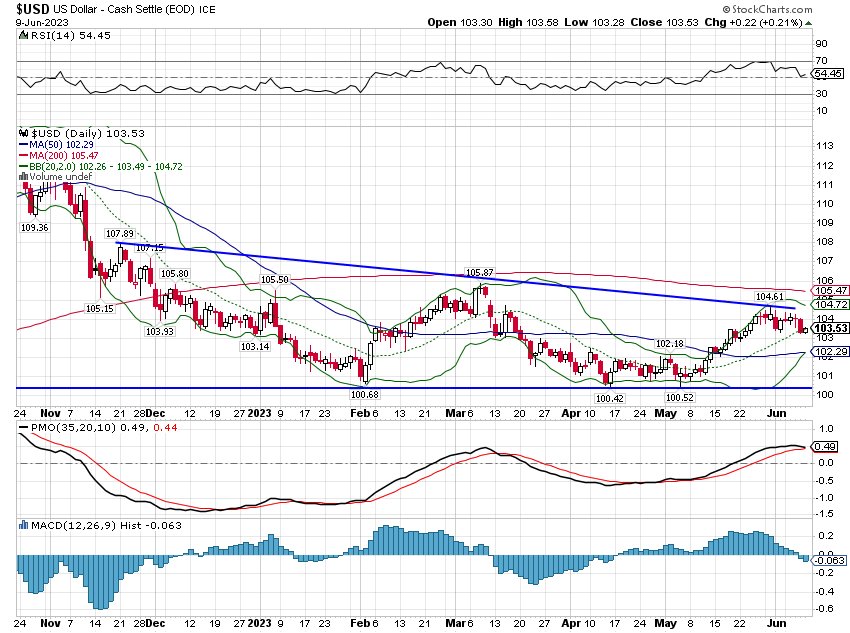

The greenback was down barely on the week however its development hasn’t modified both. The buck additionally peaked final October nevertheless it has fallen greater than charges. For the yr the greenback is basically unchanged, up a mere 0.3%. Like rates of interest, the greenback’s development is sideways.

How that adjustments will probably be decided by quite a lot of components nevertheless it actually comes right down to relative development between the US and the remainder of the world. Within the US, development expectations have been remarkably steady regardless of all of the discuss of recession. Nominal and actual rates of interest have barely budged this yr and so the distinction between the 2 hasn’t both. The ten-year TIPS yield is down 5 foundation factors this yr and the 10-year nominal yield is down 15 so 10-year breakevens are down simply 10 foundation factors.

In the meantime, European development has been weak with lots of people claiming the continent is in recession. It’s true that GDP development in Germany was unfavourable for 2 consecutive quarters however with the DAX nonetheless close to its excessive, it doesn’t appear to be putting worry within the hearts of traders. General, I’d say that European development has actually downshifted however so has the US and the relative change is small.

Japan’s Q1 GDP was revised up considerably final week and the notion of Japan is altering quickly. The acquire in Q1 GDP was as a result of funding (though partially in stock) whereas home consumption stays weak. That isn’t stunning with actual incomes nonetheless falling as a result of excessive inflation (or what passes for top in Japan). However Japan’s financial future is extra about what occurs outdoors Japan than inside. I’ve stated for fairly a very long time that Japan is well-positioned to learn from any pullback from China and that hasn’t modified. However that additionally signifies that a worldwide slowdown can have a much bigger affect on Japan than an economic system – just like the US – much less depending on exports for development.

With no course on charges or the greenback, huge bets on asset allocation would appear unwise. The property that carry out nicely when the greenback is rising are fairly completely different than those that work with a weak greenback. We now have a bias to a weaker greenback in our portfolios for now however that was initiated when the greenback reached an excessive peak final yr and the overwhelming consensus was bullish on the buck. There aren’t actually any extremes in positioning proper now and sentiment is fairly impartial. We’ll look forward to a brand new development to emerge. Foreign money developments are typically persistent so be affected person.

Markets

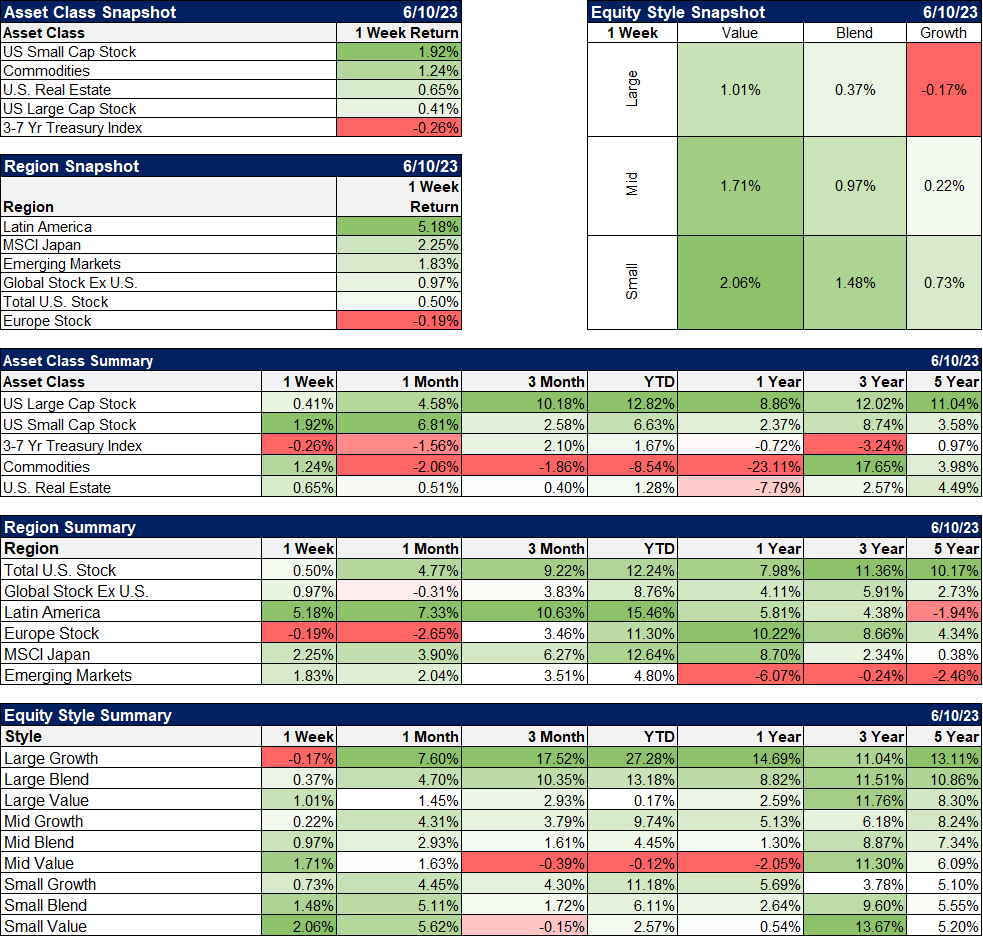

The remainder of the market began to play catch-up to the large-cap development section final week. Small-caps, REITs, and commodities had been all larger whereas large-cap development bought off modestly. However the information of the week was that the S&P 500 rose (briefly) 20% above its October low. That transfer was hailed by some as the beginning of a brand new bull market and sentiment is actually tilted bullish. Nicely, perhaps a bit of greater than tilted. Right here’s the quilt of Barron’s this week:

Barron’s covers are a mirrored image of the temper of the market and there’s no doubt the bulls have been successful the battle not too long ago with regards to giant development shares. However giant development shares aren’t the market and the way issues go from right here will rely upon a whole lot of issues we will’t predict, just like the arrival of the long-anticipated recession. If that is actually the beginning of a brand new bull market, we might count on to see the rally broaden out and begin to embody extra shares. We noticed a few of that final week with small-cap shares however the notion remains to be that the advance may be very slender.

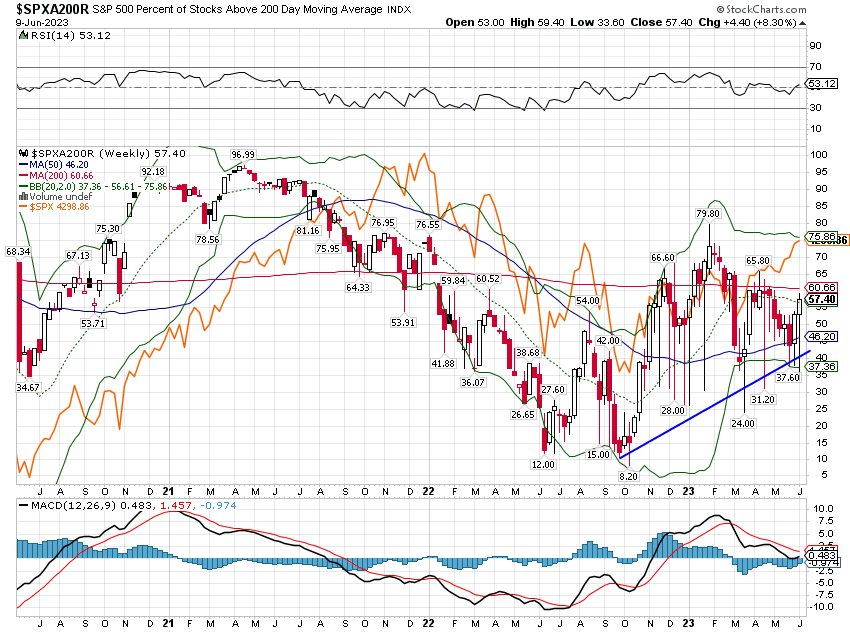

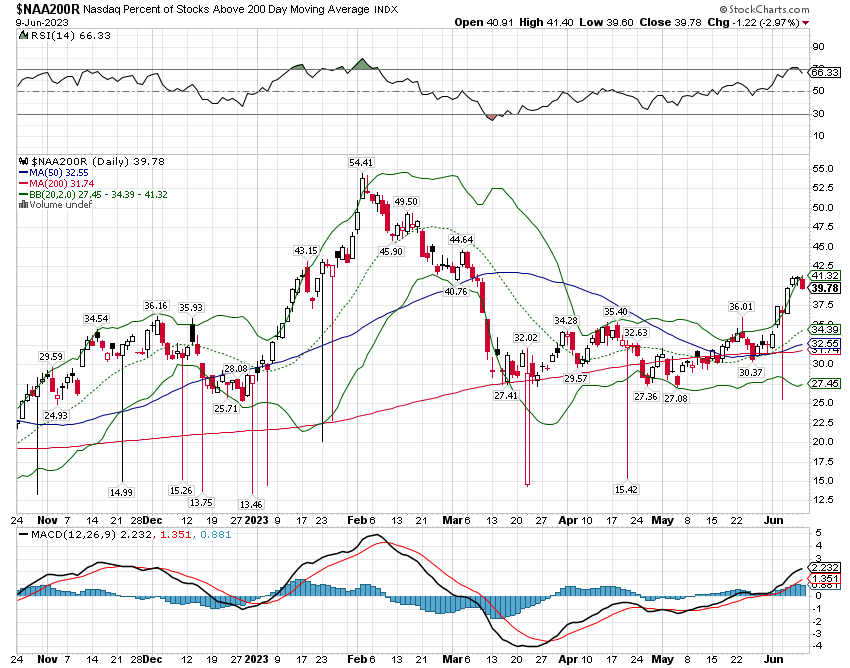

Possibly, however I believe what issues is the development. Proper now 57% of the shares within the S&P 500 are above their 200-day shifting common (a standard dividing line between uptrend and downtrend) so the vast majority of shares within the index are in an uptrend. The long-term common is 62% which is sensible because the market rises over time. However, extra importantly, the development is, for now, up.

What actually issues are the extremes. This metric hit 97% in early 2021 and eight% on the low in October and each had been close to turning factors. There’s an previous saying on Wall Avenue that tops are a course of and bottoms are an occasion and you’ll see that right here. The S&P 500 (orange line) continued larger after the height however the backside for shares was coincident with the underside for this indicator. The purpose is that we aren’t anyplace close to both excessive proper now and it’s in a rising development. The NASDAQ measure of this indicator is even decrease at round 39%. So, sure, the advance is fairly slender. However that isn’t stunning with the underside of the market simply 6 months in the past. And extra importantly, the development is up:

We take a look at sentiment in a whole lot of methods and there’s no doubt that it’s fairly bullish proper now so a correction of some sort wouldn’t be stunning within the least. The Barron’s cowl may mark some type of short-term prime, nevertheless it doesn’t must be one thing excessive; the greenback fell after Barron’s ran a bullish cowl final October, nevertheless it didn’t crash.

May a correction be confined to large-cap development? Nicely, I suppose something is feasible however that isn’t the way it often works. Different elements of the market may and doubtless will outperform large-cap development in a correction however they may nonetheless fall too. However a return to the intense low seen in October this quickly appears unlikely based mostly on historical past.

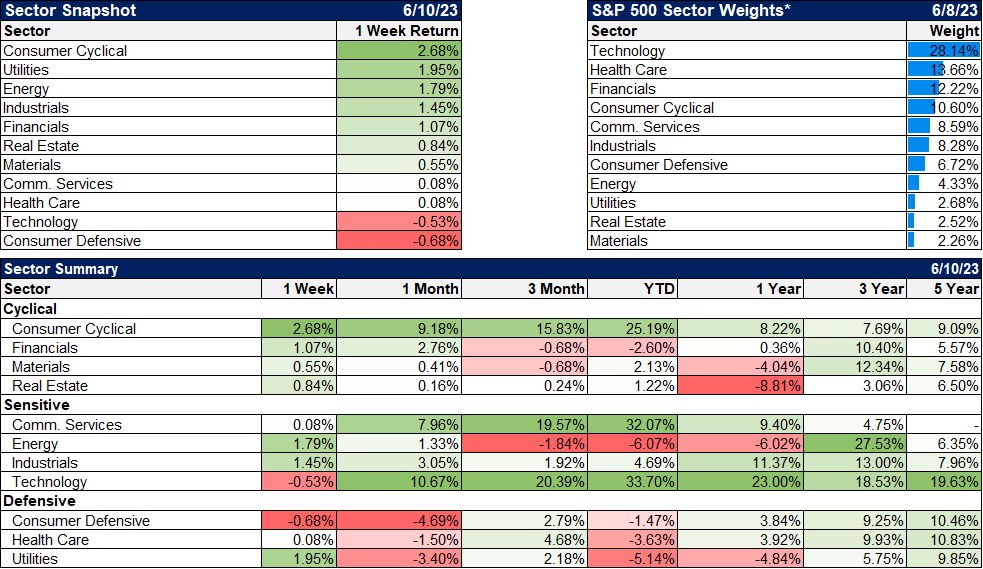

Cyclicals led the market final week however a whole lot of that was Tesla (TSLA) which makes up almost 18% of the buyer discretionary sector ETF and rose 14% final week. The opposite automakers had been up strongly too however once more, that was extra about Tesla as Ford (F) and GM (GM) each signed offers for his or her automobiles to make use of Tesla’s charging community. There have been another winners within the sector however total it was a fairly blended image.

However, the rally was extra broad-based than not too long ago with 9 of 11 sectors larger for the week. YTD beneficial properties are nonetheless concentrated in know-how, communications (which is generally tech too), and cyclicals (shopper discretionary). If this can be a new bull market we might count on to see the rally proceed to broaden out to incorporate extra sectors.

Financial/Market Indicators

There wasn’t a whole lot of financial knowledge final week so there wasn’t a lot change in short-term charges markets. The market is presently pricing a 70% likelihood of a pause – or skip or no matter you need to name it – at this week’s FOMC assembly and a 38% probability that charges are unchanged by the December assembly.

The ISM providers index was weak at 50.3 though the S&P providers PMI moved in the wrong way to 54.9. I’m nonetheless undecided whether or not to belief the S&P model of those PMI surveys. It’s a broader survey so theoretically it ought to be higher nevertheless it doesn’t have the historical past of the ISM model (though frankly, neither has a really lengthy historical past). I’ll proceed to put the next weight on the ISM model till we get some proof the S&P model is dependable.

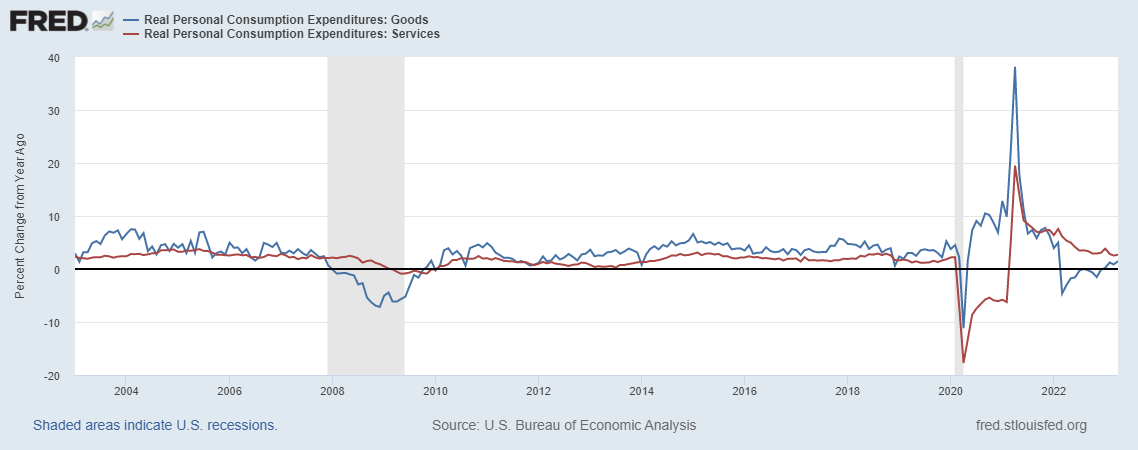

We’ve been writing concerning the distinction between items and providers for over a yr and up to now it has performed out just about as we anticipated. The products aspect of the economic system has slowed (though a lot of that was as a result of stock from provide chain points) whereas the providers aspect continues to recuperate from the COVID shutdowns. We could also be at a degree now the place these are beginning to reverse once more. Inventories haven’t risen in months and if gross sales don’t sluggish quickly, manufacturing should ramp up. Don’t be shocked if the ISM manufacturing survey begins turning up from right here.

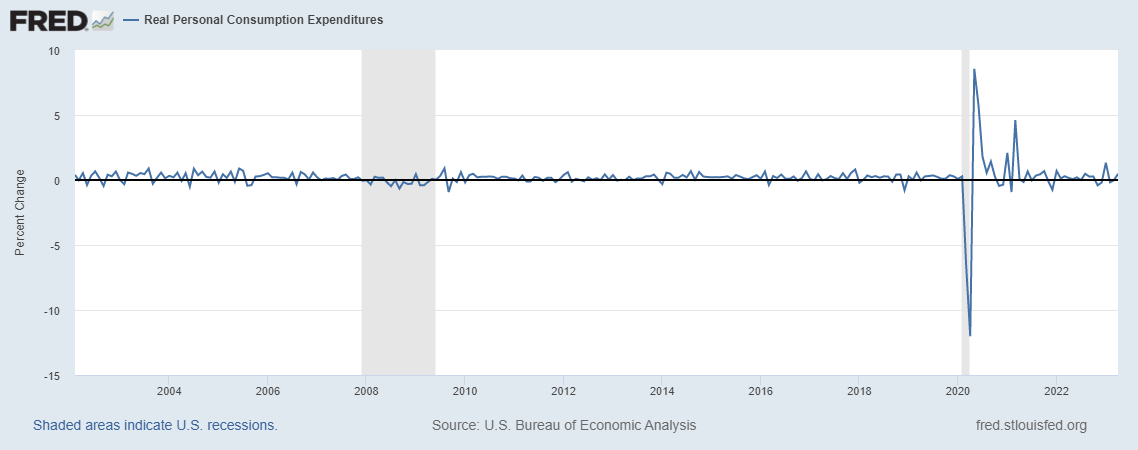

COVID was an earthquake for the economic system so perhaps it isn’t a coincidence that a whole lot of the financial knowledge charts appear to be seismographs.

Even now, 3 years after the onset of COVID, we nonetheless see larger volatility within the month-to-month knowledge on actual private consumption than previous to COVID. Items consumption year-over-year is now again in constructive territory and trending larger whereas providers is constructive however trending decrease. The 2 have a tendency to maneuver collectively though items consumption is extra risky.

Sooner or later they need to sync up once more and begin shifting collectively however when is anybody’s guess. Within the meantime, count on extra aftershocks.

Unique Submit

Editor’s Observe: The abstract bullets for this text had been chosen by Searching for Alpha editors.

{kind=link}