Marco Bello

Funding Thesis

The ARK Fintech Innovation ETF (NYSEARCA:ARKF) has outpaced the SPDR S&P 500 ETF (SPY) by 29.45% in 2023 and by 10.77% since I prompt merchants take a short-term place within the dangerous fund by means of the Q1 earnings season. Primarily based on my elementary evaluation and interpretation of present market sentiment, there may be nonetheless extra potential upside forward. Nonetheless, shareholders are pushing their luck. I like to recommend taking income earlier than the inevitable happens: markets get jittery and goal the riskiest, speculative belongings, that are lots of ARKF’s prime holdings.

ARKF Overview: When To Purchase And Promote

ARKF usually selects 35-55 corporations concerned in transaction innovation, blockchain expertise, danger transformation, frictionless funding platforms, customer-facing platforms, and new intermediaries. ARKF is actively managed by Cathie Wooden and her group at ARK Funding Administration and has a 0.75% expense ratio. Up 43% YTD, ARKF manages $914 million in belongings.

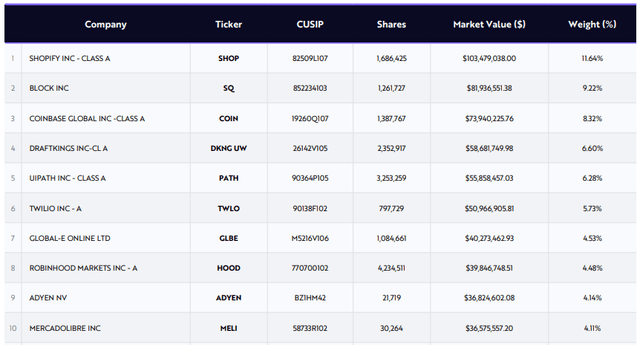

Shopify (SHOP), Block (SQ), and Coinbase International (COIN) are the fund’s prime holdings, totaling 29%. I’ve listed the highest ten beneath; the complete itemizing is accessible for obtain on ARKF’s fund web page. There was little exercise since my final overview, with weighting modifications of lower than 1% per safety.

ARK Make investments

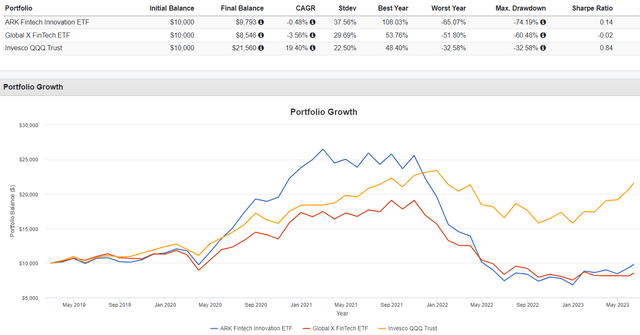

The International X FinTech Thematic ETF (FINX) is considered one of ARKF’s rivals. I beforehand used the Invesco QQQ ETF (QQQ) for instance for these wanting a safer and cheaper development fund. Right here is how the three have carried out since ARKF launched in February 2019.

Searching for Alpha

ARKF outperformed FINX by 3.08% per yr, nevertheless it’s nonetheless but to interrupt even. In the meantime, QQQ delivered an annualized 19.40% and was far more steady, resulting in a powerful 0.84 Sharpe Ratio.

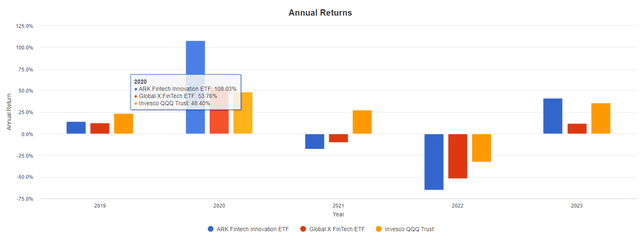

When buyers purchase ARKF, they’re searching for a house run just like the 108% achieve in 2020. The trick is to be conscious of what usually occurs subsequent to speculative, unprofitable baskets of shares: positive factors are rapidly worn out, usually in only a yr or two. That is what occurred with ARKF, because it misplaced 17.82% and 65.07% in 2021-2022.

Portfolio Visualizer

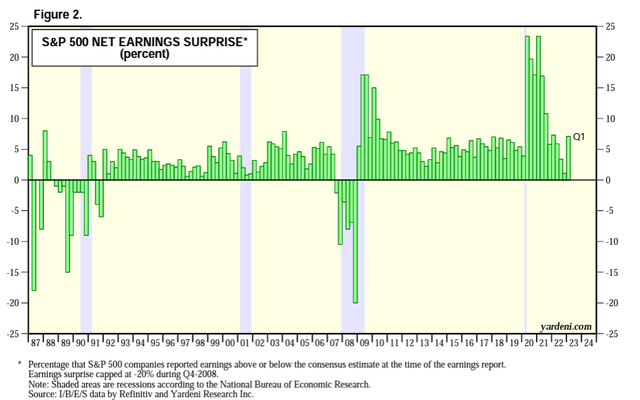

Notice that 2020 circumstances have been uncommon and weren’t all associated to COVID-19. The secret is analyzing and understanding market sentiment, and a technique is to review earnings shock developments. A benchmark is the mixture S&P 500 earnings surprises tracked quarterly by Yardeni Analysis. Discover how earnings surprises have been near or above 20% from Q2 2020 to Q2 2021, one thing we final got here near in 2009 when QQQ gained 55%.

Yardeni Analysis

Which means one yr of overwhelmingly constructive headlines encouraging buyers to purchase into the hype. Low-profitable shares have often carried out effectively for many years, however solely not too long ago have been they packaged properly into thematic ETFs. Think about the next statistics from the Ken French Knowledge Library on equal-weighted portfolios fashioned on working profitability:

1. The underside 30% portfolio (lowest working profitability) outperformed the highest 30% portfolio (highest working profitability) by 37.56% in 1999 on the peak of the dot-com bubble. What adopted in 2000 was a 23.35% underperformance, successfully undoing the prior yr’s positive factors.

2. The underside 30% portfolio outperformed the highest 30% portfolio by 53.34% in 2003, gaining 103.56%. What adopted have been 5 consecutive years of underperformance by means of to 2008. Buyers holding the complete interval from 2003-2008 would earn 26.91% in comparison with 41.69% for the highest 30%.

3. The underside 30% portfolio outperformed the highest 30% portfolio by 9.44% in 2009, gaining 77.86% as markets recovered from the Nice Monetary Disaster. There was additionally a modest 4.22% outperformance in 2010, nevertheless it missed by 7.87% in 2011. The underside 30% portfolio additionally lagged within the high-single-digits in 2016 and 2018. Buyers holding from 2009-2019 would nonetheless do effectively, gaining 324%. Nonetheless, the highest 30% portfolio gained 410%.

4. The underside 30% portfolio beat the highest 30% portfolio by 35.06% in 2020. Nonetheless, these positive factors rapidly reversed in 2021-2022 by 25.52% and 20.97% in 2021-2022, similar to with ARKF. These translate to annualized positive factors of two.11% for the underside 30% portfolio vs. 10.78% for the highest 30% portfolio.

5. Within the 25 years between 1999-2023, the underside 30% averaged a 13.30% achieve in comparison with 13.53% for the highest 30%. This may occasionally lead you to imagine that the working profitability metric has no worth. Nonetheless, compounded returns for the 2 portfolios have been 614% and 1,305%. In different phrases, the high-profitability portfolio is the higher selection as quickly as you lengthen your holding interval past one yr. The underside 30% portfolio is for merchants, not buyers, and the identical is true for ARKF. As an example, let’s take a look at the profitability of its parts subsequent.

ARKF Evaluation

Profitability

ARKF has a 4.48/10 Profitability Rating, which I derived utilizing particular person Searching for Alpha Profitability Grades, normalizing them on a ten-point scale, after which weighting them accordingly. To clarify how poor that is, I made the identical calculations for 800+ U.S. Fairness ETFs, and ARKF scored the fourth-lowest. It is in good firm, too. The Roundhill MEME ETF (MEME) and the Direxion Moonshot Innovators ETF (MOON) are the worst at 3.48/10 and three.60/10. The SPDR S&P Oil & Fuel Gear & Companies ETF (XES) is third at 3.79/10, adopted by a number of thematic ETFs, together with these:

ALPS Clear Vitality ETF (ACES): 4.53/10 ProShares S&P Kensho Cleantech ETF (CTEX): 4.75/10 ARK Subsequent Technology Web ETF (ARKW): 4.95/10 ARK Innovation ETF (ARKK): 5.17/10 SPDR Kensho Clear Energy ETF (CNRG): 5.27/10

Particularly to ARKF, solely 57% of its holdings by whole weight are money movement constructive during the last twelve months, and 29% have constructive EBITDA margins. In distinction, QQQ’s figures are 99% on each metrics. Subsequently, I’ve little doubt ARKF would simply fall into that “backside 30%” class.

Fundamentals

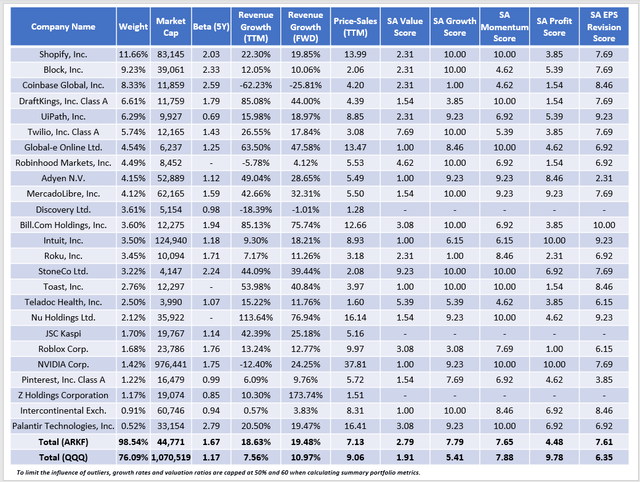

The place ARKF lacks in profitability and valuation, it excels in development. The next desk summarizes the portfolio’s prime 25 holdings.

The Sunday Investor

ARKF’s Searching for Alpha Development Rating is 7.79/10 and has a 19.48% estimated one-year gross sales development price, each within the prime 3% of all ETFs in my database. QQQ’s estimated development price is simply 10.97%, or about half of what it was in January 2022, so there are fewer development alternatives than earlier than. For this reason buyers are actually leaning into extra speculative shares like these held in ARKF. Development is briefly provide, and thematic ETFs like ARKF are a simple technique to achieve publicity.

Nonetheless, one quarter’s value of above-average earnings surprises would not justify ARKF’s 43% YTD value achieve. It isn’t but an upward development, however shareholders are successfully betting it’s. Even when Q2 2023 brings one other 7% earnings shock, we’re removed from the 15% and 20% figures we had in 2009 and 2020. I do not think about there’s a lot upside left, however as demonstrated earlier, these speculative corporations have loads of draw back dangers.

Funding Advice

Assigning a ranking was troublesome as a result of I acknowledge how the market favors the expansion issue. ARKF’s 19.48% estimated gross sales development price is sort of double that of QQQ, and the ETF might proceed to soar if the Q2 earnings season is profitable. Nonetheless, I settled on a “promote” ranking to emphasise ARKF’s draw back dangers. Low-quality portfolios like these are finest for buying and selling, not investing, and since ARKF is up 43% YTD primarily based on only one quarter’s value of above-average earnings surprises, taking income is barely prudent. Thanks for studying, and I sit up for offering one other replace subsequent quarter.

{kind=link}