tupungato/iStock Editorial through Getty Photos

Lanxess Aktiengesellschaft (OTCPK:LNXSF) has had some latest exercise that alerts worth for the enterprise on personal markets. They created a J.V with Creation by spinning off certainly one of its companies, and this has proven that personal markets may worth the remainder of Laxness’ companies, which have turn into more and more specialty and fewer commodity during the last couple of years, at a a lot larger a number of than the place it presently trades.

The problem is that the path for LANXESS’ markets is dangerous, with them being particularly cyclical, and there are dominoes but to fall. The economic system just isn’t doing nicely. Whereas it’s falling slower than anticipated as of now, it should see an extended decline, and there are precise deflation dangers for Lanxess’ whereas they nonetheless lag with costly stock. We would not think about Lanxess in the meanwhile as a result of there are different cheaper concepts whose fortunes usually tend to be incrementally constructive, though the Creation deal actually makes Lanxess fascinating as soon as we come nearer to a probable backside within the cycles nonetheless some quarters away.

Q1 2023 Notes

To the credit score of the Lanxess administration, they do not sugarcoat issues.

And right here, we’ve an enormous publicity to — in Inorganic Pigments to building and building is de facto ugly throughout the board. It is the primary time that I see China building destructive. Europe can be extraordinarily tender. It isn’t as dangerous in the USA. However total, building, which has an underlying constructive traits, 2023 will certainly undergo.

Matthias Zachert, CEO on Lanxess.

Sadly, we’ve to agree with the evaluation. The Chinese language property market scenario disappoints to the draw back, with main falls in growth exercise. When you may argue that is simply the markets discovering new equilibrium, builders are additionally not elevating as a lot funds. Gross sales of properties are up however not due to demand for housing, however due to demand for liquidity, highlighting the fairly pronounced deleveraging danger that China faces. The scenario has spurred a price lower, and whereas it’s useful it is also proof of the hazards of the Chinese language market proper now, a serious marketplace for building and for Lanxess.

Lanxess administration believes this quarter and Q2 shall be troughs, as they attempt to offload stock that has been topic to inflation. Destocking traits might reverse, however the destocking problem is right here on account of the poor demand scenario. Finally, whereas on a technical foundation the stock inflation lag will go by the system, we consider issues can worsen, together with deflation of Lanxess chemical compounds, since even administration acknowledges that markets are inclined to pause and wait out worth declines as soon as the opportunity of deflation and a deflation spiral arrive. That can lengthen the ache. Moreover, there are different footwear that also must drop, together with automotive and digital exposures which have been benefiting from an more and more exhausted pool of pent-up demand.

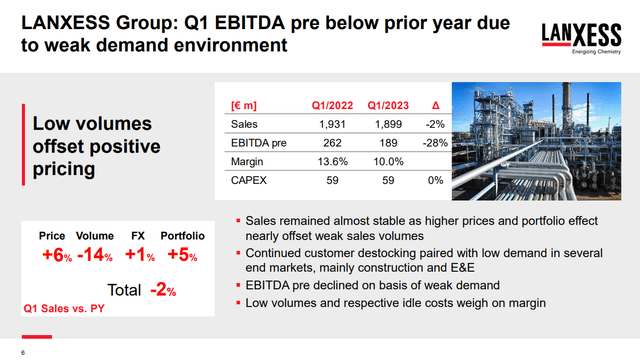

Group Outcomes (Q1 2023 Pres)

Utilization is 65%, beneath averages of 75%, and the main volumes shortfall, not even absolutely offset by costs whereas they liquidate pricey stock, means significant loss in industrial economic system. Therefore, the 28% declines in EBITDA pushed by commodity merchandise but in addition specialty merchandise that face building, Laxness’ key finish market.

Backside Line

The Creation deal was nice. The 1.2 billion EUR or so in proceeds imply a 33% discount in leverage, an actual boon to shareholders delivered by an accretive a number of, above Lanxess’ complete a number of. Furthermore, the worth of the Lanxess stake within the J.V with an choice to exit creates latent worth for Lanxess, for now one other 1.2 billion EUR in worth, however presumably extra if synergies in that deal might be delivered.

Nevertheless, whereas there’s a precedent transaction argument to make for the enterprise proper now, and the 5.4x EV/EBITDA a number of just isn’t excessive (given administration estimates and assuming the J.V worth as a non-operating asset), we’re nonetheless conscious of companies which have much less headwinds and commerce cheaper, all in industrial sectors as nicely. Lanxess AG is an fascinating play, one that we’ll watchlist, however with the earnings path being definitely destructive, simply unsure to what extent, we expect there are different extra direct methods to become profitable in shares proper now.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

{kind=link}